Not all bonds are equally affected by interest rate fluctuations.

Short-duration fixed-income securities reduce interest rate risk by leveraging lower sensitivity, mitigating potential losses in declining bond markets.

Floating-rate corporate bonds minimize exposure to rising Treasury rates and credit spread changes through increased interest payments and short durations.

Rising interest rates benefit long-term investors through opportunities in resilient high-yield corporate bonds, discounted purchases of reputable companies' bonds, and increased coupons, especially during economic expansions.

Riskier investors can profit from longer-term bonds rising in value when central banks are expected to cut interest rates.

Diversifying bond portfolios across sectors, durations, countries, credit qualities, and issuer types is essential for effective risk management.

Embrace the challenge, seize the opportunity - that's the mantra for bond investors navigating the dynamic landscape of rising interest rates. In the face of economic shifts, it's essential to move beyond the conventional narrative that paints high-interest rates as a threat. While some bonds may experience short-term turbulence, the astute investor recognizes that, over the long haul, rising interest rates can be a boon if approached strategically.

High-interest rates, within the economic panorama, represent the cost borrowers incur when accessing capital. This metric has far-reaching implications, influencing the overall health and activity levels of an economy. When interest rates are elevated, the expense associated with borrowing rises, impacting various facets of economic behavior.

Investors find themselves grappling with a scenario not witnessed since the era of Rubik's Cubes and Post-it Notes in the 1980s. The current surge in interest rates, unseen for decades, is compelling a new playbook for generations accustomed to a prolonged period of low borrowing costs.

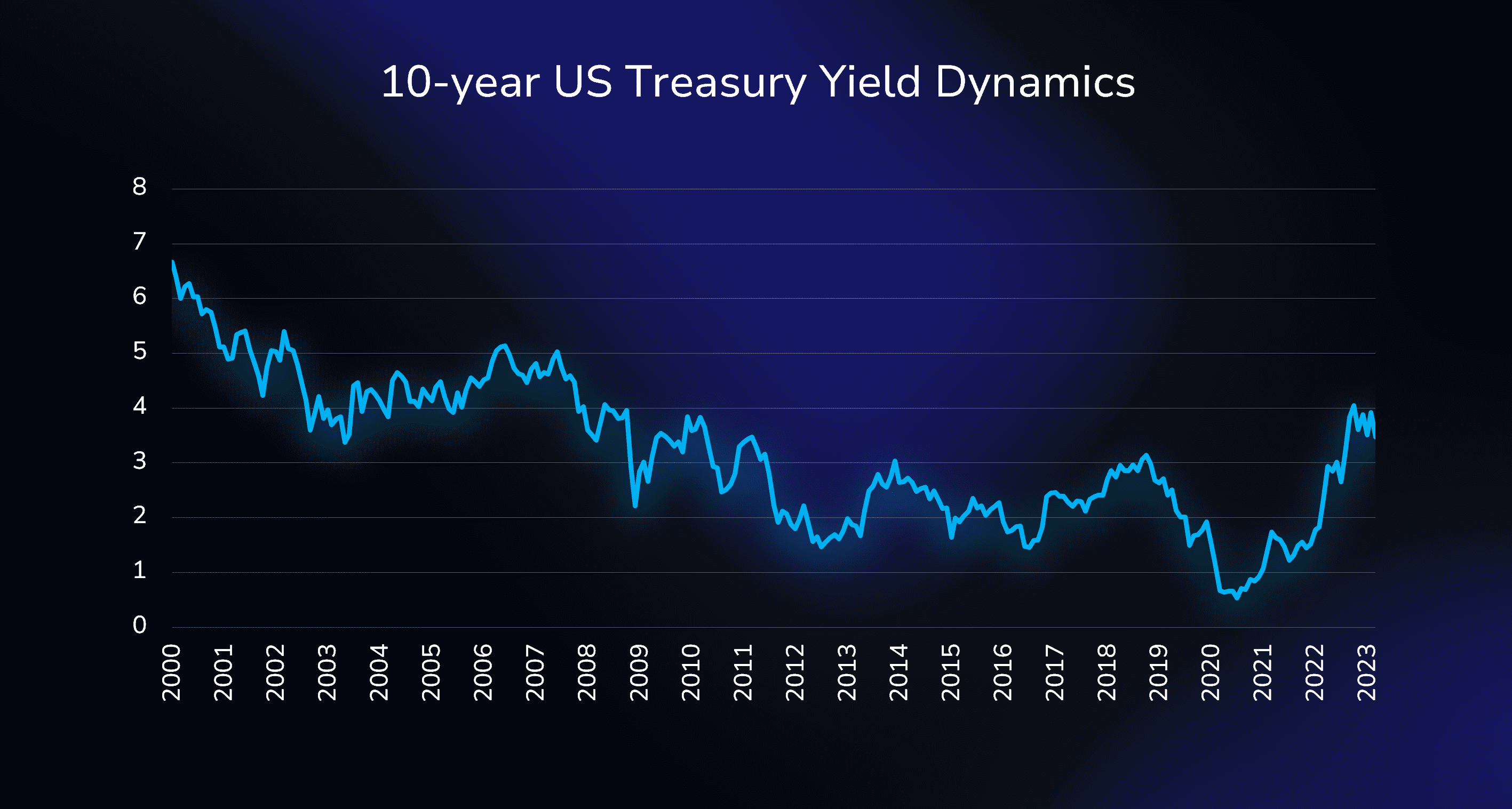

Transitioning from an era of "lower for longer" to a sudden "higher for longer" has upended established plans. The 10-year Treasury yield, which had been approaching 5% in 2023, has risen from just 0.52% in August 2020 to its highest level in 16 years. Recent expectations by many investors that the Fed will start cutting rates in 2024 have pushed the Treasury yield lower. However, the current level of around 4% is still high and has not been seen before 2023 for over a decade. Unlike previous episodes, this ascent follows a backdrop of prolonged low rates, challenging investors unaccustomed to such market dynamics.

Economic health indicators, such asGDP growth, employment rates, and inflation, play a significant role. Positive indicators may prompt central banks to raise interest rates as a measure to control economic activity and inflation. The policies enacted by central banks are pivotal in determining interest rates, with tools like adjusting policy rates and open market operations employed to influence borrowing costs and foster economic stability, responding to inflationary pressures and maintaining a balance between price stability and economic growth.

it's crucial to dispel the myth that all bonds are equally affected by interest rate fluctuations. The common adage, "when interest rates rise, bond prices fall," oversimplifies the intricate dynamics at play.

The impact of interest rate changes varies across different bonds, influenced by factors such as maturity dates and coupon rates. Generally, bonds with extended maturity periods and lower coupon rates are more susceptible to the sway of interest rate adjustments. High-yield bonds which are the bonds with lower credit quality are more susceptible to corporate events and changes in the financial standing of the borrowers than to the general movements of interest rates. This nuanced sensitivity underscores the importance of considering the specific attributes of each bond when navigating the complex fixed-income landscape.

One effective strategy for potential profit amid rising interest rates is to focus on fixed-income securities with a short duration. Short-term bonds tend to have lower exposure to interest rate risk compared to their longer-term counterparts, as their prices are less sensitive to changes in interest rates. This approach can help mitigate potential losses associated with falling bond prices when interest rates rise.

At the moment, European investment-grade bonds with short maturities of less than two years offer attractive yields, close to 4% in euro terms. For example, Lufthansa's 2.875% Nov 2025 bond (XS2296201424) is yielding 3.7%, while Intesa Sanpaolo's 0.75% Dec 2024 bond (XS2089368596) is yielding 3.8% at the time of purchase.

Floating-rate corporate bonds have interest payments that increase when Treasury rates rise. As a result, investors in these securities have almost no exposure to changes in Treasury rates. In addition, because floating-rate securities generally have short durations, changes in credit spreads have limited (but not zero) impact on their value. Just like short-duration fixed-coupon corporate bonds, these securities reduce exposure to interest rates and credit spreads simultaneously.

To illustrate, take a look at Italy's 4.621% Apr 2026 government bond (IT0005428617), which has a coupon linked to the 6-month Euribor rate.

For long-term investors, rising interest rates can be advantageous for several reasons. Firstly, many corporate bonds, particularly high yield ones, are not very sensitive to changes in interest rates, but are more sensitive to changes in the financial health of the companies, while offering a generous level of yield, that allows them to continue to perform well as interest rates rise. Secondly, as interest rates rise, opportunities emerge for investors to acquire bonds of reputable companies at discounted prices. The inverse relationship between Treasury yields and corporate bond prices creates buying opportunities, especially during periods of economic expansion.

Furthermore, rising interest rates can drive higher bond coupons and yields on future corporate bond issues. This becomes particularly relevant for investment-grade corporate bonds, where an improving economy can lead to higher income with less default risk.

Somewhat at odds with the above strategies, riskier investors can take advantage of the tendency of longer-term bonds to rise rapidly in value when central banks are expected to cut interest rates. Instead of holding long-term bonds to maturity, investors can buy them, wait for their market value to rise and then sell them at a higher price when yields have compressed sufficiently. This method can generate additional profits in a relatively short period of time, sometimes as little as a year or less.

The strategy is based on the inverse relationship between bond prices and yields. Duration is a key measure of the sensitivity of a bond or bond fund to changes in interest rates and is influenced by its maturity and yield. In essence, the longer the duration of a bond, the greater its potential gain when interest rates fall. For example, a bond with a duration of 10 years would increase in value by approximately 10% if interest rates fell by one percentage point.

Investors looking to take advantage of the end of the Federal Reserve's or European Central Bank's tightening cycle could consider extending the duration of their bonds. However, investors should be aware that this strategy carries much higher risks than the others mentioned above. It's difficult to time the market accurately and there's always the risk of incurring losses on price falls. In addition, given the recent volatility in interest rates, yields could potentially rise if inflation picks up again.

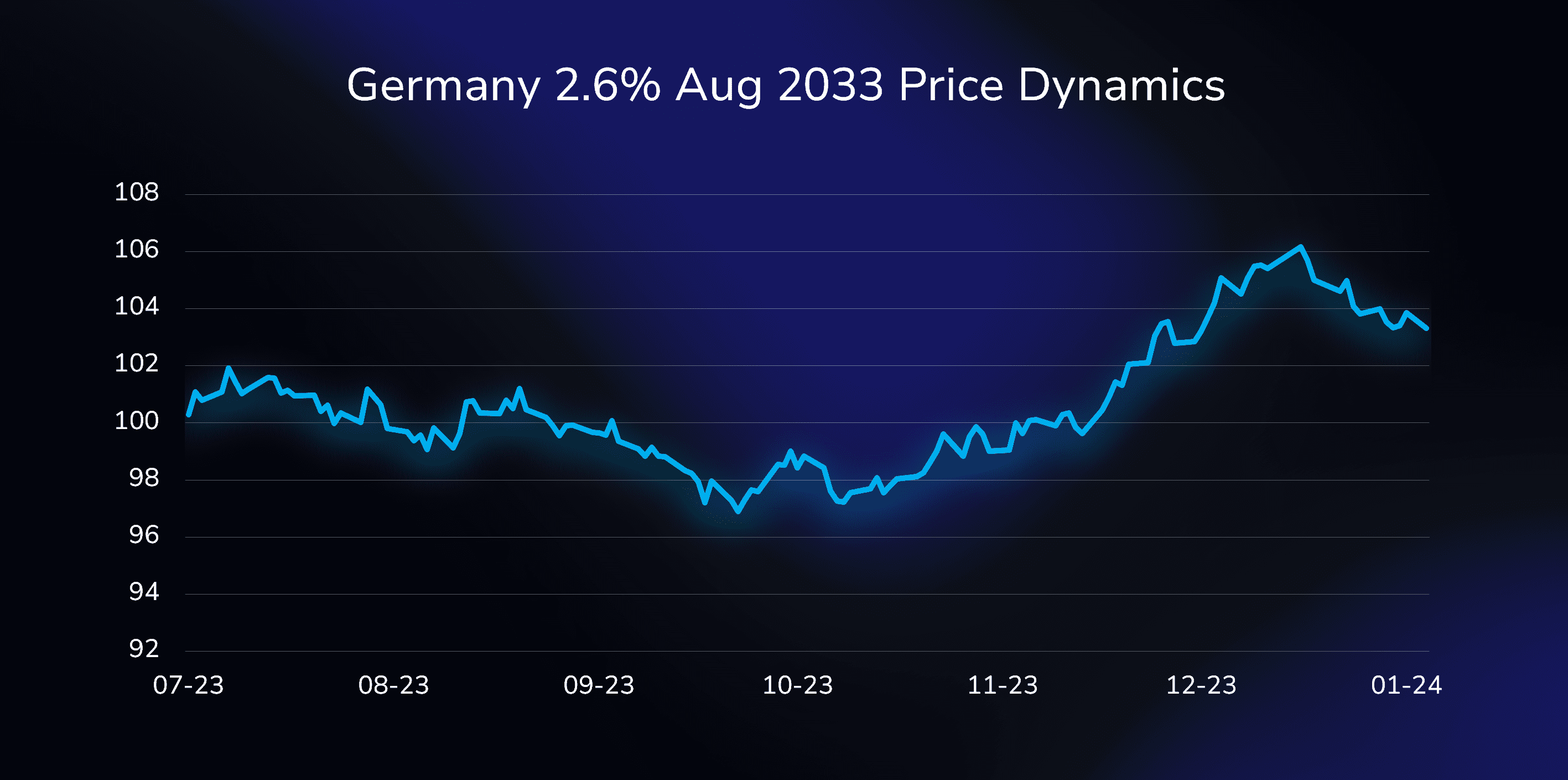

To illustrate, consider an investment in a 10-year German government bond (Bund) with a duration of 8.8 at the beginning of October 2023. This investment strategy would have yielded an impressive return of over 7% in euro terms in just three months.

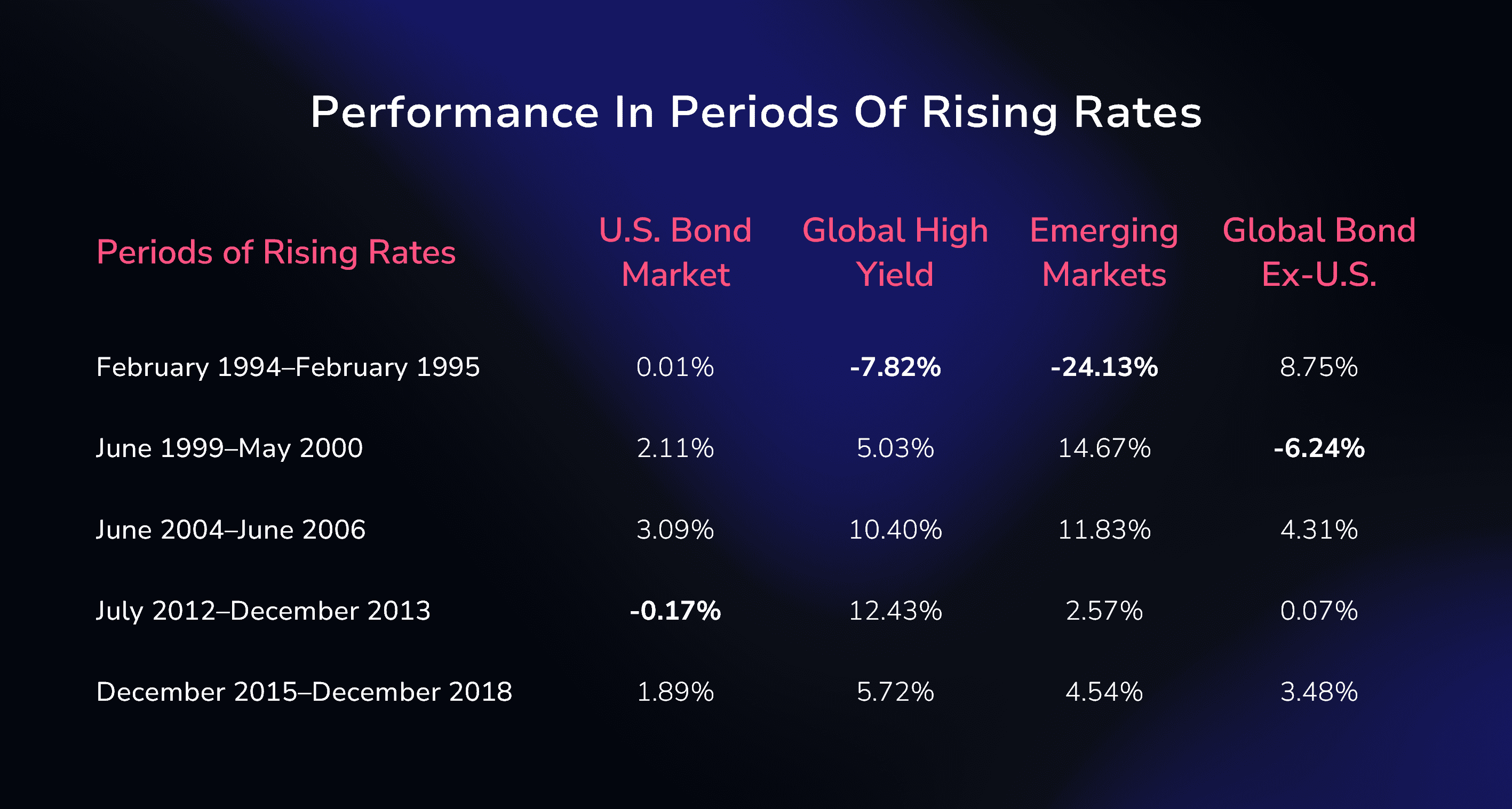

Diversification is as crucial for optimizing your online bond portfolio as it is for managing stocks. Bonds can be diversified across various factors, such as sector, duration, country of origin, credit quality, or issuer type. Examining historical performance, it's evident that different international bond markets exhibit significant variation. By cultivating a diversified portfolio that extends beyond U.S. bonds, investors stand to benefit from the positive returns of specific bonds even when others may face declines. While diversification is an effective risk management strategy, it's essential to recognize that it doesn't guarantee profits or provide absolute protection against losses in an unpredictable online market.

Source: T. Rowe Price

The evolving realm of high-interest rates presents both challenges and opportunities for bond investors. Navigating this dynamic landscape requires a departure from conventional narratives, as well as a strategic mindset that goes beyond simplistic views on interest rate fluctuations. Understanding the specific dynamics of bonds, considering factors like maturity dates and coupon rates, allows investors to craft a nuanced and effective strategy.

Various tactical approaches offer avenues for profit amid rising interest rates, from focusing on short-term and floating-rate bonds to capitalizing on the long-term benefits of economic expansions. Diversification remains a critical risk management tool, offering investors the ability to spread their portfolio across different factors and international markets.