Premium

PremiumPublication date: 22-05-2026

Brazil's largest taxpayer, accounting for roughly 7% of all national tax revenue, and the country's main fuel supplier — Petrobras is about as systemic as an issuer could be. The question is whether you are buying an oil major, a sovereign proxy, or both.

Source: Agência Petrobras

Petróleo Brasileiro S.A. (Petrobras) is one of the world's largest integrated oil and gas groups and the dominant energy producer in Latin America. The company explores for and produces crude oil and natural gas, refines petroleum products, and distributes them both in Brazil and abroad.

The Brazilian state retains control over Petrobras, holding about 50,3% of voting shares and roughly 36,6% of total share capital. This makes Petrobras a strategically important asset for the Brazilian economy: the company is one of the key fuel suppliers in the domestic market and the country's largest taxpayer. In 2025, Petrobras paid 278 billion Brazilian reais (about $48 billion) into the Brazilian budget system in the form of taxes, royalties, and other mandatory contributions, 3% more than in the previous year. The company additionally paid around $449 million in taxes outside Brazil. Over the last five years, Petrobras's cumulative contribution to Brazil's public finances exceeded 1,3 trillion reais, and the company accounts for roughly 7% of total national tax revenue — a scale that reflects its systemic significance for the country as a whole and places it firmly in the "Too Big to Fail" category.

Production remains the company's main competitive advantage. In 2025, Petrobras exceeded all of its operational targets: combined oil and natural gas output reached 3 million barrels of oil equivalent per day (boe/d), 11% above the 2024 level and one of the highest production volumes in the company's history. Commercial production accounted for 2,6 million boe/d. The pre-salt fields in the Santos and Campos basins play a central role in this growth, contributing 82% of total output. Two new platforms came on stream in 2025: FPSO Almirante Tamandaré at the Búzios field and FPSO Alexandre de Gusmão at the Mero field.

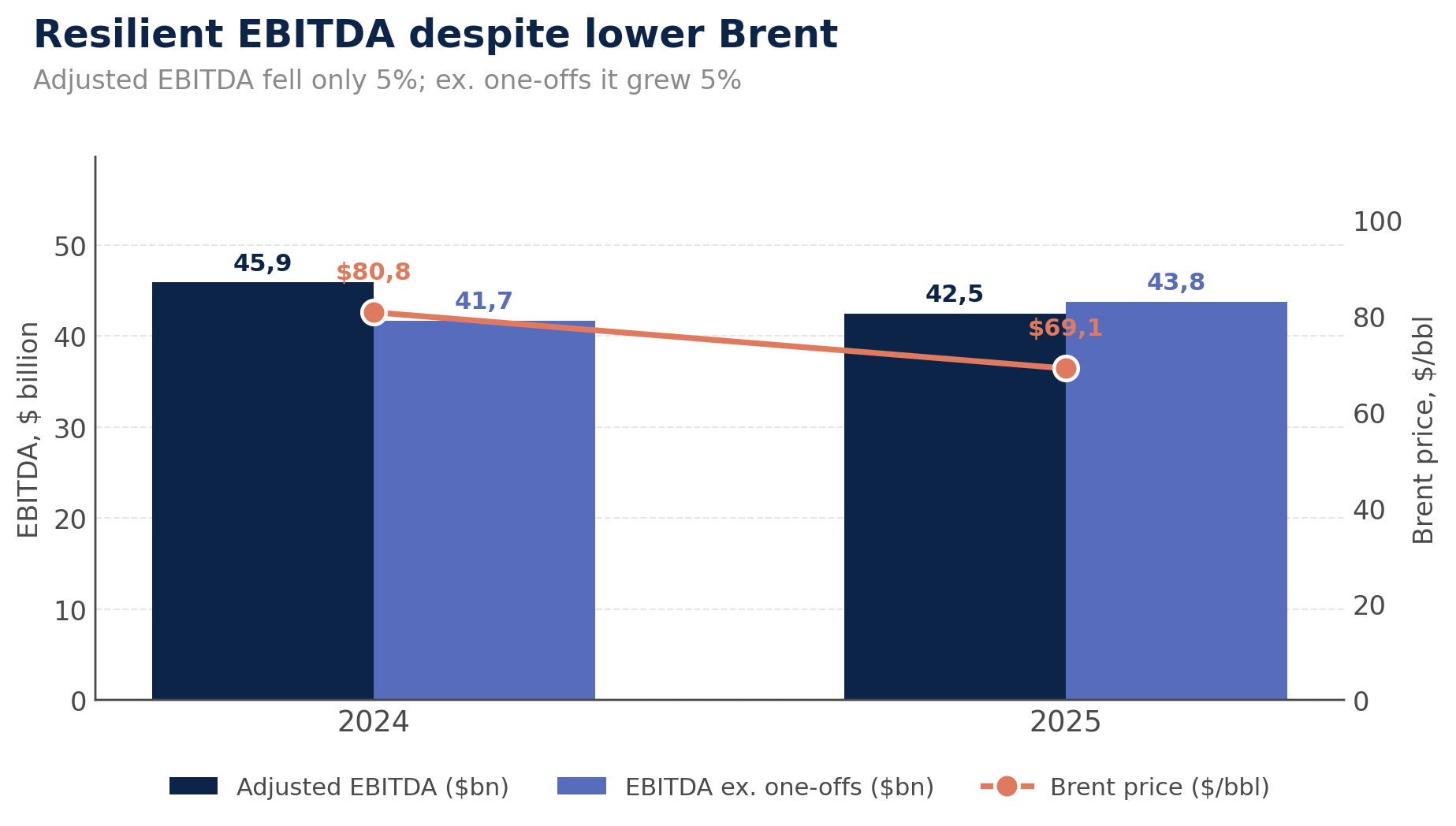

Production costs remain globally competitive. Under its 2025–2029 strategic plan, the company targets full lifting costs of around 36,5 USD/boe. With the average Brent price at $69,1 per barrel in 2025, this leaves a substantial operating margin even in a volatile oil market. Petrobras also operates an extensive refining network: in 2025, refinery utilization reached 91%, a multi-year high, and 68% of refined output consisted of diesel, gasoline, and jet fuel — the products with the highest added value.

The 2025 financial results confirmed the resilience of Petrobras's operating model even against the backdrop of falling oil prices. The average Brent price declined from $80,8 per barrel in 2024 to $69,1 in 2025, yet thanks to higher production volumes and strong operational efficiency, adjusted EBITDA fell by only 5%, to $42,5 billion. Excluding one-off items, EBITDA actually increased by 5%, reaching $43,8 billion, reflecting the company's ability to maintain stable cash generation in a volatile commodity environment. Operating cash flow came in at $36,0 billion, free cash flow at $16,5 billion, and revenue at $89,2 billion.

Source: Petrobras, SEC filings

Reported net income reached $19,7 billion, up 160% versus 2024, boosted by a one-off currency effect from the appreciation of the Brazilian real against the dollar. Normalized for one-off items, net income stood at $18,1 billion, 6,5% below the 2024 level — a decline explained entirely by lower oil prices.

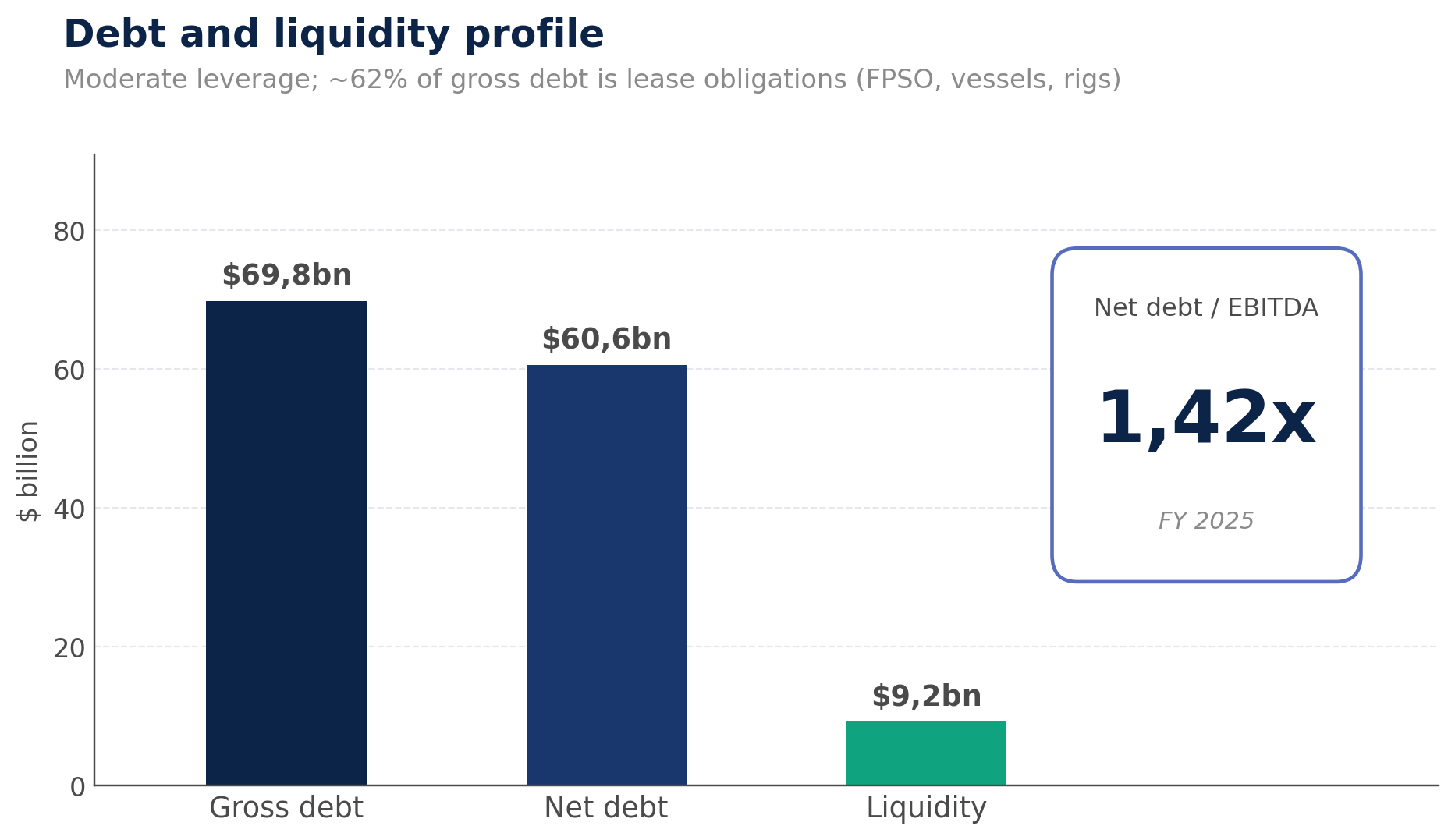

On the debt side, gross debt as of 31 December 2025 stood at $69,8 billion, of which about 62% consisted of lease obligations (FPSO platforms, vessels, drilling rigs), in line with the company's business model. Net debt was $60,6 billion, and the net debt to adjusted EBITDA ratio was 1,4x at the end of Q4 2025. Liquidity is supported by cash and short-term financial investments of $9,2 billion.

Source: Petrobras 4Q25 Results, SEC filings

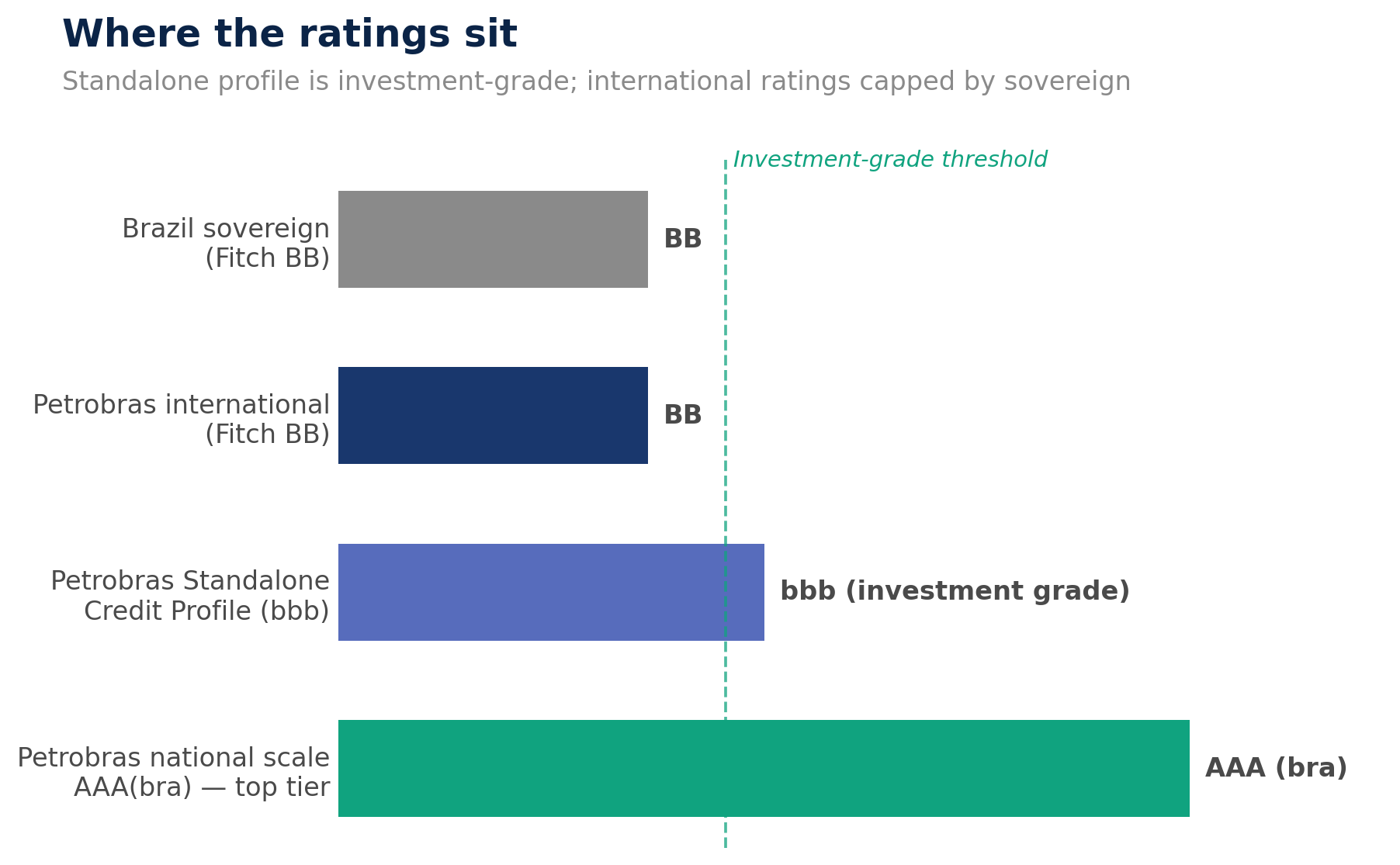

On credit ratings, Moody's rates Petrobras at Ba1 with a stable outlook (the outlook was revised from positive to stable in June 2025, following a similar action on Brazil's sovereign rating). Fitch Ratings has the company at BB, also with a stable outlook. Fitch additionally assigns Petrobras the highest national-scale rating, "AAA(bra)", reflecting the company's exceptionally strong position in the Brazilian domestic market and its high relative creditworthiness among local issuers. Notably, Fitch assesses Petrobras's standalone credit profile at "bbb", which corresponds to the investment-grade category. The company's current international ratings are therefore constrained primarily by Brazil's sovereign ceiling rather than by any fundamental weaknesses of the issuer itself.

Source: Fitch Ratings, Petrobras IR

The Petrobras Global Finance 6,875% notes due January 2040 are senior unsecured obligations denominated in U.S. dollars. As a long-dated bond, the issue has a high duration (around 8,6 years) and elevated sensitivity to interest rates. In return, investors receive a fixed 6,875% coupon paid semi-annually and a yield to maturity of around 6,7%.

as of 31-12-2025 USD bn

| Column 1 | Column 2 | Column 3 | Column 4 | Column 5 | Column 6 |

|---|---|---|---|---|---|

| Assets | 222,3 | Adj. EBITDA | 42,5 | Net debt | 60,6 |

| Revenue | 89,2 | Gross debt | 69,8 | Net debt / Adj. EBITDA | 1,42x |

| Operating cash flow | 36,0 | Free cash flow | 16,5 | Equity | 75,9 |

All data and information is provided “as is” for informational purposes only, and is not intended for trading purposes or financial, investment, tax, legal, accounting or other advice. Please consult your broker or financial representative to verify pricing before executing any trade. Bondfish is not an investment adviser, financial adviser or a broker. None of the data and information constitutes investment advice nor an offering, recommendation or solicitation by Bondfish to buy, sell or hold any security or financial product, and Bondfish makes no representation (and has no opinion) regarding the advisability or suitability of any investment. Mention of specific financial products or operations does not constitute an endorsement by Bondfish.

The financial products or operations referred to in such data and information may not be suitable for your investment profile and investment objectives or expectations. It is your responsibility to consider whether any financial product or operation is suitable for you based on your interests, investment objectives, investment horizon and risk appetite. Bondfish shall not be liable for any damages arising from any operations or investments in financial products referred to within. Bondfish does not recommend using the data and information provided as the only basis for making any investment decision.

This data is not updated in real time and represents the prices available at the end of the previous trading day. Bondfish does not verify any data and disclaims any obligation to do so. Bondfish expressly disclaims the accuracy, adequacy, or completeness of any data and shall not be liable for any errors, omissions or other defects therein, delays or interruptions in such data, or for any actions taken in reliance thereon. Bondfish shall not be liable for any damages relating to your use of the information provided herein.

Past performance is not a reliable indicator of future results.