Premium

Premium

Updated 14-07-2026: the bond rallied on news of the upcoming refinancing. At current prices the yield is no longer attractive, but investors who bought when we first flagged the bond in May - have earned roughly 12% in just two months!

Publication date: 29-05-2026

Internet where there is a village —" Internet dove c'è un paese" — is the slogan of today's bond in focus by niche Italian internet provider EOLO. The strong 11% EUR yield is normally locked behind a €100,000 bond notional value, but with our partner Mintos, any investor can buy a fractional position of any minimum desired size.

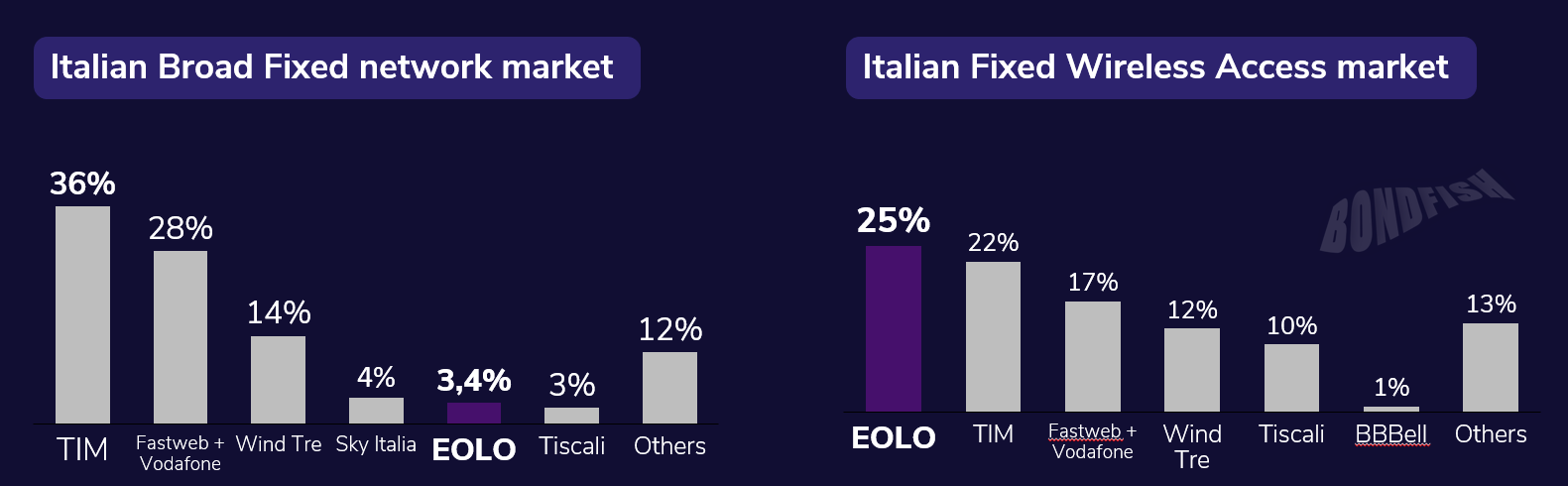

EOLO is the largest fixed wireless access (FWA) broadband operator in Italy. The technology brings internet to areas with limited access to traditional fibre cable networks. In Italy, EOLO controls 25% of the FWA market and a much lower 3,4% of the broader internet market - as FWA is a new technology only gaining attention. The bond's strong EUR yield of around 11% makes it worth a closer look ahead of its October 2028 maturity.

Italian fixed internet market. Source: AGCOM - the Italian communications regulator.

Italian fixed internet market. Source: AGCOM - the Italian communications regulator.

98% of sales come from selling wireless access to homes and small businesses.

The company covers 7.000 Italian towns - mostly in Northern Italy - with most under 10.000 people. This user base grows 4-5% a year, 2 times slower than the total Italian FWA market. EOLO customers change providers less often due to a limited number of providers in the served areas. The actual attrition number (the churn ratio) is not disclosed, but it is described as much lower than the Italian average of about 14%. Revenue per user is stable at around €30 a month. Such stability supports sales, compared to the Italian communications price index down 13% since 2021. That makes Italian internet one of the cheapest in Europe.

EOLO is highly leveraged at a 5,5-6,5× Net Debt / EBITDA ratio, with EBITDA at around €120 mn and gross debt of €755 mn (including a €343 mn interest-free shareholder loan). This debt built up for two reasons. The first was the shareholder change in 2021-2022, when over €1 bn of new debt was placed. The second reason is the heavy network expansion. EOLO invests nearly all EBITDA to increase its FWA coverage and speeds - with CAPEX of around €100 mn per year since 2021.

Leverage is unlikely to decrease by bond maturity in 2028. Free cash flow is likely to remain negative due to network investments exceeding EBITDA. The EBITDA increase depends on whether EOLO's user base and FWA adoption in general can still grow in Italy - and here the picture is mixed.

First, we need to understand the Fixed Wireless Access (FWA) technology.

It delivers home broadband over a radio signal instead of a cable. EOLO built its own network of >4k radio base stations. Its customers have an outdoor antenna installed on each roof, pointed at the nearest tower in line of sight. The customer's router is connected to that antenna by cable, so there is no SIM card and no reliance on mobile networks. EOLO operates two technology layers: a legacy 5 GHz band (lower speed, longer range) and millimeter-wave 26/28 GHz (up to 1 Gbps). One tower can serve hundreds of households within a few kilometres. The trade-off is dependence on physical line of sight and weather sensitivity at higher frequencies.

FWA is popular in Italy because fixed broadband internet reached rural areas late and was often unprofitable.

The government is funding rural fibre internet coverage in the same areas where EOLO operates (through a plan called "Piano Italia 1 Giga"). Satellite broadband, including Starlink, is a secondary threat, but its higher price keeps it off most EOLO households. Overall, the FWA market is expected to remain at around 10-15% share, with fixed broadband taking the rest. EOLO can still compete with fibre by investing in network stability and speeds.

EOLO's coverage across Italy. Source: EOLO S.p.A Impact Report 2024/25

The debt refinancing and CAPEX funding mainly depend on continuing shareholder support.

EOLO's main shareholder is Partners Group, a Swiss private equity firm, which bought a 75% stake in a €1,1 bn debt-funded buyout in 2021. For Partners Group's AUM of $185 bn, EOLO is a small investment - affordable to support, but not one Partners Group would defend at any cost if the business runs into distress. The remaining 25% is held by founder Luca Spada, who still runs operations while Partners Group controls the board. Since the acquisition, shareholders waived €0,4 bn of debt, and the remaining €0,3 bn shareholder loan is interest-free and sits junior to bondholders. In the last 2 years, they additionally committed €90 mn of liquidity to support CAPEX.

The €375 mn note is senior debt secured by EOLO's shares and assets.

It sits behind a €140 mn super senior loan and ahead of the €343 mn interest-free shareholder loan. The issue is rated B/stable by Fitch and S&P and B3/stable by Moody's. Ratings reflect a strong position in the niche FWA market and shareholder support, offset by high leverage and negative free cash flow due to heavy CAPEX.

as of 31-03-2025 EUR bn

| Metric | Value | Metric | Value | Metric | Value |

|---|---|---|---|---|---|

| Assets | 1,4 | EBITDA Margin LTM | 48 % | CFO/Debt | 0,15 |

| Revenue LTM | 0,2 | Net debt | 0,8 | FCF LTM | - |

| EBITDA LTM | 0,1 | Net Debt/EBITDA | 7,1× | Equity | 0,4 |

| Net Profit LTM | -0,1 | EBITDA/Interest | 3,3× | Debt/Equity | 2,3× |

All data and information is provided “as is” for informational purposes only, and is not intended for trading purposes or financial, investment, tax, legal, accounting or other advice. Please consult your broker or financial representative to verify pricing before executing any trade. Bondfish is not an investment adviser, financial adviser or a broker. None of the data and information constitutes investment advice nor an offering, recommendation or solicitation by Bondfish to buy, sell or hold any security or financial product, and Bondfish makes no representation (and has no opinion) regarding the advisability or suitability of any investment. Mention of specific financial products or operations does not constitute an endorsement by Bondfish.

The financial products or operations referred to in such data and information may not be suitable for your investment profile and investment objectives or expectations. It is your responsibility to consider whether any financial product or operation is suitable for you based on your interests, investment objectives, investment horizon and risk appetite. Bondfish shall not be liable for any damages arising from any operations or investments in financial products referred to within. Bondfish does not recommend using the data and information provided as the only basis for making any investment decision.

This data is not updated in real time and represents the prices available at the end of the previous trading day. Bondfish does not verify any data and disclaims any obligation to do so. Bondfish expressly disclaims the accuracy, adequacy, or completeness of any data and shall not be liable for any errors, omissions or other defects therein, delays or interruptions in such data, or for any actions taken in reliance thereon. Bondfish shall not be liable for any damages relating to your use of the information provided herein.

Past performance is not a reliable indicator of future results.