Premium

Premium

Publication date: 13-10-2025 (updated: 15-03-2026)

Romania's recent story is one of fiscal correction, political renewal, and a difficult balancing act between reform and growth.

After a turbulent election year in 2024, the country entered a new phase in May 2025, when President Nicușor Dan, an independent, pro-EU reformist, came to power. He has brought a pragmatic tone to politics, working closely with Prime Minister Ilie-Gavril Bolojan, whose government draws on a four-party coalition holding close to two-thirds of parliamentary seats. Their joint task is to narrow the budget deficit while keeping the economy from stalling. They are doing it through a combination of VAT rate increases (from 19% to 21%), excise hikes on fuels and alcohol, a public sector wage and pension freeze, cuts to bonuses and non-critical investment, and improved tax collection.

Romania is a semi-presidential republic, where the president is head of state and the prime minister leads the government. The two now share the responsibility of guiding the country through its most ambitious fiscal adjustment in over a decade. The budget deficit peaked at 9,3% of GDP in 2024. The 2025 cash deficit of 7,7% of GDP came in well below the government's own 8,4% target, and January 2026 recorded a small budget surplus. For 2026, estimates range between 6,0% and 6,4% of GDP. The process will be difficult, but the early results have been encouraging.

Source: Country Investor Presentation Feb 2026

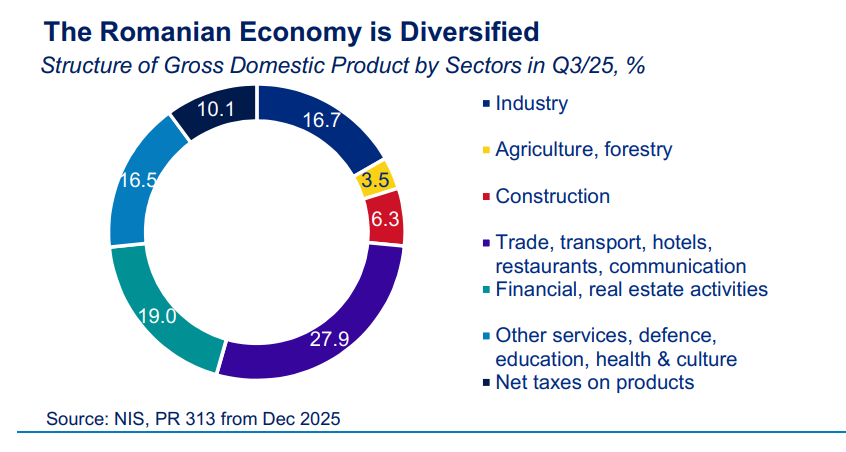

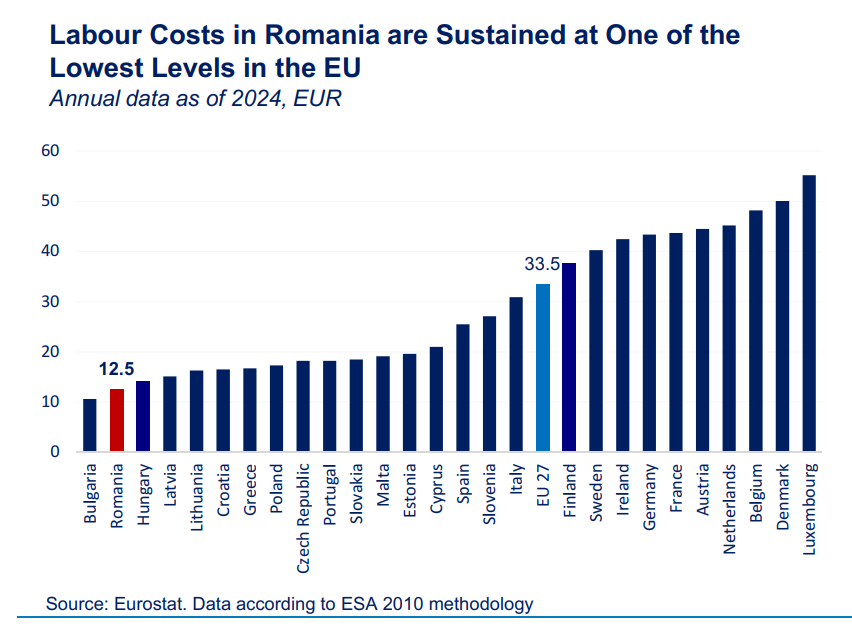

Despite short-term pain, Romania's fundamentals remain sound. The economy is diversified: industry accounts for about 16,7% of GDP, with electronics, IT, and motor-vehicle production forming its backbone. Trade, transport, and services contribute around 27,9%, while agriculture and natural gas play supporting roles. Romania is the largest electronics producer in Central and Eastern Europe and a growing centre for cybersecurity and software. Income levels are among the highest in the region, with GDP per capita (PPP) estimated at USD 46.900 in 2024. Labour costs of EUR 12,5 per hour remain among the lowest in the EU. This combination supports the country's competitiveness.

Source: Country Investor Presentation Feb 2026

The country's strategic location shapes its importance. Together with Bulgaria, Romania provides the EU with access to the Black Sea, a key trade and security corridor linking Europe with the Caucasus and the Middle East. Its membership in NATO, the EU (since 2007), and the Schengen area (since March 2024) underlines its deep integration with Western institutions.

Economically, Romania faces headwinds. Growth slowed to 0,9% in 2024 and only 0,7% in 2025. The economy entered a technical recession in the second half of 2025, with GDP contracting 1,9% quarter-on-quarter in Q4. Growth in 2026 is forecast at just 0,6% as fiscal tightening continues to weigh on domestic demand. Inflation remains among the highest in the region at 9,3% in February 2026, driven by VAT hikes and the removal of energy price caps. It may exceed 10% in April–May 2026. The National Bank of Romania holds its policy rate at 6,50% and has signalled that rate cuts are unlikely before the summer of 2026.

Trade is tightly integrated with the EU single market, with Germany as Romania's main partner. More than two-thirds of both exports and imports are with EU countries. The current account deficit narrowed only marginally, from 8,2% of GDP in 2024 to about 8,0% in 2025. Rising interest and FDI income payments abroad have slowed the adjustment despite fiscal tightening. The gap is expected to narrow toward 6% of GDP in 2026 as import demand falls.

Romania's public debt stood at 59,6% of GDP at end-2025, up from 54,8% at end-2024. Over 50% of government debt is denominated in foreign currency, predominantly euros. Debt is projected to rise toward 63% of GDP by 2027 and stabilise near 65% by the end of the decade. Credit rating agencies keep the country at the lowest investment-grade level: S&P BBB-/Negative, Fitch BBB-/Negative, and Moody's Baa3/Negative. All three recognise the strong reform intent of the new leadership but stress the importance of implementation beyond 2026.

The country benefits from substantial EU support. Roughly EUR 40 billion (about 10% of GDP) in EU funds remain available under the 2021–2027 framework and the Recovery and Resilience Facility. In addition, Romania was allocated EUR 16,7 billion (about 4,4% of GDP) under the EU's Security Action for Europe (SAFE) programme for defence procurement in September 2025. These inflows support public investment, help finance external deficits, and reduce reliance on market borrowing.

The 6,625% euro bond due September 2029 offers a high fixed coupon in euros, and no early-redemption risk. It matures before President Dan's current term ends in 2030, providing investors with visibility through a predictable political cycle as Romania works to restore fiscal stability and deepen its European integration.

as of 31-12-2025

| Column 1 | Column 2 | Column 3 | Column 4 | Column 5 | Column 6 |

|---|---|---|---|---|---|

| GDP, EUR bn | 378,8 | Debt/GDP | 59,6 % | Inflation | 9,7 % |

| GDP per capita, EUR th | 19,9 | Foreign currency debt / Government debt | 47,3 | Unemployment | 6,1 % |

| GDP growth, yoy | 0,7 % | Interest expense / Government revenue | 7,6 % | Central government balance / GDP | -7,7 % |

| Current account / GDP | -8,0 % | Reserves / foreign-currency debt | 72 % | Policy rate | 6,5 % |

All data and information is provided “as is” for informational purposes only, and is not intended for trading purposes or financial, investment, tax, legal, accounting or other advice. Please consult your broker or financial representative to verify pricing before executing any trade. Bondfish is not an investment adviser, financial adviser or a broker. None of the data and information constitutes investment advice nor an offering, recommendation or solicitation by Bondfish to buy, sell or hold any security or financial product, and Bondfish makes no representation (and has no opinion) regarding the advisability or suitability of any investment. Mention of specific financial products or operations does not constitute an endorsement by Bondfish.

The financial products or operations referred to in such data and information may not be suitable for your investment profile and investment objectives or expectations. It is your responsibility to consider whether any financial product or operation is suitable for you based on your interests, investment objectives, investment horizon and risk appetite. Bondfish shall not be liable for any damages arising from any operations or investments in financial products referred to within. Bondfish does not recommend using the data and information provided as the only basis for making any investment decision.

This data is not updated in real time and represents the prices available at the end of the previous trading day. Bondfish does not verify any data and disclaims any obligation to do so. Bondfish expressly disclaims the accuracy, adequacy, or completeness of any data and shall not be liable for any errors, omissions or other defects therein, delays or interruptions in such data, or for any actions taken in reliance thereon. Bondfish shall not be liable for any damages relating to your use of the information provided herein.

Past performance is not a reliable indicator of future results.