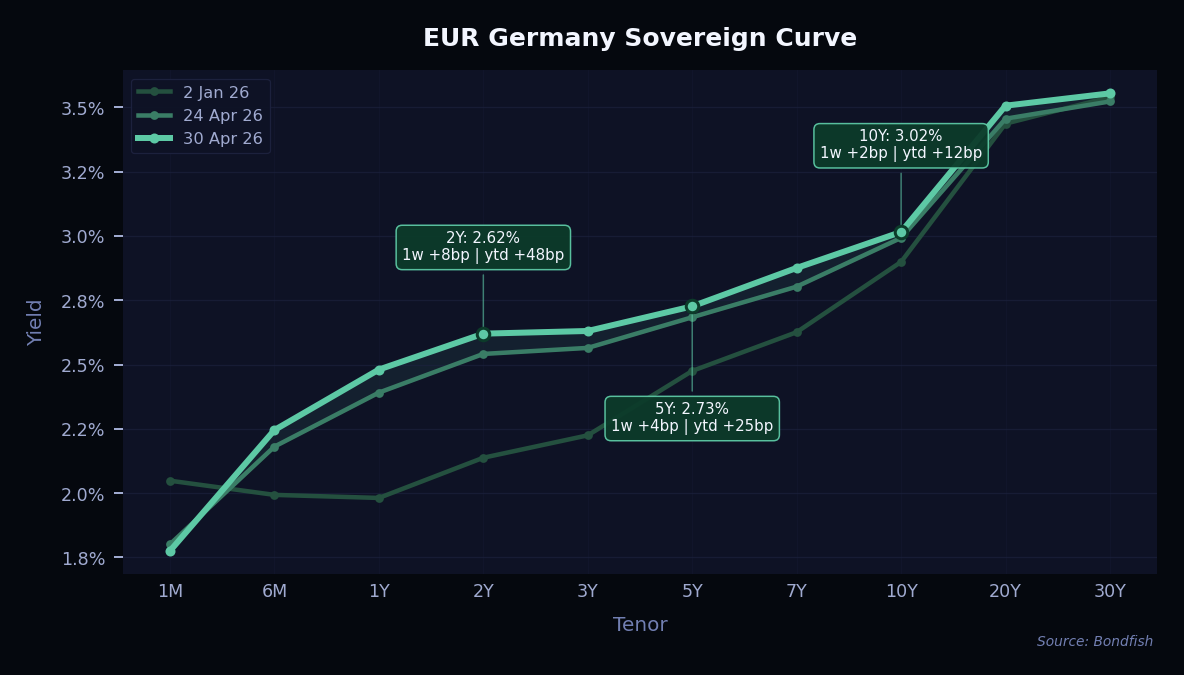

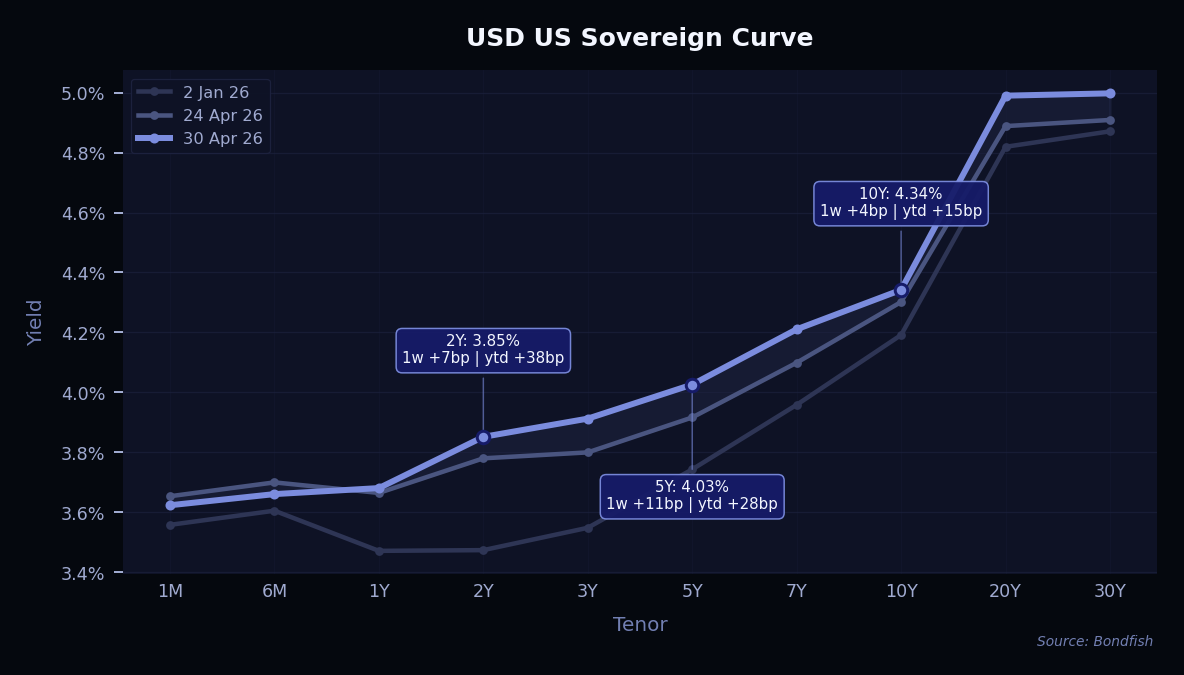

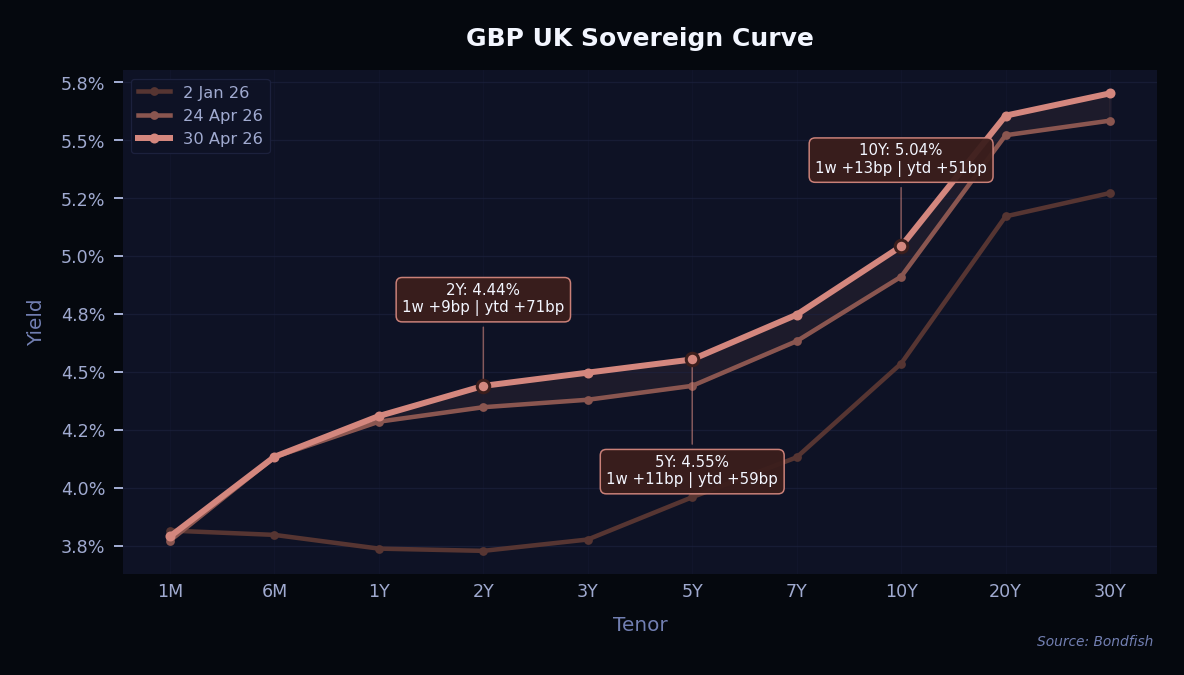

Developed market yield curves moved higher during the week, as investors reacted to renewed inflation pressure from higher energy prices, continued geopolitical uncertainty and more hawkish central bank signals. In the US, the Fed kept rates unchanged, but several policymakers pushed back against the idea that the next move is more likely to be a cut, making markets price a more balanced risk between future hikes and cuts. In Europe, the ECB also stayed on hold, but further hikes remain possible if energy-driven inflation pressure persists. In the UK, the BoE described its decision as an “active hold,” with policy still sensitive to the scale and duration of the energy shock. Trading conditions were also thinner than usual because of the short trading week and the Labour Day holiday across much of Europe, which may have amplified some of the moves. Overall, the week was another reminder that duration risk remains important while inflation and central bank uncertainty stay elevated.

Credit markets were mixed but resilient during the week. Higher government bond yields put pressure on bond prices, especially for longer-duration bonds. At the same time, credit spreads remained broadly stable, supported by solid corporate earnings, continued fund inflows and demand from investors looking for attractive yields. High-quality bonds continued to find buyers, while high-yield spreads were almost unchanged despite the more hawkish tone from the central banks.

Below are the bonds with the strongest weekly price appreciation.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| bla se tr db 0.35% Mar 2027 | CHF | 0,34% | 0,74% | Medium |

|

Reason

No clear positive issuer catalyst

|

||||

| Pfndbnk Schweiz 0.625% May 2031 | CHF | 0,17% | 0,55% | VeryLow |

|

Reason

No clear positive issuer catalyst

|

||||

| AIR FRANCE-KLM 7.25% May 2026 | EUR | 0,13% | 2,76% | Medium |

|

Reason

Air France-KLM beat Q1 estimates with a narrower-than-expected operating loss.

|

||||

| Pfndbnk Schweiz 1.875% Jun 2050 | CHF | 0,11% | 1,14% | VeryLow |

|

Reason

No clear positive issuer catalyst

|

||||

The following bonds experienced the sharpest weekly declines.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| Foncier 3.875% Apr 2055 | EUR | -1,16% | 4,11% | VeryLow |

|

Reason

Long duration amplified losses as yields rose

|

||||

| Goldman Sachs 5.4% Aug 2035 | USD | -1,02% | 5,45% | Low |

|

Reason

Long duration amplified losses as yields rose

|

||||

| Natl Bk Canada 4.1% Oct 2027 | USD | -0,79% | 4,47% | VeryLow |

|

Reason

No clear negative issuer catalyst

|

||||

| Citigroup 5% May 2032 | USD | -0,32% | 5,21% | Low |

|

Reason

No clear negative issuer catalyst

|

||||

Note: only long-term senior unsecured ratings were taken into account.

| Issuer | Agency | Change |

| Adeia | S&P | BB- → BB |

| Agnico Eagle Mines | Fitch | BBB+ → A- |

| Alaska Air | S&P | BB → BB- |

| Baltimore Gas and Electric | S&P | A → A- |

| Banca Popolare dell'Alto Adige | Fitch | BB+ → BBB- |

| Banco Itau Chile | S&P | BBB+ → A- |

| C&D Technologies | S&P | B- → CCC |

| Centerfield Media Parent | S&P | CCC+ → B- |

| China Vanke | Fitch | RD → CC |

| Coherent | S&P | BB- → BB |

| Conduent | S&P | B → B- |

| Corp Service | Fitch | BB → BB+ |

| Domtar | S&P | B → CCC+ |

| Eli Lilly & | S&P | A+ → AA- |

| Energisa Minas Rio -Distribuidora De Energia | Fitch | BB+ → BB |

| Energisa Paraiba - Distribuidora de Energia | Fitch | BB+ → BB |

| Energisa S/A | Fitch | BB+ → BB |

| Energisa Sergipe-Distribuidora de Energia | Fitch | BB+ → BB |

| EVOCA | S&P | B- → CCC+ |

| Expleo Group SAS | Fitch | B- → CCC+ |

| First Pacific | S&P | BBB- → BBB |

| Frontera Energy | S&P | B+ → B |

| Grupo Antolin Irausa | S&P | B- → CCC+ |

| Infrabel | S&P | AA → AA- |

| Itau Chile New York Branch | S&P | BBB+ → A- |

| Kapital Bank | S&P | BB- → BB |

| Kosmos Energy | Fitch | CCC+ → B- |

| Las Vegas Sands | S&P | BBB- → BBB |

| LSF9 Canto Investments | S&P | B- → CCC+ |

| Lumentum | S&P | B → B+ |

| Madison IAQ | S&P | B → BB- |

| Marina Bay Sands Pte | S&P | BBB- → BBB |

| Novo Banco | Fitch | BBB → A- |

| Poseidon Bidco SASU | S&P | CCC+ → SD |

| S&S | S&P | B → B- |

| Sands China | S&P | BBB- → BBB |

| SK hynix | Fitch | BBB → BBB+ |

| Specialty Building Products | S&P | B → B- |

| SPIE | Fitch | BB+ → BBB- |

| Transtelecom | S&P | B → B+ |

| Tullow Oil | S&P | CC → D |

| VML US Finance | S&P | BBB- → BBB |

| WMB | Fitch | BB → BB+ |

New bond issuance remained active, especially in the US market. Investment-grade companies brought a large amount of new debt, but demand stayed solid as higher yields continued to attract investors. This helped the market absorb heavy supply without major pressure on spreads. High-yield issuance also improved, showing that the market remains open even for riskier borrowers.

| Issuer | Size | Term | Yield | Risk Level |

| A&K Travel Group Holdings | USD 0,70bn |

7Y | 7,5% | Very High |

|

ISIN (CUSIP)

USG0015BAA91

|

||||

| Accorinvest Group | EUR 0,40bn |

5Y | 5,4% | Very High |

|

ISIN (CUSIP)

XS3049459749

|

||||

| Aegon Funding Company | USD 0,50bn |

10Y | 5,7% | Medium |

|

ISIN (CUSIP)

US00775VAB09

|

||||

| Aeroporti Di Roma Spa | EUR 0,75bn |

7Y | 3,7% | Medium |

|

ISIN (CUSIP)

XS3067397789

|

||||

| Alexandrite Monnet Uk Holdco | EUR 0,47bn |

5Y | 6,9% | High |

|

ISIN (CUSIP)

XS3350943018

|

||||

| Alpha Bank | EUR 0,60bn |

6Y | 3,8% | Medium |

|

ISIN (CUSIP)

XS3357187809

|

||||

| Alphabet | EUR 1,5bn |

8Y | 3,1% | Very Low |

|

ISIN (CUSIP)

XS3064423174

|

||||

| American Express | USD 1,8bn |

4Y | 4,4% | Low |

|

ISIN (CUSIP)

US025816ET20

|

||||

| Arkea Home Loans Sfh | EUR 0,75bn |

6Y | 3,3% | Very Low |

|

ISIN (CUSIP)

FR00140182I0

|

||||

| Banco Bilbao Vizcaya Argentaria | USD 2,2bn |

5Y, PERP | 5,0–7,1% | Medium |

|

ISIN (CUSIP)

US05946KAX90…US05946KAW18

|

||||

| Banco Nacional De Mexico Integrante Del Grupo Financiero Banamex | USD 1,3bn |

10Y | 6,7% | Medium |

|

ISIN (CUSIP)

USP1S8TDFJ81

|

||||

| Brixmor Operating Partnership | USD 0,40bn |

10Y | 5,4% | Medium |

|

ISIN (CUSIP)

US11120VAQ68

|

||||

| Cbre Group | USD 0,75bn |

PERP | 5,4% | Medium |

|

ISIN (CUSIP)

US12505BAM28

|

||||

| China Water Affairs Group | USD 0,15bn |

4Y | 7,1% | High |

|

ISIN (CUSIP)

XS3201944314

|

||||

| Coca-Cola Europacific Partners | EUR 0,60bn |

6Y | 3,6% | Low |

|

ISIN (CUSIP)

XS3367599860

|

||||

| Consumers Energy (Cms_Pb.N) | USD 0,85bn |

10Y | 5,1% | Low |

|

ISIN (CUSIP)

US210518EA04

|

||||

| Cooperatieve Rabobank Ua | EUR 0,75bn |

10Y | 4,0% | Very Low |

|

ISIN (CUSIP)

XS3364887615

|

||||

| Cosmos | USD 1,00bn |

5Y | 9,0% | High |

|

ISIN (CUSIP)

USU81257AA27

|

||||

| Dexia (Paris) | EUR 1,5bn |

5Y | 3,3% | Low |

|

ISIN (CUSIP)

XS3364790611

|

||||

| Edison International | USD 0,50bn |

2Y | 5,1% | Medium |

|

ISIN (CUSIP)

US281020BE62

|

||||

| Elia Group | EUR 0,90bn |

PERP | 4,8% | Very High |

|

ISIN (CUSIP)

BE6373697216

|

||||

| Emirates Nbd Bank Pjsc | USD 0,75bn |

PERP | 6,2% | Very High |

|

ISIN (CUSIP)

XS3357228504

|

||||

| European Financial Stability Facility | EUR 3,0bn |

7Y | 3,2% | Very Low |

|

ISIN (CUSIP)

EU000A2SCAZ3

|

||||

| Firstcash | USD 0,75bn |

8Y | 6,1% | High |

|

ISIN (CUSIP)

USU3195CAD12

|

||||

| Generadora De Gatun | USD 1,0bn |

18Y | 6,9% | Medium |

|

ISIN (CUSIP)

USP46224AA20

|

||||

| Guardian Life Global Funding | USD 0,60bn |

7Y | 4,9% | Very Low |

|

ISIN (CUSIP)

US40139MBQ33

|

||||

| Hamburg Free And Hanseatic, City Of | EUR 0,50bn |

5Y | 3,0% | Very Low |

|

ISIN (CUSIP)

DE000A3MQTS5

|

||||

| Hexcel | USD 0,40bn |

5Y | 4,9% | Medium |

|

ISIN (CUSIP)

US428291AQ19

|

||||

| Hut 8 Dc | USD 3,2bn |

17Y | 6,2% | Medium |

|

ISIN (CUSIP)

USU43898AA06

|

||||

| Intel | USD 6,5bn |

5–40Y | 4,7–6,2% | Medium |

|

ISIN (CUSIP)

US458140CQ17…US458140CV02

|

||||

| Jpmorgan Chase | USD 3,0bn |

PERP | 6,1% | Very Low |

|

ISIN (CUSIP)

US48128BAR24

|

||||

| Jsc National Company Qazaqgaz / Kaztransgaz Ao | USD 0,70bn |

10Y | 5,9% | Medium |

|

ISIN (CUSIP)

XS3366268384

|

||||

| Kookmin Bank | USD 0,70bn |

3–5Y | 4,3%; FLOAT, +48bp | Low |

|

ISIN (CUSIP)

USY2350DER36

|

||||

| Kuwait, State Of (Gvd-Kw) | USD 0,80bn |

PERP | 6,4% | Medium |

|

ISIN (CUSIP)

XS3076918419

|

||||

| Lansforsakringar Bank Ab | EUR 0,50bn |

5Y | 3,5% | Low |

|

ISIN (CUSIP)

XS3366141128

|

||||

| Lsf12 Pillar Investments (Us) | EUR 0,75bn |

7Y | 5,8% | Very High |

|

ISIN (CUSIP)

XS3368834159

|

||||

| Lutech Spa | EUR 0,40bn |

5Y | 8,1% | Very High |

|

ISIN (CUSIP)

XS3363444178

|

||||

| Lv Bonds | GBP 0,15bn |

20Y | 7,5% | Very High |

|

ISIN (CUSIP)

XS3336934701

|

||||

| Meta Platforms | USD 16,0bn |

7–40Y | 4,9–6,3% | Very Low |

|

ISIN (CUSIP)

US30303MAG78…US30303MAK80

|

||||

| Muenchener Hypothekenbank Eg | EUR 0,10bn |

5Y | 3,0% | Very Low |

|

ISIN (CUSIP)

DE000MHB40J0

|

||||

| Mundys Spa | EUR 0,50bn |

6Y | 4,5% | High |

|

ISIN (CUSIP)

XS3367640680

|

||||

| National Bank Of Kuwait Sakp | USD 0,80bn |

PERP | 6,4% | Medium |

|

ISIN (CUSIP)

XS3076918419

|

||||

| National Rural Utilities Cooperative Finance | USD 0,45bn |

10Y | 4,1% | Low |

|

ISIN (CUSIP)

US63743HGF38

|

||||

| North-Rhine Westphalia, State Of | EUR 2,2bn |

10Y | 3,4% | Very Low |

|

ISIN (CUSIP)

DE000NRW0QM7

|

||||

| Oxford Finance | USD 0,60bn |

5Y | 7,8% | High |

|

ISIN (CUSIP)

US69145LAE48

|

||||

| Powszechna Kasa Oszczednosci Bank Polski | EUR 0,70bn |

4Y | 3,8% | Medium |

|

ISIN (CUSIP)

XS3296830444

|

||||

| Pr Rno Property Owner I | USD 4,6bn |

5Y | 6,7% | High |

|

ISIN (CUSIP)

USU7446DAA38

|

||||

| Schlumberger Investment | USD 2,0bn |

5–10Y | 4,6–5,2% | Low |

|

ISIN (CUSIP)

US806854AN59…US806854AQ80

|

||||

| Seb Ab | EUR 1,0bn |

5Y | 3,4% | Very Low |

|

ISIN (CUSIP)

XS3367253567

|

||||

| Serbia, Republic Of | EUR 1,9bn |

5–12Y | 4,4–5,2% | High |

|

ISIN (CUSIP)

XS3363425383…XS3363425466

|

||||

| Serbia, Republic Of | USD 1,2bn |

10Y | 5,8% | High |

|

ISIN (CUSIP)

XS3363387351

|

||||

| Serica Energy | USD 0,30bn |

5Y | 7,9% | Very High |

|

ISIN (CUSIP)

NO0013742163

|

||||

| Sfil | EUR 1,0bn |

7Y | 3,6% | Very Low |

|

ISIN (CUSIP)

FR0014018BH9

|

||||

| Shawbrook Group | GBP 0,25bn |

PERP | 8,4% | Very High |

|

ISIN (CUSIP)

XS3351070555

|

||||

| Shui On Development | USD 0,15bn |

3Y | 9,5% | Very High |

|

ISIN (CUSIP)

XS3040578745

|

||||

| Sk On | USD 0,50bn |

3Y | 4,4% | Very Low |

|

ISIN (CUSIP)

XS3361215315

|

||||

| Swiss Life Finance I | EUR 0,50bn |

7Y | 3,7% | Very High |

|

ISIN (CUSIP)

CH1548688378

|

||||

| United Group Bv | EUR 0,62bn |

7Y | 6,4% | Very High |

|

ISIN (CUSIP)

XS3367705640

|

||||

| Volvo Treasury Ab | EUR 0,50bn |

3Y | 3,2% | Low |

|

ISIN (CUSIP)

XS3364827983

|

||||

| Walmart | USD 3,9bn |

3–10Y | 4,0–4,8% | Very Low |

|

ISIN (CUSIP)

US931142FS73…US931142FV03

|

||||

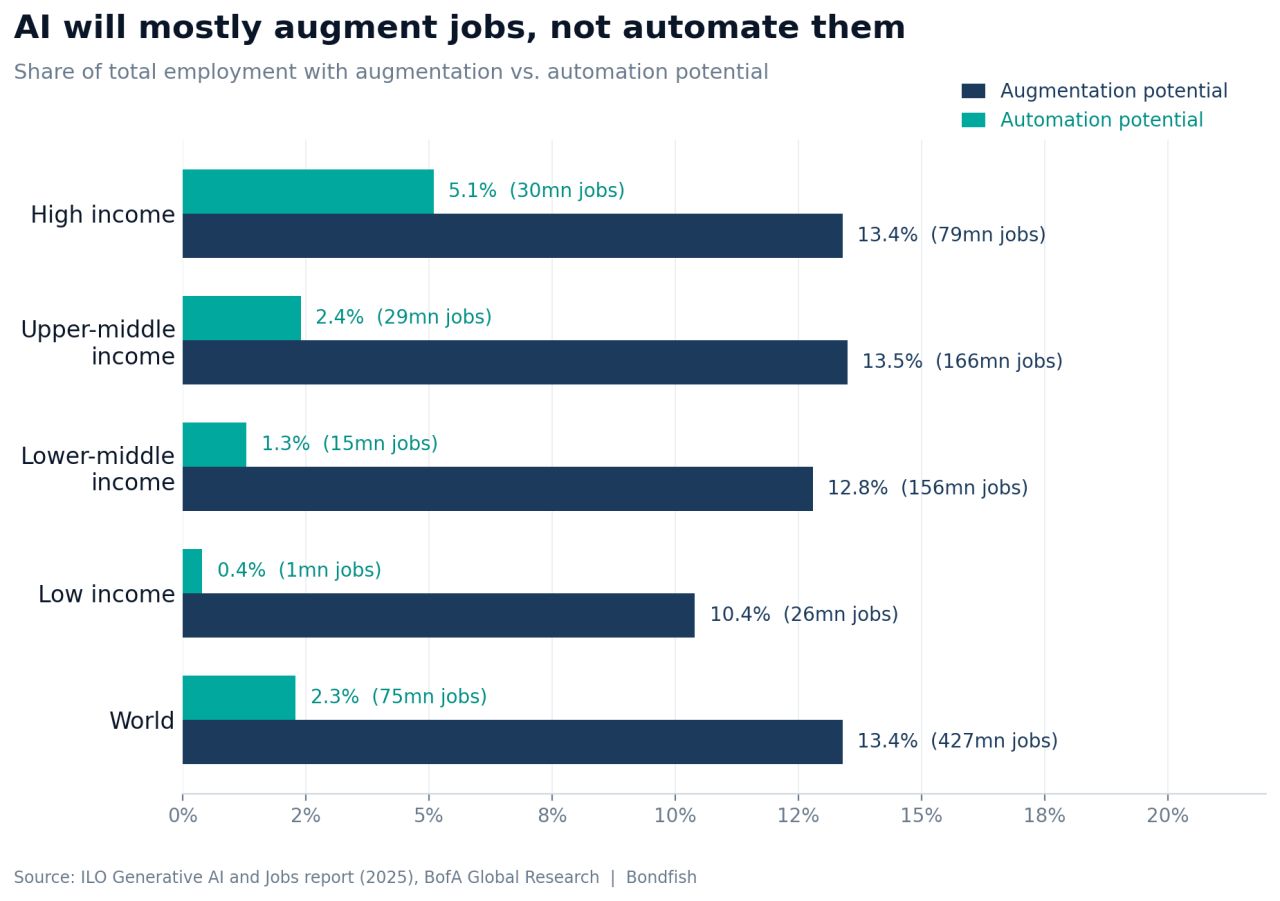

According to ILO research, roughly 24% of global jobs are exposed to AI — but augmentation outweighs automation by nearly 6:1 (427mn jobs enhanced vs. 75mn at risk). The implication for bonds? Long-term inflation expectations have been falling since late 2023, even through tariffs and wars. Markets appear to be pricing in a disinflationary AI productivity boom. More productivity = lower costs = lower long-term rates. That may be why long rates volatility is suppressed despite all the serious inflationary pressures.