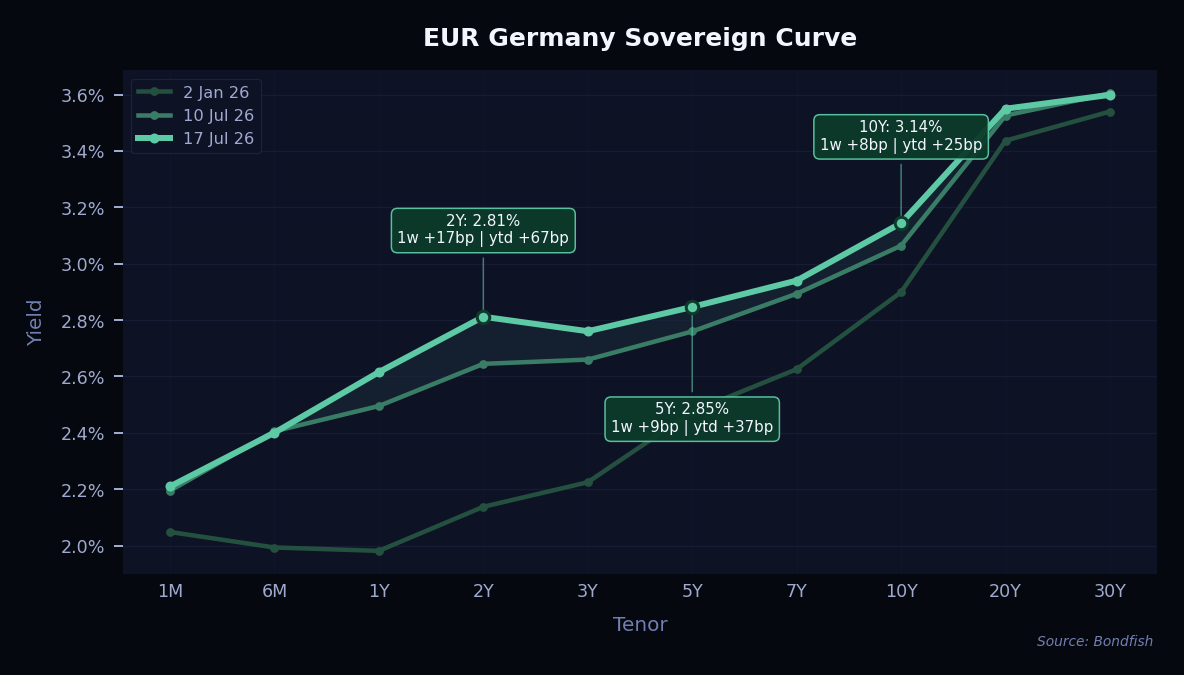

German yields rose across the curve, and the biggest move was at the short end — the 2-year climbed 17 basis points to 2.81%. The jump in oil and gas prices revived inflation worries, and heavy government bond supply added to the pressure. The 10-year finished at 3.14%, up 8 basis points on the week.

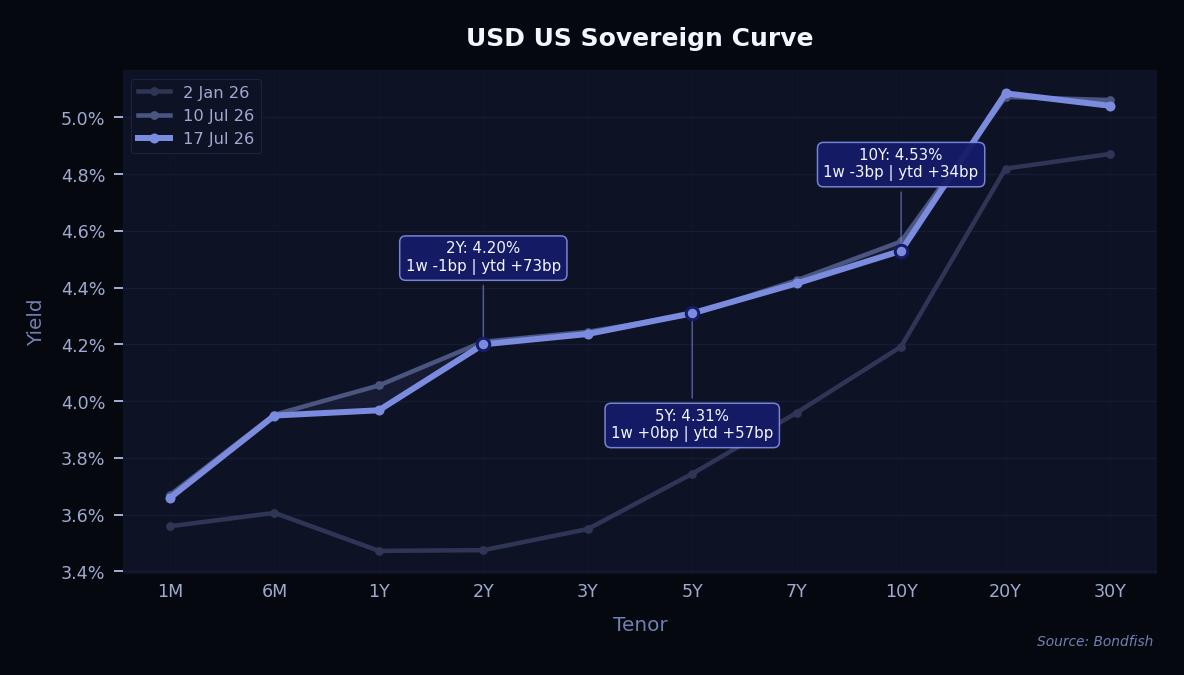

US yields barely moved, and the long end slipped a little. The 10-year eased 3 basis points to 4.53% and the 2-year was down 1 basis point at 4.20%. A sharp drop in semiconductor shares pulled some money into Treasuries as a safe haven, which offset the inflation signal from higher oil and left the curve broadly steady.

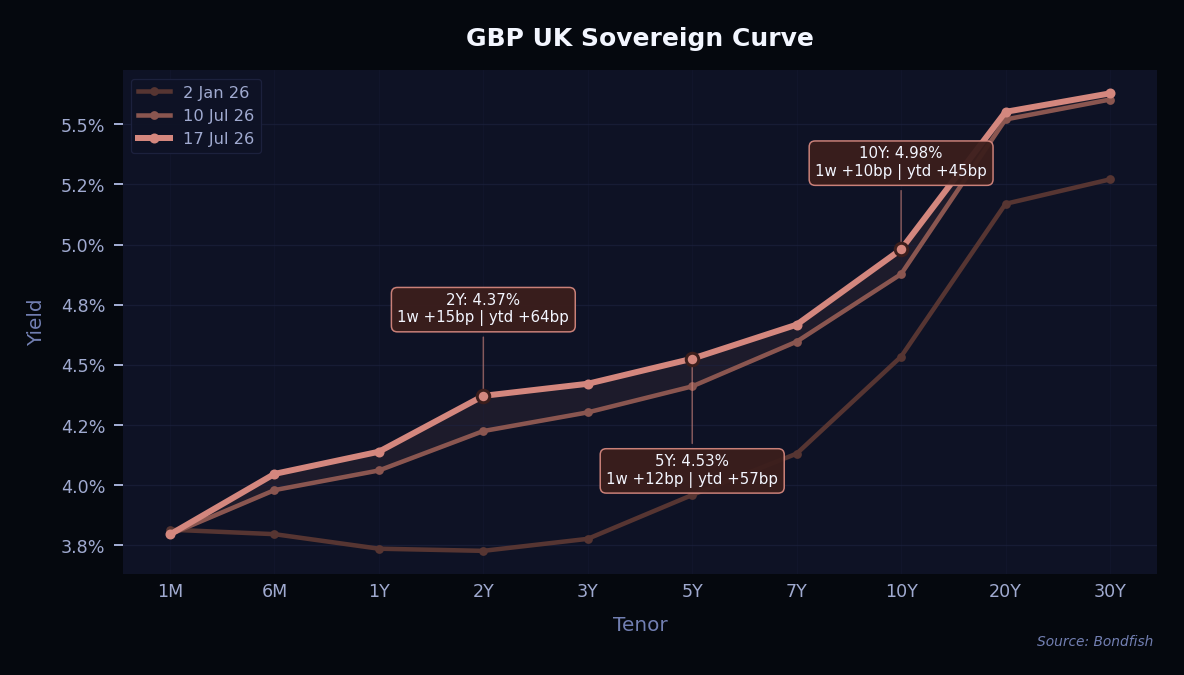

UK yields rose all along the curve. The 2-year gained 15 basis points to 4.37% and the 10-year added 10 basis points to 4.98%. Higher energy prices and still-sticky inflation kept the pressure on gilts, and investors trimmed their bets on near-term rate cuts.

With supply heavy and inflation still sticky, the favoured stance stays defensive — keeping duration on the shorter side and earning income from high-quality bonds rather than reaching for the longest maturities.

The week's standout was PayPal's 3.25% 2050 bond, a long-dated high-grade name that jumped 12.1%. High-yield industrials rebounded broadly: both Ineos Quattro Fin 2 bonds rose (up 4.3% and 3.3%), joined by Ineos Finance (+1.7%), Kohl's (+2.4%), Domtar (+2.4%) and Kronos International (+1.7%). Howard University's 2051 bond gained 4.5%, and higher-rated names Athene Global (+1.8%) and Stora Enso (+1.7%) rounded out the list.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| PayPal Hldg 3.25% Jun 2050 | USD | 12,14% | 5,39% | Low |

| Howard Uni 4.756% Oct 2051 | USD | 4,53% | 6,49% | Medium |

| Ineos Quattro Fin 2 6.75% Apr 2030 | EUR | 4,29% | 11,44% | Very High |

| Ineos Quattro Fin 2 8.5% Mar 2029 | EUR | 3,33% | 11,18% | Very High |

| Kohls 6.875% Dec 2037 | USD | 2,41% | 9,25% | Very High |

| Domtar 6.75% Oct 2028 | USD | 2,39% | 23,48% | Very High |

| Athene Global 5.543% Aug 2035 | USD | 1,79% | 5,50% | Low |

| Stora Enso 7.25% Apr 2036 | USD | 1,73% | 5,72% | Medium |

| Kronos Intnl 9.5% Mar 2029 | EUR | 1,70% | 10,21% | Very High |

| Ineos Finance 5.625% Aug 2030 | EUR | 1,67% | 6,96% | High |

The falls were concentrated in high-yield telecom, where all three Virgin Media bonds dropped — Virgin Media Fin (-4.7%), Virgin Media O2 (-3.3%) and Vmed UK (-2.9%). Community Health Systems (-3.1%) and Flagstar Bank (-2.9%) also declined. Longer-dated bonds felt the rise in yields most: Northumbrian Water (-2.7%), Paramount Global (-2.5%) and Harley-Davidson (-2.4%) all slid, along with Places for People and even the very-low-risk European Financial Stability Facility bond (-2.4%).

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| Virgin Media Fin 3.75% Jul 2030 | EUR | -4,74% | 11,18% | Very High |

| Virgin Media O2 7.875% Mar 2032 | GBP | -3,32% | 13,21% | Very High |

| Community Health Systems 6.125% Apr 2030 | USD | -3,09% | 9,90% | Very High |

| Places Peopl 3.901% Dec 2034 | EUR | -3,00% | 4,47% | Low |

| Flagstar Bnk 7.574% Nov 2030 | USD | -2,93% | 19,31% | High |

| Vmed UK 3.25% Jan 2031 | EUR | -2,93% | 6,83% | High |

| Northumbrian Wtr 6.875% Apr 2045 | GBP | -2,65% | 7,00% | Medium |

| Paramount Global 5.9% Oct 2040 | USD | -2,46% | 9,06% | High |

| Harley Davidson 4.625% Jul 2045 | USD | -2,42% | 6,76% | Medium |

| European Fin Stability 2.75% Dec 2029 | EUR | -2,39% | 2,97% | Very Low |

Note: only long-term senior unsecured ratings were taken into account.

Upgrades edged out downgrades, 16 to 14. The biggest jump came from Chart Industries, lifted several notches by S&P to A-, while Ford Bank, KeyCorp and KeyBank all won higher marks from Moody's and Banco BPI moved up to A+. On the downside, HSBC Bank Uruguay was cut three notches to BB+, Baker Hughes slipped to A-, and KB Home, Cornerstone OnDemand and PECO Energy were all lowered. Sirona fell to selective default.

| Issuer | Agency | Change |

| Ammega | Fitch | B- → CCC+ |

| Baker Hughes | S&P | A → A- |

| Banco BPI | Fitch | A → A+ |

| Banistmo | S&P | BB- → BB |

| Bright Food International | S&P | BBB- → BBB |

| Chart Industries | S&P | BB- → A- |

| Co-Operative Bank | Fitch | A+ (new) |

| Cornerstone OnDemand | S&P | B- → CCC+ |

| Eagle Broadband Investments | S&P | B+ → B |

| Eurotelesites | Fitch | BBB- → BBB |

| Ford Bank | Moody's | Baa1 → A3 |

| Forgent Power | S&P | B → B+ |

| HSBC Bank Uruguay | Fitch | BBB+ → BB+ |

| Janus Henderson US | Fitch | BB+ (new) |

| KB Home | S&P | BB+ → BB |

| Keybank National Association | Moody's | Baa1 → A3 |

| KeyCorp | Moody's | Baa2 → Baa1 |

| M/I Homes | S&P | BB → BB+ |

| Medical Solutions Parent | S&P | D → CCC+ |

| Mega Broadband Investments Intermediate I | S&P | B+ → B |

| Neuraxpharm | S&P | B → B- |

| PECO Energy | Moody's | A2 → A3 |

| Petroquimica Comodoro Rivadavia | S&P | B (new) |

| Project Boost Purchaser | S&P | B- → B |

| Project Leopard | Fitch | B- → CCC |

| Sirona | S&P | CCC → SD |

| Tungsten Cayco | Fitch | B- → CCC |

| Urumqi Gaoxin Investment and Development | Fitch | BB+ → BBB- |

| Uzmetkombinat OAO | Fitch | B+ → B |

| Victoria | S&P | CCC+ → CCC- |

It was a heavy week for high-grade supply, led by financials. JPMorgan Chase, Morgan Stanley, Goldman Sachs, Mitsubishi UFJ and PNC all printed multi-tranche dollar deals. Supranationals and agencies were busy too — the International Bank for Reconstruction and Development, Export Development Canada, New Development Bank and African Export-Import Bank all came to market — alongside sovereigns including the United Kingdom and Serbia. Demand stayed firm even with oil prices spiking and volatility rising elsewhere, with investors leaning toward high-quality, longer-dated bonds.

| Issuer | Size | Term | Yield | Risk Level |

| African Export Import Bank | USD 1,5bn |

6–10Y | 6,2–7,1% | Medium |

|

ISIN (CUSIP)

XS3437376703…XS3437376612

|

||||

| Anhui Transportation Holding Group HK | USD 0,40bn |

3Y | 4,3% | Low |

|

ISIN (CUSIP)

XS3435193381

|

||||

| Australia and New Zealand Banking Group | GBP 1,2bn |

4Y | FLOAT, +50bp | Very Low |

|

ISIN (CUSIP)

XS3449093007

|

||||

| Bank of New York Mellon | USD 0,50bn |

PERP | 6,2% | Medium |

|

ISIN (CUSIP)

US064058AW09

|

||||

| Bayer US Finance | USD 5,0bn |

5–30Y | 5,1–6,4% | Medium |

|

ISIN (CUSIP)

USU07264AN10…USU07264AQ41

|

||||

| Beusa Investments | USD 0,80bn |

5Y | 7,0% | Very High |

|

ISIN (CUSIP)

USU0877JAA35

|

||||

| Carrix | USD 2,5bn |

7Y | 6,1% | Medium |

|

ISIN (CUSIP)

USU1453NAA47

|

||||

| China CITIC Bank International | USD 0,40bn |

PERP | 5,0% | High |

|

ISIN (CUSIP)

XS3371242911

|

||||

| Conceria Pasubio SpA | EUR 0,40bn |

6Y | 9,5% | Very High |

|

ISIN (CUSIP)

XS3445916524

|

||||

| Corelogic | USD 2,5bn |

5–6Y | 9,0–13,3% | Very High |

|

ISIN (CUSIP)

USU20621AC97…USU20621AD70

|

||||

| Distrito Especial Industrial y Portuario de Barranquilla | USD 0,35bn |

5Y | 7,3% | High |

|

ISIN (CUSIP)

USP3600PAD70

|

||||

| Export Development Canada | USD 2,0bn |

5Y | 4,3% | Very Low |

|

ISIN (CUSIP)

US30216BKT88

|

||||

| Export-Import Bank of Korea | USD 2,0bn |

3–5Y | 4,5–4,6% | Very Low |

|

ISIN (CUSIP)

US302154EV78…US302154EW51

|

||||

| GA Global Funding | USD 0,40bn |

5Y | 5,5% | Low |

|

ISIN (CUSIP)

US36143M2X01

|

||||

| Goldman Sachs Group | EUR 5,0bn |

4–8Y | 3,6–4,1%; FLOAT | Low |

|

ISIN (CUSIP)

XS3447651202…XS3447651111

|

||||

| Goldman Sachs Group | USD 10,0bn |

6–31Y | 5,2–6,2% | Low |

|

ISIN (CUSIP)

US38145GAV23…US38145GAX88

|

||||

| Heico | USD 1,2bn |

10Y, PERP | 5,0–5,4% | Medium |

|

ISIN (CUSIP)

422806AC3…422806AD1

|

||||

| Iliad | EUR 0,65bn |

5Y | 4,1% | High |

|

ISIN (CUSIP)

FR0014019WY8

|

||||

| International Bank for Reconstruction and Development | USD 1,5bn |

7Y | FLOAT, +38bp | Very Low |

|

ISIN (CUSIP)

US459058MB69

|

||||

| Intrum Investments and Financing AB | EUR 0,53bn |

5Y | 7,0% | Very High |

|

ISIN (CUSIP)

XS3438544630

|

||||

| Jinko Power (HK) | USD 0,10bn |

3Y | 4,4% | Very High |

|

ISIN (CUSIP)

XS3408475476

|

||||

| John Deere Bank | EUR 0,60bn |

4Y | 3,4% | Low |

|

ISIN (CUSIP)

XS3438591128

|

||||

| JPMorgan Chase | USD 9,0bn |

4–15Y | 4,9–5,8%; FLOAT | Very Low |

|

ISIN (CUSIP)

US48128BAV36…US48128BAT89

|

||||

| Kennedy Wilson | USD 0,30bn |

7Y | 7,0% | Very High |

|

ISIN (CUSIP)

USU49454AG37

|

||||

| Korea Electric Power | USD 0,70bn |

3–5Y | 4,9%; FLOAT, +62bp | Very Low |

|

ISIN (CUSIP)

USY4907LAU62

|

||||

| KT&G | USD 0,30bn |

4Y | 4,9% | Low |

|

ISIN (CUSIP)

XS3428230844

|

||||

| Massachusetts Electric | USD 0,60bn |

30Y | 6,2% | Medium |

|

ISIN (CUSIP)

USU57467AE94

|

||||

| Mitsubishi HC Finance America | USD 0,50bn |

5Y | 5,2% | Low |

|

ISIN (CUSIP)

USU6S68YAK42

|

||||

| Mitsubishi UFJ Financial Group | USD 3,0bn |

4–21Y | 5,0–6,0%; FLOAT | Low |

|

ISIN (CUSIP)

US606822DZ48…US606822ED27

|

||||

| Morgan Stanley | USD 6,5bn |

3–11Y | 5,2–5,6%; FLOAT | Low |

|

ISIN (CUSIP)

US61748UBA97…US61748UBB70

|

||||

| New Development Bank | USD 1,8bn |

3Y | 4,4% | Very Low |

|

ISIN (CUSIP)

XS3425662601

|

||||

| Nonghyup Bank | USD 0,60bn |

4–5Y | 4,7%; FLOAT, +60bp | Very Low |

|

ISIN (CUSIP)

USY6396XAM12

|

||||

| Paragon Banking Group | GBP 0,20bn |

10Y | 6,5% | Medium |

|

ISIN (CUSIP)

XS3392880038

|

||||

| PNC Financial Services Group | USD 2,0bn |

4–11Y | 4,8–5,5% | Low |

|

ISIN (CUSIP)

US693475CL76

|

||||

| Sba Communications | USD 3,5bn |

3–7Y | 5,1–5,6% | Medium |

|

ISIN (CUSIP)

US78410GAH74…US78410GAK04

|

||||

| Republic of Serbia | EUR 0,50bn |

6Y | 4,8% | Very High |

|

ISIN (CUSIP)

XS3436151750

|

||||

| SMBC Aviation Capital Finance | USD 2,0bn |

3–10Y | 5,0–5,7% | Medium |

|

ISIN (CUSIP)

USG82296AR85…USG82296AQ03

|

||||

| Standard Life | GBP 0,35bn |

PERP | 7,4% | Medium |

|

ISIN (CUSIP)

XS3435285070

|

||||

| Tata Capital | USD 0,40bn |

4Y | 5,3% | Very High |

|

ISIN (CUSIP)

XS3436154341

|

||||

| Turkiye Is Bankasi | USD 0,50bn |

12Y | 8,4% | Very High |

|

ISIN (CUSIP)

XS3431962532

|

||||

| United Kingdom of Great Britain and Northern Ireland | GBP 4,8bn |

12Y | 2,1% | Very Low |

|

ISIN (CUSIP)

GB00BMY62Z61

|

||||

| Validus Energy II Midcon | USD 0,50bn |

5Y | 8,0% | Very High |

|

ISIN (CUSIP)

USU9100XAA29

|

||||