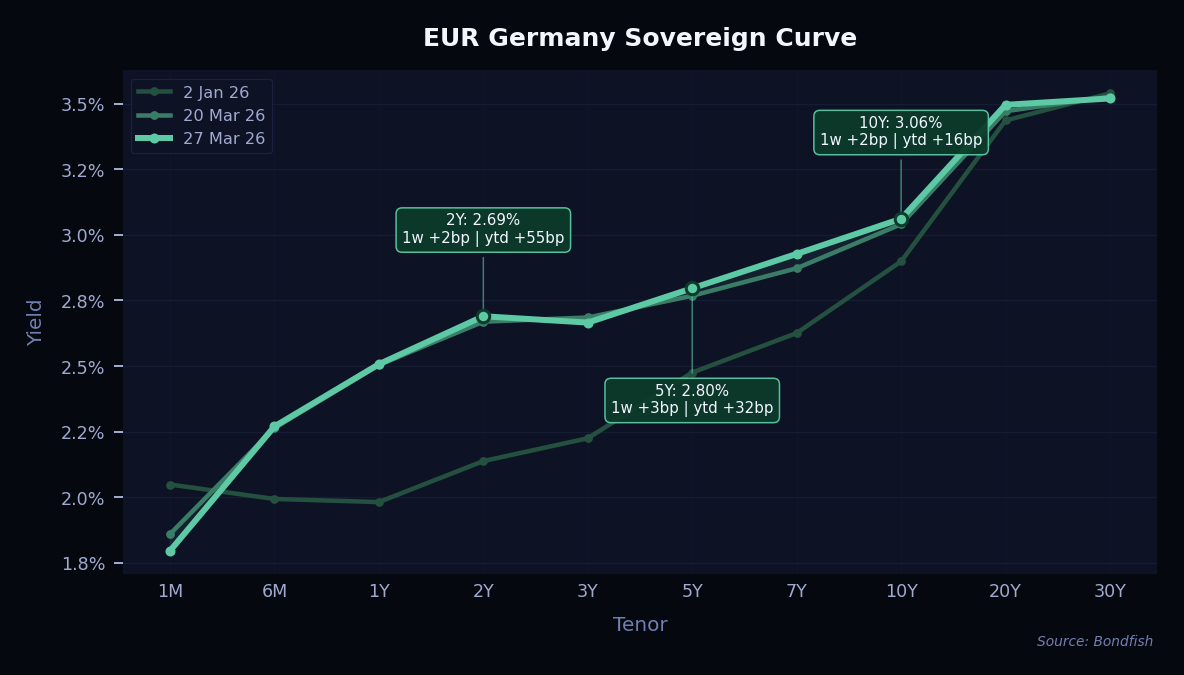

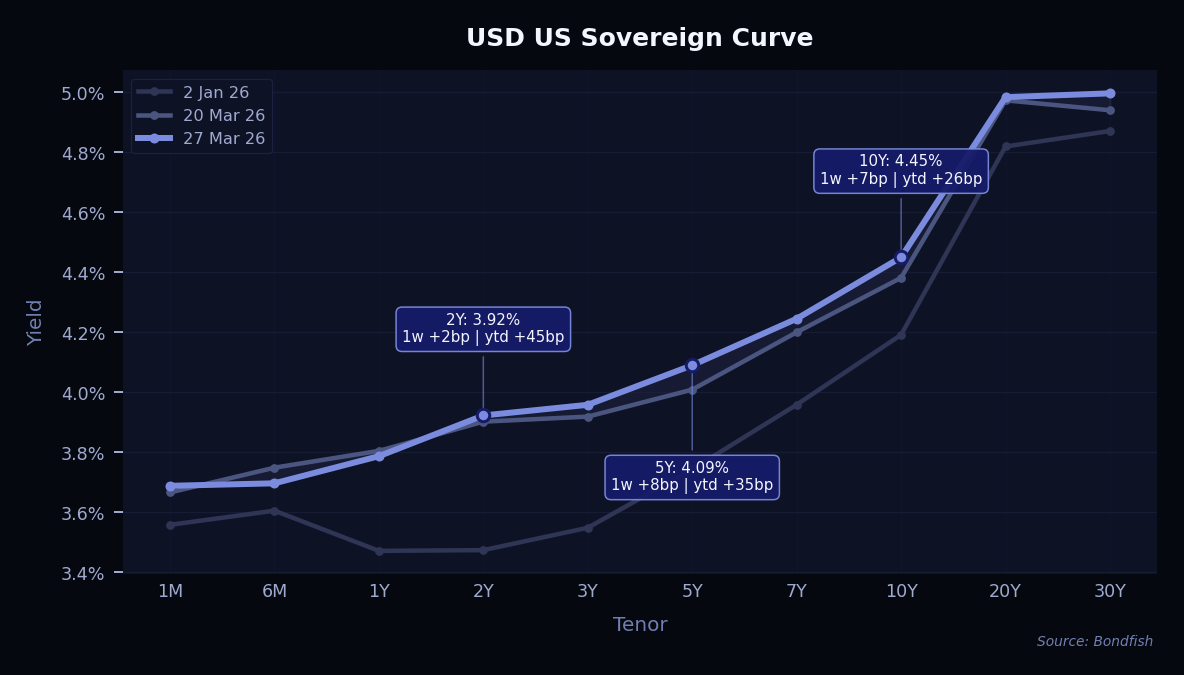

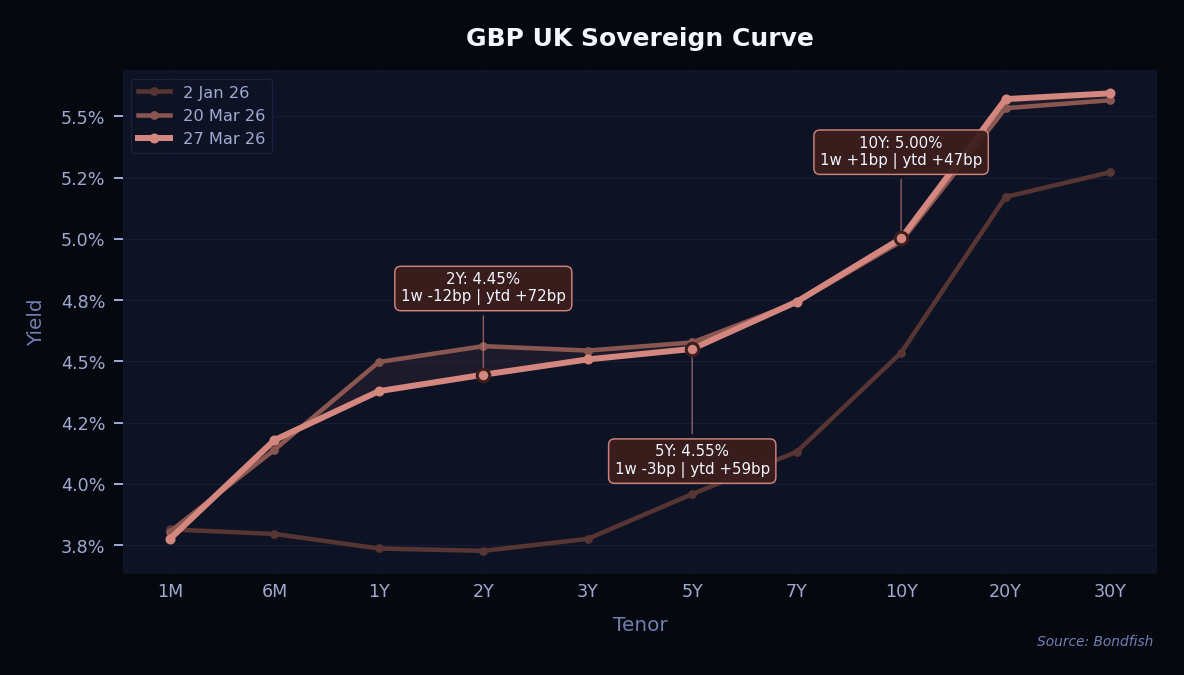

Developed market yield curves were little changed overall last week, even though energy prices and Middle East headlines remained the main themes in the background. Moves were modest across the US, UK and Germany, with most key tenors changing only slightly over the week.

The broader message is that bond markets are still sensitive to oil, gas and geopolitical developments, especially in Europe, where energy prices matter more for inflation. In this kind of environment, a cautious overall stance still seems appropriate, as rate moves remain closely tied to developments that are hard to predict.

Credit markets were relatively stable last week despite a cautious risk environment. Investment-grade bonds held up well, even as equities weakened and high-yield spreads widened slightly. This suggests that demand for higher-quality bonds remained solid.

One key factor was the level of yields. Higher yields continued to attract buyers, helping absorb a large amount of new bond issuance. At the same time, fund inflows slowed and some outflows appeared, showing that investor sentiment became more cautious.

Below are the bonds with the strongest weekly price appreciation.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| Bausch Health 5% Jan 2028 | USD | 5.33% | 13.93% | VeryHigh |

|

Reason

Clinical trial success and potential merger speculation.

|

||||

| goeasy 9.25% Dec 2028 | USD | 2.53% | 12.23% | High |

|

Reason

Lender covenant waivers secured funding access despite rising credit risks.

|

||||

| FMC 3.45% Oct 2029 | USD | 1.34% | 7.15% | Medium |

|

Reason

M&A interest and perceived undervaluation outweighed negative rating outlook.

|

||||

| Micron Tech 5.8% Jan 2035 | USD | 1.24% | 4.99% | Medium |

|

Reason

Strong earnings and tender offer.

|

||||

| Micron Tech 6.05% Nov 2035 | USD | 1.15% | 5.11% | Medium |

|

Reason

Strong earnings and tender offer.

|

||||

The following bonds experienced the sharpest weekly declines.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| Alta Equip Grp 9% Jun 2029 | USD | -4.76% | 14.09% | VeryHigh |

|

Reason

Moody's downgrade on weak construction and manufacturing demand pressured credit.

|

||||

| Service Propts 8.875% Jun 2032 | USD | -4.36% | 10.47% | VeryHigh |

|

Reason

Debt wall and refinancing risks overshadowed the REIT's strategic pivot.

|

||||

| APPLOVIN CORPORATION 5.95% Dec 2054 | USD | -3.77% | 6.76% | Medium |

|

Reason

Tech selloff and new short call hit AppLovin sentiment.

|

||||

| Bath & Body Works 6.75% Jul 2036 | USD | -3.70% | 7.55% | High |

|

Reason

Weak outlook and securities lawsuits.

|

||||

| Warnermedia Hldg 4.279% Mar 2032 | USD | -3.44% | 8.89% | High |

|

Reason

Merger antitrust scrutiny and weaker deal odds.

|

||||

| Discovery Com 5% Sep 2037 | USD | -3.43% | 9.05% | High |

|

Reason

Merger antitrust scrutiny and weaker deal odds.

|

||||

| Service Propts 4.375% Feb 2030 | USD | -3.40% | 9.89% | VeryHigh |

|

Reason

Debt wall and refinancing risks overshadowed the REIT's strategic pivot.

|

||||

| Bath & Body Works 6.875% Nov 2035 | USD | -3.23% | 7.45% | High |

|

Reason

Weak outlook and securities lawsuits.

|

||||

| Navient 5.625% Aug 2033 | USD | -3.22% | 9.90% | High |

|

Reason

Investors worried about cash flow coverage of upcoming debt maturities.

|

||||

| Kohls 5.125% May 2031 | USD | -3.22% | 12.40% | VeryHigh |

|

Reason

Weak retail performance and turnaround execution.

|

||||

Primary markets remained active last week despite geopolitical volatility. The largest transaction was the Oak-Eagle AcquireCo multi-currency financing linked to the Electronic Arts buyout. The bond portion totaled $6,6 billion and was issued in three tranches, including two secured tranches in USD and EUR, while the remainder of the financing was raised through loans. The overall package attracted more than $50 billion of investor demand and the bonds traded higher after launch. This showed that issuers can still access sizeable funding when market windows open.

More broadly, banks continue to work through a pipeline of large leveraged transactions, including additional loan and high-yield bond deals linked to acquisitions. At the same time, some planned deals were delayed due to market volatility, highlighting that timing remains sensitive. Overall, demand for new issues appears solid, but pricing concessions are often required to complete larger transactions.

| Issuer | Size | Term | Yield | Risk Level |

| Amphenol Technologies Holding Gmbh | EUR 0,50bn |

5Y | 3,7% | Low |

|

ISIN (CUSIP)

XS3316225757

|

||||

| Angola | USD 2,5bn |

7–11Y | 9,4–9,9% | Very High |

|

ISIN (CUSIP)

XS3328007797…XS3328007870

|

||||

| Apollo Global Management | USD 0,75bn |

10Y | 5,7% | Low |

|

ISIN (CUSIP)

US03769MAG15

|

||||

| Bank Of Ireland Group | EUR 0,75bn |

8Y | 4,0% | Low |

|

ISIN (CUSIP)

XS3332496184

|

||||

| Bank Of Montreal | USD 1,2bn |

5Y | 4,2% | Very Low |

|

ISIN (CUSIP)

USC0623PRG56

|

||||

| Canadian Imperial Bank Of Commerce | USD 1,2bn |

5Y | 4,2% | Very Low |

|

ISIN (CUSIP)

USC2428PBR13

|

||||

| Citadel Securities Global Holdings | USD 1,5bn |

6–10Y | 5,3–6,0% | Medium |

|

ISIN (CUSIP)

US17289RAE62…US17289RAF38

|

||||

| Coca-Cola Hbc Finance Bv | EUR 2,1bn |

2–8Y | 3,5–4,0% | Medium |

|

ISIN (CUSIP)

XS3326473694…XS3326476523

|

||||

| Commonwealth Bank Of Australia | USD 2,0bn |

3Y | 4,4%; FLOAT | Very Low |

|

ISIN (CUSIP)

US20271RAX89

|

||||

| Cooperatieve Rabobank Ua | USD 0,75bn |

3Y | 4,3% | Very Low |

|

ISIN (CUSIP)

US21688ABV35

|

||||

| Danfoss Finance I Bv | EUR 0,70bn |

7Y | 3,9% | Medium |

|

ISIN (CUSIP)

XS3326479469

|

||||

| Danone | EUR 1,2bn |

4–8Y | 3,4–3,8% | Medium |

|

ISIN (CUSIP)

FR0014017HN6…FR0014017HO4

|

||||

| Danone | GBP 0,35bn |

6Y | 5,3% | Medium |

|

ISIN (CUSIP)

FR0014017HM8

|

||||

| Danske Bank A/S | USD 1,6bn |

3–6Y | 4,7–5,0% | Low |

|

ISIN (CUSIP)

US23636BBM00…US23636BBN82

|

||||

| Dnb Bank Asa | USD 0,75bn |

6Y | 4,8% | Very Low |

|

ISIN (CUSIP)

USR1655VAH17

|

||||

| Emera Us Finance | USD 0,75bn |

3–7Y | 4,7–5,3% | Medium |

|

ISIN (CUSIP)

US29103HAC16…US29103HAD98

|

||||

| Enbridge | USD 2,0bn |

5–10Y | 4,9–5,5% | Medium |

|

ISIN (CUSIP)

US29250NCQ60…US29250NCR44

|

||||

| Fondo Mivivienda | USD 0,40bn |

5Y | 5,4% | Medium |

|

ISIN (CUSIP)

USP42009AF09

|

||||

| Glencore Funding | USD 2,5bn |

5–10Y | 4,9–5,5% | Low |

|

ISIN (CUSIP)

USU37818BY30…USU37818CA45

|

||||

| Henkel & Kgaa | EUR 1,5bn |

2–5Y | 3,6%; FLOAT, +35bp | Very High |

|

ISIN (CUSIP)

XS3319131119

|

||||

| Hta Group | USD 0,50bn |

5Y | 7,0% | High |

|

ISIN (CUSIP)

XS3312132338

|

||||

| Inmobiliaria Colonial Socimi | EUR 0,50bn |

5Y | 4,0% | Very High |

|

ISIN (CUSIP)

XS3320133781

|

||||

| IBRD | GBP 1,0bn |

6Y | FLOAT, +36bp | Very Low |

|

ISIN (CUSIP)

XS3333014747

|

||||

| Itc Holdings | USD 0,90bn |

5–10Y | 4,9–5,5% | Medium |

|

ISIN (CUSIP)

USU4501WAN21…USU4501WAP78

|

||||

| Japan Finance Organization For Municipalities | USD 0,50bn |

5Y | 4,2% | Low |

|

ISIN (CUSIP)

XS3327050244

|

||||

| Korea National Oil | USD 1,2bn |

3–5Y | 4,6–4,8%; FLOAT, +80bp | Very Low |

|

ISIN (CUSIP)

USY4938AAW90…USY4938AAY56

|

||||

| LG Energy Solution | USD 1,6bn |

3–10Y | 5,0–6,0%; FLOAT, +156bp | Medium |

|

ISIN (CUSIP)

USY5S5CGAS19…USY5S5CGAV48

|

||||

| Macquarie Bank | USD 1,2bn |

3Y | 4,5%; FLOAT | Very Low |

|

ISIN (CUSIP)

US55608RCB42

|

||||

| Munich, City Of | EUR 0,50bn |

10Y | 3,4% | Very High |

|

ISIN (CUSIP)

DE000A460HM6

|

||||

| Natwest Markets | USD 2,3bn |

3–5Y | 4,7–4,9%; FLOAT | Very Low |

|

ISIN (CUSIP)

USG6382RQG67…USG6382RQE10

|

||||

| Nexstar Media | USD 5,1bn |

8Y | 6,5–7,2% | Very High |

|

ISIN (CUSIP)

USU6500WAB47…USU6500WAA63

|

||||

| Nordea Kiinnitysluottopankki | EUR 1,0bn |

3Y | 2,9% | Very Low |

|

ISIN (CUSIP)

XS3330368518

|

||||

| Oak-Eagle AcquireCo | USD 5,38bn |

7–8Y | 7,3–8,8% | High |

|

ISIN (CUSIP)

US67124CAA18…US67124CAB90

|

||||

| Oak-Eagle AcquireCo | EUR 1,08bn |

7Y | 6,3% | High |

|

ISIN (CUSIP)

XS3323687023

|

||||

| Oklahoma Gas And Electric | USD 0,35bn |

30Y | 6,0% | Low |

|

ISIN (CUSIP)

US678858CA77

|

||||

| Pacificorp | USD 2,5bn |

10Y, PERP | 4,7–5,8% | Low |

|

ISIN (CUSIP)

US695114DM76…US695114DQ80

|

||||

| Puget Energy | USD 0,90bn |

30Y | 7,0–7,2% | High |

|

ISIN (CUSIP)

USU74592AH60…USU74592AJ27

|

||||

| Rogers Communications | USD 0,75bn |

30Y | 6,9% | Medium |

|

ISIN (CUSIP)

775109DL2

|

||||

| Royal Bank Of Canada | USD 0,75bn |

3Y | 4,1% | Very Low |

|

ISIN (CUSIP)

USC79875AA54

|

||||

| Snf Group | USD 0,75bn |

5Y | 5,6% | Medium |

|

ISIN (CUSIP)

USF8449EAA31

|

||||

| Serbia | EUR 0,50bn |

5Y | 6,5% | Very High |

|

ISIN (CUSIP)

XS3327023787

|

||||

| Sumitomo Mitsui Banking | EUR 1,0bn |

4Y | 3,5% | Low |

|

ISIN (CUSIP)

XS3320639282

|

||||

| Sumitomo Mitsui Financial Group | EUR 1,0bn |

8Y | 4,0% | Low |

|

ISIN (CUSIP)

XS3320639100

|

||||

| Tennet Netherlands Bv | EUR 2,0bn |

10Y | 3,3% | Very Low |

|

ISIN (CUSIP)

XS3329155504

|

||||

| Turkiye Halk Bankasi As | USD 0,21bn |

PERP | 8,3% | Very High |

|

ISIN (CUSIP)

XS3314690176

|

||||

| Westpac Banking | EUR 1,0bn |

5Y | 3,1% | Very Low |

|

ISIN (CUSIP)

XS3328597060

|

||||

EUR credit spreads have stayed relatively calm after the latest Middle East escalation. Investment Grade widened by less than 15 bp, which is much less than during last March’s “judgement day” repricing. At the same time, European equities fell around 10%, so credit clearly outperformed stocks. The market still seems to expect a contained conflict, not a prolonged macro shock. High yields also continue to support demand. And according to investment banks, dealer inventories in long-duration credit have fallen to record lows, which also helps explain why spreads have moved only modestly.

.png)