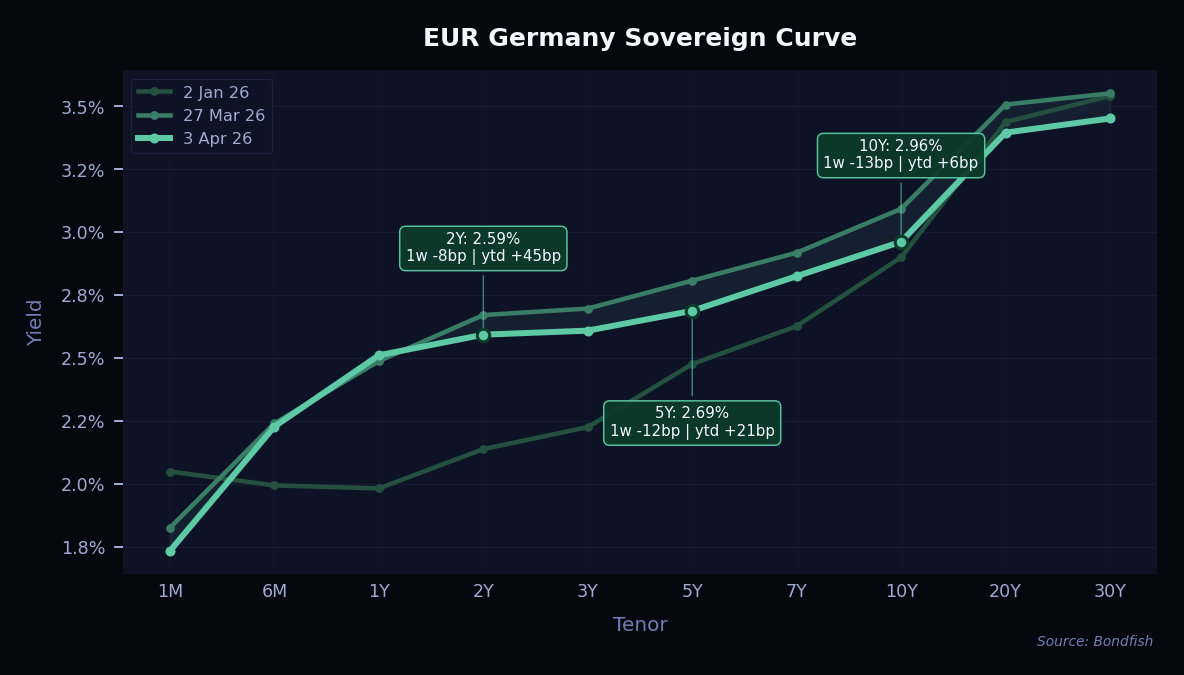

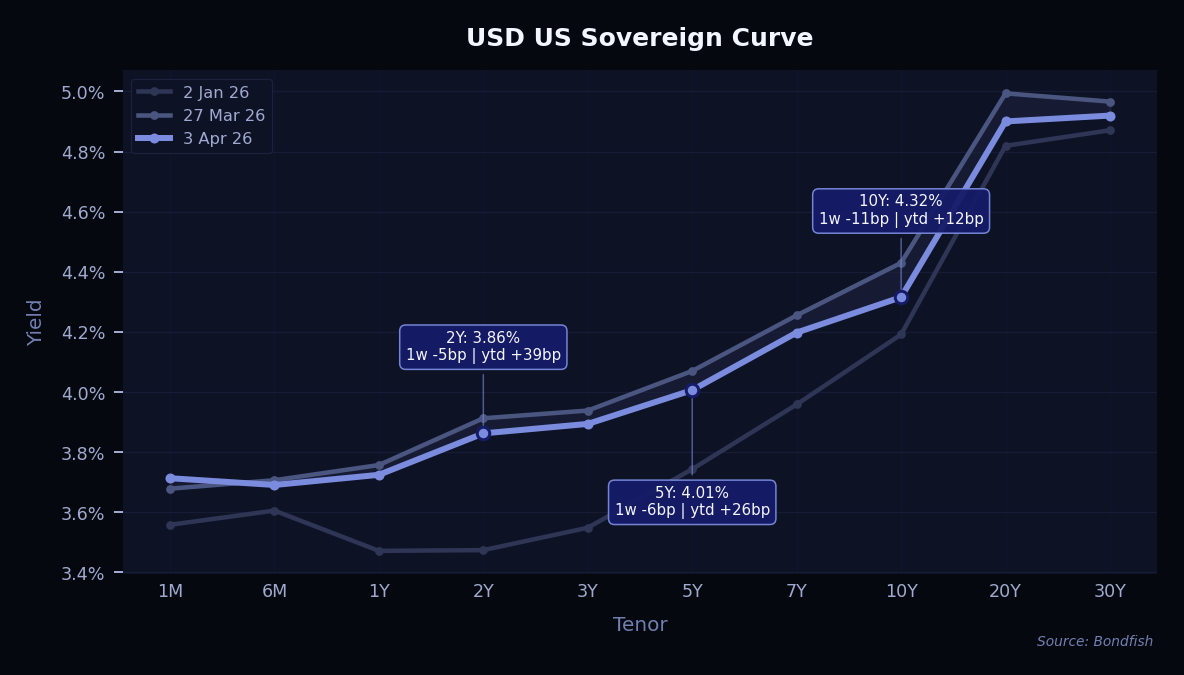

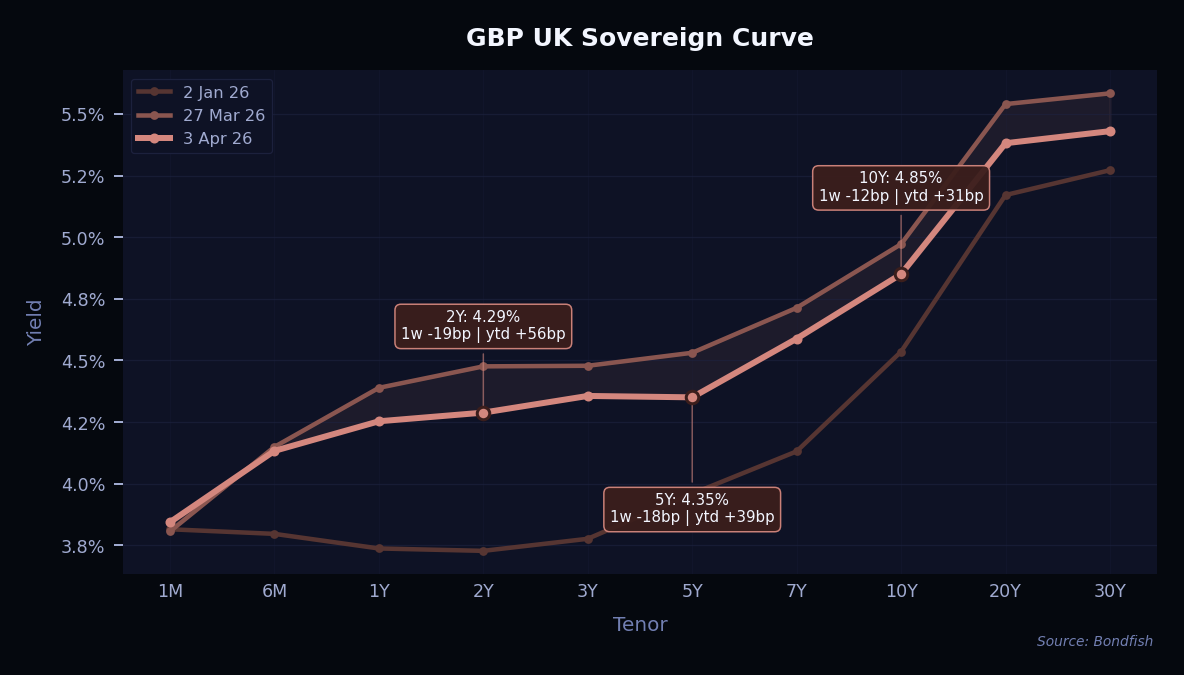

Developed market yield curves moved lower and generally steepened during the week, as investors grew more optimistic that the Middle East conflict could move closer to resolution. Falling oil prices and a weaker dollar helped ease immediate inflation concerns, while stronger equity markets supported a broader risk-on tone. This pushed yields down across the US, Europe and the UK, with longer maturities benefiting most from the drop in macro risk premium. Even so, the move was driven more by improving sentiment than by a major change in underlying fundamentals, so markets remain sensitive to any reversal in geopolitical headlines or surprises in labor and inflation data. In this environment, longer-dated high-quality bonds look somewhat more attractive after the rally in sentiment, but investors may still want to stay balanced, as rate volatility could return quickly if optimism fades.

Credit markets strengthened during the week, with significantly more gainers than losers as lower government bond yields and improving risk sentiment supported bond prices. The broad decline in curves helped duration-heavy bonds outperform, while tighter spreads were seen across many investment-grade names. High-yield bonds also saw more positive moves, as investors became more comfortable adding risk. The gains were relatively broad-based, indicating that the rally was driven more by market direction than by issuer-specific news.

Below are the bonds with the strongest weekly price appreciation.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| Service Propts 8.875% Jun 2032 | USD | 7.59% | 8.90% | VeryHigh |

|

Reason

Equity raise improved liquidity, enabled debt repayment and deleveraging.

|

||||

| Service Propts 4.95% Oct 2029 | USD | 6.97% | 7.80% | VeryHigh |

|

Reason

Equity raise improved liquidity, enabled debt repayment and deleveraging.

|

||||

| Kohls 5.125% May 2031 | USD | 6.87% | 10.83% | VeryHigh |

|

Reason

Operational improvements and product expansion boosted sentiment and bond demand.

|

||||

| Perrigo Finance 6.125% Sep 2032 | USD | 5.96% | 7.39% | High |

|

Reason

Tax dispute win and refinancing strengthened balance sheet and investor confidence.

|

||||

| Warnermedia Hldg 4.279% Mar 2032 | USD | 5.30% | 7.87% | High |

|

Reason

Merger progress supported valuation despite regulatory scrutiny.

|

||||

| Kohls 6.875% Dec 2037 | USD | 5.14% | 10.31% | VeryHigh |

|

Reason

Operational improvements and product expansion boosted sentiment and bond demand.

|

||||

| Pemex 6.75% Sep 2047 | USD | 4.97% | 8.53% | High |

|

Reason

Mixed fundamentals but improved financials and strong trading demand driven by the oil price rise.

|

||||

| Service Propts 3.95% Jan 2028 | USD | 4.81% | 6.10% | VeryHigh |

|

Reason

Equity raise improved liquidity, enabled debt repayment and deleveraging.

|

||||

| Warnermedia Hldg 4.279% Mar 2032 | USD | 4.62% | 5.98% | High |

|

Reason

Merger progress supported valuation despite regulatory scrutiny.

|

||||

| Greece 1.875% Jan 2052 | EUR | 4.44% | 4.29% | Medium |

|

Reason

High duration and modest spread repricing.

|

||||

The following bonds experienced the sharpest weekly declines.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| Mobico Group 4.875% Sep 2031 | EUR | -2.23% | 9.97% | VeryHigh |

|

Reason

Modest spread repricing with no clear reason.

|

||||

| Annington Funding Plc 2.308% Oct 2032 | GBP | -2.15% | 4.51% | VeryHigh |

|

Reason

Modest spread repricing with no clear reason.

|

||||

| Sysco 4.5% Apr 2046 | USD | -2.06% | 6.21% | Medium |

|

Reason

Leveraged $29bn Restaurant Depot acquisition led to downgrade risk.

|

||||

| Intl Paper 8.7% Jun 2038 | USD | -1.99% | 6.17% | Medium |

|

Reason

Weak performance and cautious analyst outlook.

|

||||

| CSX 7.45% Apr 2038 | USD | -1.87% | 5.40% | Low |

|

Reason

Modest spread repricing with no clear reason.

|

||||

| Puget Sound Engy 7% Mar 2029 | USD | -1.67% | 4.98% | Low |

|

Reason

New junior debt deal and refinancing activity slightly pressured existing secured bonds.

|

||||

Primary market activity was relatively subdued due to the Easter holiday, with fewer deals but still several benchmark-sized transactions across both EUR and USD markets. Among the largest were Hyundai Capital America with around USD 2.0bn across 2–5 year maturities, and JBS with roughly USD 2.0bn in long-dated bonds out to 30 years. JBS is one of the world’s largest meat producers, with operations across beef, poultry, and pork markets in the Americas, Europe, and Australia.

Another notable transaction came from Sword Purchaser LLC, which raised around USD 2.4bn. This issuer is a special-purpose vehicle set up to finance Clayton, Dubilier & Rice’s leveraged buyout of Sealed Air. Sealed Air is a global packaging company focused on food protection and parcel-shipping solutions, best known for brands such as Bubble Wrap and Cryovac.

| Issuer | Size | Term | Yield | Risk Level |

| Abn Amro Bank | EUR 1,2bn |

4Y | 3,4% | Very Low |

|

ISIN (CUSIP)

XS3311914850

|

||||

| Alerion Clean Power Spa | EUR 0,30bn |

6Y | 4,6% | Very High |

|

ISIN (CUSIP)

XS3213330791

|

||||

| American Water Capital | USD 0,70bn |

10Y | 5,2% | Medium |

|

ISIN (CUSIP)

03040WBH7

|

||||

| Bank Mandiri (Persero) Tbk Pt | USD 0,75bn |

5Y | 5,4% | Medium |

|

ISIN (CUSIP)

XS3302293819

|

||||

| Bng Bank | EUR 1,2bn |

10Y | 3,3% | Very Low |

|

ISIN (CUSIP)

XS3336964369

|

||||

| Currenta Group Holdings Sarl | EUR 0,12bn |

PERP | FLOAT, +400bp | High |

|

ISIN (CUSIP)

XS3067389174

|

||||

| De Volksbank | EUR 0,50bn |

7Y | 3,3% | Very Low |

|

ISIN (CUSIP)

XS3335806678

|

||||

| Erste Group Bank | EUR 1,0bn |

5Y | 3,1% | Very Low |

|

ISIN (CUSIP)

AT0000A3TF46

|

||||

| General Motors Financial Company | USD 1,4bn |

3Y | 4,8% | Medium |

|

ISIN (CUSIP)

US37045XFQ43

|

||||

| Hessen, State Of | EUR 1,0bn |

4Y | 2,9% | Very High |

|

ISIN (CUSIP)

DE000A1RQFC1

|

||||

| Hyundai Capital America | USD 2,0bn |

2–5Y | 4,6–5,0% | Low |

|

ISIN (CUSIP)

US44891CEJ80…US44891CEL37

|

||||

| Ing Bank | EUR 1,5bn |

5Y | 3,2% | Very Low |

|

ISIN (CUSIP)

XS3332391757

|

||||

| Jbs | USD 2,0bn |

11–31Y | 5,6–6,5% | Medium |

|

ISIN (CUSIP)

USL56608AV11…USL56608AW93

|

||||

| Komercni Banka As | EUR 0,75bn |

6Y | 3,3% | Very Low |

|

ISIN (CUSIP)

XS3328489334

|

||||

| Korea Development Bank | EUR 1,0bn |

3Y | 3,1% | Very Low |

|

ISIN (CUSIP)

XS3323712235

|

||||

| Korea Mine Rehabilitation And Mineral Resources | USD 0,50bn |

5Y | 5,0% | Low |

|

ISIN (CUSIP)

XS3322576417

|

||||

| Liquid Telecommunications Financing | USD 0,30bn |

5Y | 10,8% | Very High |

|

ISIN (CUSIP)

XS3330165674

|

||||

| New Zealand Local Government Funding Agency | EUR 0,50bn |

6Y | 3,2% | Very Low |

|

ISIN (CUSIP)

XS3337424462

|

||||

| Nomura Holdings | EUR 0,60bn |

7Y | 4,2% | Medium |

|

ISIN (CUSIP)

XS3330368351

|

||||

| Realty Income | USD 0,80bn |

7Y | 5,0% | Low |

|

ISIN (CUSIP)

756109DB7

|

||||

| Sasol Financing International | USD 0,75bn |

7Y | 8,8% | High |

|

ISIN (CUSIP)

USU8035UAD47

|

||||

| Shinhan Bank | USD 0,60bn |

3–5Y | 4,4%; FLOAT, +58bp | Low |

|

ISIN (CUSIP)

USY7770HAE81

|

||||

| State Of Rhineland Palatinate | EUR 0,25bn |

PERP | 3,3% | Very Low |

|

ISIN (CUSIP)

DE000RLP1635

|

||||

| Sword Purchaser | USD 2,4bn |

7–8Y | 8,5–10,5% | Very High |

|

ISIN (CUSIP)

USU8681CAB55…USU8681CAA72

|

||||

| Talanx | EUR 0,50bn |

7Y | 3,8% | Very High |

|

ISIN (CUSIP)

XS3311087152

|

||||

| The Export-Import Bank Of Korea | USD 0,50bn |

5Y | 4,2% | Very Low |

|

ISIN (CUSIP)

USY2387CVK89

|

||||

| Veolia Environnement | EUR 1,0bn |

5–10Y | 3,7–4,1% | Medium |

|

ISIN (CUSIP)

FR0014017P12…FR0014017P04

|

||||

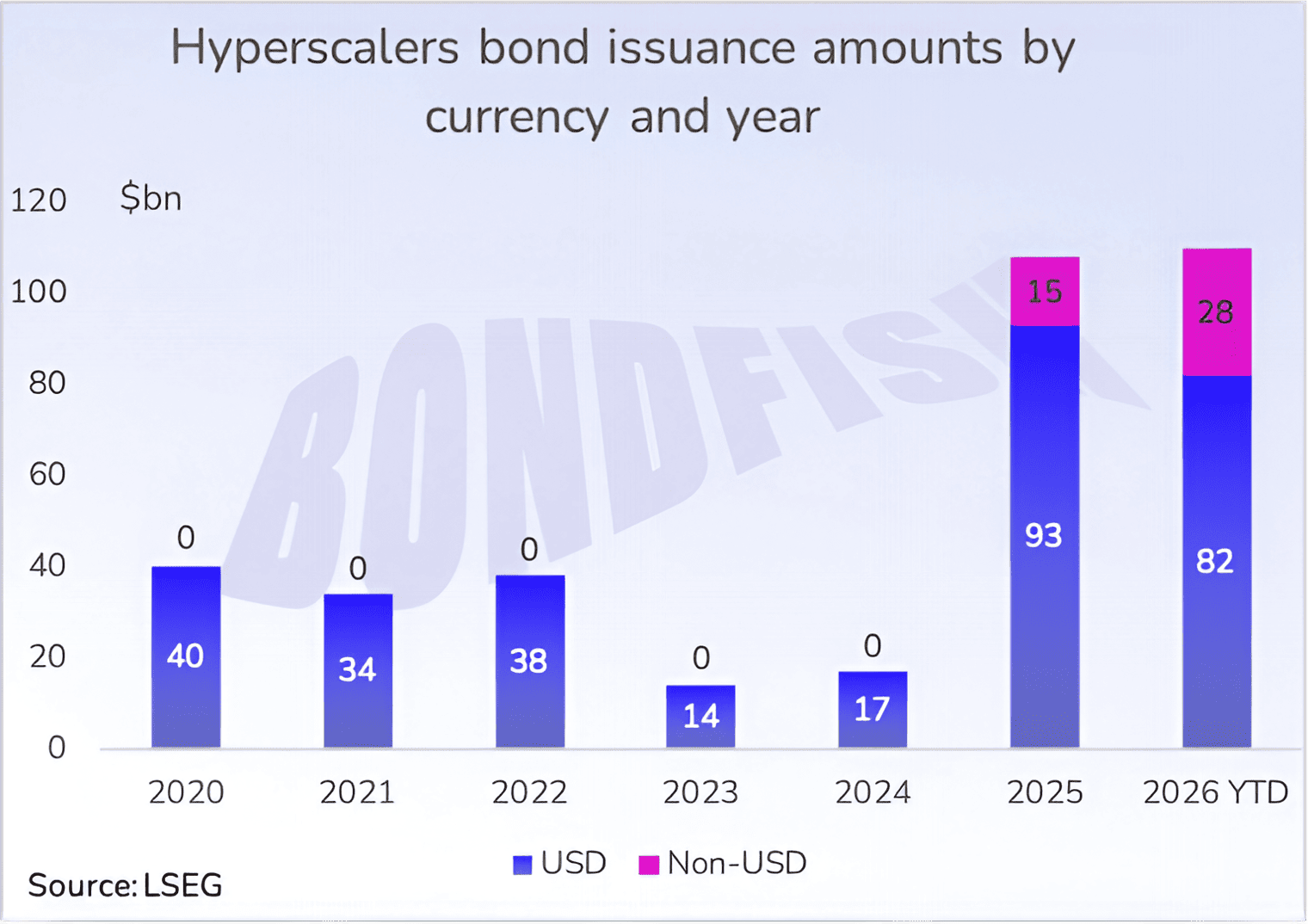

AI cycle is no longer just an equity story — it is becoming a major bond market theme.

Debt issuance from hyperscalers —Amazon, Microsoft, Google and peers — has accelerated sharply. Volumes jumped from $17bn in 2024 to more than $100bn in 2025, and have already exceeded $100bn year-to-date in 2026 (which is around 15–16% of total US IG supply this year).

They are also increasingly issuing in non-USD markets. Why? Because tech exposure is much lower in EUR, GBP and CHF credit markets than in USD, so hyperscalers can diversify funding and tap fresh demand without pushing too much supply into the USD market and risking wider spreads.