Building a balanced investment portfolio often means combining assets that generate income with those that provide stability. Among all fixed income instruments, corporate bonds remain one of the most effective ways to achieve both goals. They sit between government bonds and equities in terms of risk and return, offering regular cash flows through interest payments while typically experiencing less volatility than stocks.

This article explores how investment grade corporate bonds can help balance risk and reward, how corporate bond funds work, and which current issues may suit investors looking for stability with solid income potential.

When investors buy corporate bonds, they are effectively lending money to a company — the bond issuer — in exchange for interest payments (also known as periodic interest payments) and the return of face value when the bond matures. A corporate bond is a debt obligation of the issuing company, representing its commitment to repay borrowed money with interest. Each bond has a coupon rate, which determines the amount of income received over its life, and a bond's maturity, which marks the repayment of the par value.

Unlike savings bonds or treasury bonds, which are backed by governments and considered to have lower risk, corporate bonds carry credit risk — the possibility that the issuer might default on its debt obligations. To compensate investors for this greater risk, corporate bonds usually offer higher yields.

Corporate bonds are categorized by their credit ratings, which reflect the issuer’s ability to meet its obligations. The issuer's ability to make timely payments is a key factor in determining credit risk and bond pricing, as it indicates the financial health and credibility of the issuer.

For long-term investors seeking predictable income and capital preservation, investment grade bonds are generally more appropriate. These investment grade bonds issued by financially solid companies are considered low risk due to the financial strength of the issuers, and often offer a balance between safety and attractive yields, especially during periods when interest rates rise or interest rates fall.

Corporate bonds work as a key component of the fixed income portion of a diversified portfolio. They provide regular interest payments, which can help offset declines in equity markets. When interest rates move, bond prices adjust inversely: if interest rates rise, existing bonds with lower coupons may trade at a discount on the secondary market; if interest rates decline, their prices typically increase. Corporate bonds carry credit risk; in fact, corporate bonds generally have more credit risk than government or agency bonds, which is reflected in their higher yields.

Because of this relationship, understanding interest rate risk is crucial. Investors with a shorter time horizon or lower risk tolerance may prefer bonds with moderate maturities, which balance yield and price stability. Medium term bonds, typically with maturities of four to ten years, can offer a balance between yield and price stability for these investors.

In a world where interest rates remain uncertain and inflation continues to influence returns, investment grade corporate bonds offer a compelling balance. These instruments combine:

Predictable income through coupon payments

Transparency in issuer fundamentals

Liquidity through trading on the secondary market

Diversification benefits versus equities or municipal bonds

They are often used by conservative investors or retirees who seek fixed rate returns without exposure to speculative investments.

Additionally, investment grade corporate bonds are less affected by the federal alternative minimum tax, making them suitable for a wide range of portfolios. When compared to non investment grade bonds, they tend to demonstrate lower default risk and less price volatility.

For investors who prefer not to select individual bonds, corporate bond funds and exchange traded funds (ETFs) provide diversified exposure to corporate debt across sectors and maturities. Many corporate bond ETFs track a corporate index, which serves as a benchmark for the fund's composition and performance. Some funds, such as those focused on US investment grade bonds, may track a US corporate index to provide exposure to intermediate-term US corporate bonds. These bond funds pool investor capital to purchase dozens or even hundreds of bonds issued by different corporations. By investing in these funds, investors participate alongside other investors, which increases market liquidity and enables easier trading of bonds.

The main advantage of corporate bond funds lies in diversification and liquidity. However, their current market value fluctuates with interest rates, and investors do not control the exact maturity date or coupon rate of each bond.

An investor seeking stable income over an extended period may consider combining corporate bond funds with carefully selected individual bonds to balance flexibility and predictability.

Even investment grade issuers can face downgrades or operational stress. Monitoring the issuer’s credit risk and financial health remains crucial. Investors should review the company’s cash flow, leverage, and liquidity position rather than relying only on external credit ratings.

When interest rates rise, the prices of fixed rate bonds generally fall. Conversely, when interest rates decline, bond prices increase. Managing interest rate risk means balancing bonds with different maturities to maintain stable overall income.

Additionally, floating rate bonds, which have variable interest rates that adjust with market benchmarks, can help reduce interest rate risk in a bond portfolio.

Higher inflation erodes the purchasing power of fixed income streams. This is particularly relevant for zero coupon bonds, which do not make periodic interest payments and rely entirely on capital appreciation at maturity.

Even highly rated corporate bonds may experience temporary price fluctuations in volatile markets. Maintaining a diversified bond portfolio across industries and maturities helps reduce these effects.

When investing in corporate bonds, two fundamental concepts to understand are face value and interest payments. The face value, also known as par value, is the principal amount that the bond issuer promises to repay the bondholder at the bond’s maturity date. This is the amount you, as an investor, will receive back when the bond matures, provided the issuer does not default.

Interest payments are the periodic payments made by the bond issuer to compensate investors for lending money. These payments are typically made semi-annually or annually and are calculated based on the bond’s coupon rate—a fixed percentage of the face value. For example, if you buy corporate bonds with a face value of €1,000 and a coupon rate of 5%, you will receive €50 in interest payments each year until the maturity date.

Investors can buy corporate bonds directly from the issuer during the initial offering or purchase existing bonds on the secondary market through brokers. Whether you hold the bond to maturity and collect all scheduled interest payments, or sell it before maturity at a potentially higher price, understanding the relationship between face value, coupon rate, and interest payments is key to maximizing returns from your corporate bond investments.

Yield to maturity (YTM) is a vital metric for anyone considering corporate bonds. YTM represents the total annualized return an investor can expect if the bond is held until its maturity date, taking into account the bond’s current market price, face value, coupon rate, and the time remaining until maturity. This calculation provides a comprehensive measure of a bond’s potential return, making it easier to compare different investment grade bonds and high yield bonds on an equal footing.

For example, if a corporate bond is trading below its face value, the YTM will be higher than the coupon rate, reflecting the additional gain from buying the bond at a discount. Conversely, if the bond is trading above face value, the YTM will be lower. Corporate bond funds and other bond funds also report their average YTM, allowing investors to assess the expected return of a diversified portfolio of corporate bonds, whether they are investment grade or high yield.

By focusing on yield to maturity, investors can make more informed decisions about which corporate bonds or corporate bond funds best align with their income goals and risk tolerance, ensuring their fixed income allocation remains both competitive and resilient.

Choosing between short-term and long-term corporate bonds is a key decision that shapes your portfolio’s risk and return profile. Short-term bonds, which typically mature in less than five years, offer lower yields but are less sensitive to interest rate risk. This makes them an attractive option for investors who prioritize capital preservation and may need access to their funds in the near future.

Long-term bonds, on the other hand, have maturities extending beyond ten years and generally provide higher yields to compensate for the increased risks. These bonds are more exposed to interest rate risk—meaning their prices can fluctuate significantly if interest rates change. They are also more vulnerable to inflation risk, as rising prices can erode the real value of future interest payments.

For example, an investor approaching retirement might favor short-term bonds to reduce exposure to market volatility, while a younger investor with a longer time horizon might choose long-term bonds to benefit from higher yields. Regardless of your choice, it’s important to consider the credit risk associated with each corporate bond, as well as how interest rate and inflation risk could impact your returns over time.

Evaluating corporate bonds requires a careful assessment of several key factors to ensure your investments align with your financial goals and risk tolerance. The first consideration is credit risk—the likelihood that the bond issuer will fail to make interest payments or repay the principal at maturity. Credit ratings, assigned by agencies like Moody’s or Standard & Poor’s, provide a quick reference for a bond’s credit quality. Investment grade bonds, which carry higher credit ratings, are generally considered safer but offer lower yields compared to non investment grade bonds, which are riskier but may provide higher returns.

Interest rate risk is another important factor. When interest rates rise, the value of existing bonds with lower coupon rates typically falls, as new bonds are issued with more attractive yields. Conversely, when interest rates decline, bond prices tend to rise. This dynamic affects both long term bonds and short term bonds, though long-term bonds are usually more sensitive to interest rate changes.

To make informed decisions, investors should also consider a bond’s yield to maturity, which reflects the total expected return if the bond is held until maturity. Diversifying across different types of bonds—including government bonds, municipal bonds, and a mix of maturities—can help manage risk and enhance returns. By thoroughly evaluating credit risk, interest rate risk, and yield to maturity, investors can build a robust portfolio of corporate bonds tailored to their unique investment objectives.

In a diversified portfolio, corporate bonds often act as a stabilizer. They may underperform equities during strong bull markets but tend to hold their value better during downturns. The steady income from coupon payments can smooth portfolio returns, especially when other investments like stocks or real estate experience volatility.

Investors with a moderate risk tolerance can combine investment grade bonds with government bonds or agency backed bonds to further reduce risk exposure. Those seeking higher income might add a smaller allocation to below investment grade debt, carefully balancing potential return with greater risk.

As of late 2025, the European bond market is stabilizing after several years of rate volatility. Inflation is gradually moderating, and interest rates appear near their cyclical peak. For long-term investors, this environment opens opportunities to lock in attractive coupon rates on quality issuers.

Yields on investment grade corporate bonds in euros remain well above pre-pandemic levels, offering meaningful income even after adjusting for inflation. Bond prices have largely adjusted to higher rates, providing a potentially favourable entry point.

Investors should also consider the impact of local taxes on bond income, as tax treatment can affect the net yield received from corporate bonds.

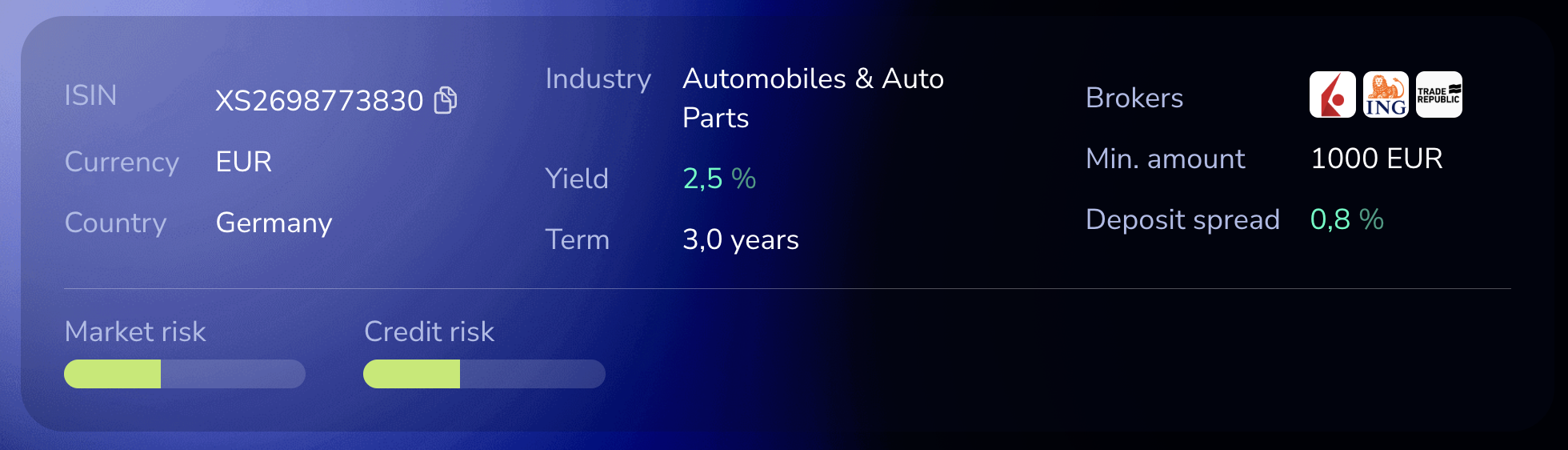

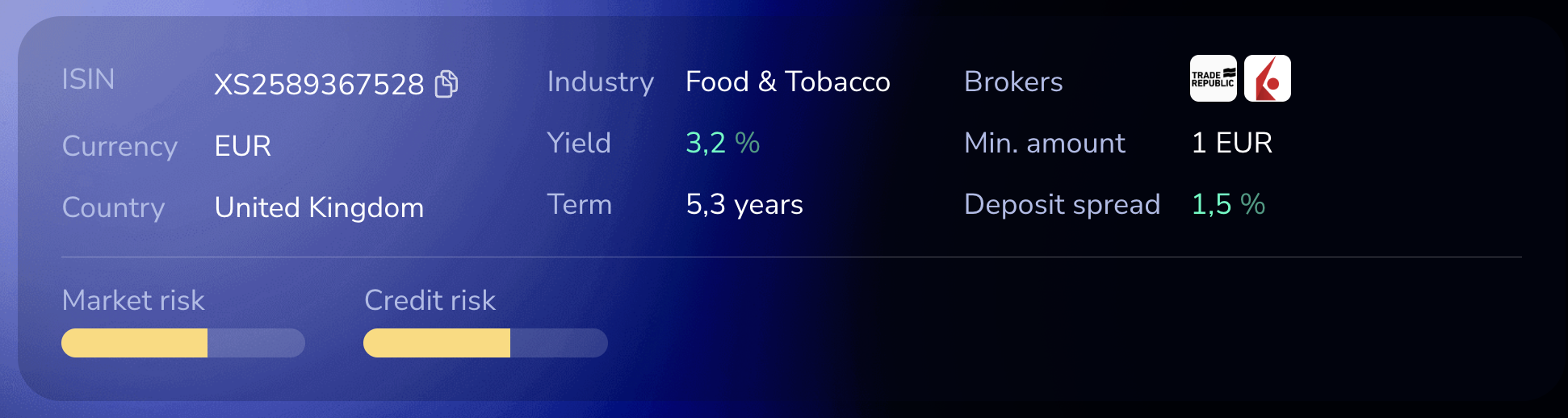

Below are three examples of investment grade corporate bonds currently available to European investors through common brokers such as Interactive Brokers or Trade Republic. Each combines strong financial foundations with attractive yield characteristics suitable for a diversified portfolio.

BMW is one of the world’s most respected automotive groups, with a robust balance sheet and significant cash reserves exceeding €17 billion. The company’s strong profitability, low leverage, and disciplined approach to capital allocation translate into relatively low credit risk for bondholders.

For investors seeking lower risk exposure in the corporate sector, BMW’s 2028 bond offers regular interest payments and a predictable maturity date. Its moderate term limits interest rate risk, making it a stable component within a balanced fixed income allocation.

Crédit Agricole is France’s largest retail-focused banking group, operating under a cooperative structure that reinforces capital stability. The bank’s balance sheet strength and large buffer of subordinated debt provide strong protection to senior bondholders and reduce default risk.

The bond offers both solid income and potential for capital appreciation if interest rates decline. It fits well within a diversified bond portfolio focused on reliable issuers from the European financial sector.

British American Tobacco (BAT) is one of the world’s largest consumer goods companies, generating steady free cash flow across 150 markets. Despite exposure to regulatory pressure and shifting consumer preferences, BAT’s high operating margins and stable cash generation help contain credit risk.

With a coupon rate of 5.375 %, this bond delivers a competitive yield compared to many other EUR-denominated corporate bonds. Its structure ensures regular interest payments for most of its life, providing a reliable income stream within a fixed rate allocation.

Selecting the best corporate bonds can be challenging, especially when comparing yields, maturities, and credit risk across dozens of issuers. That’s where Bondfish comes in.

Bondfish is a digital platform that simplifies access to investment grade corporate bonds and provides detailed analytics on yield, credit risk, and market availability. Investors can explore thousands of individual bonds and filter by term, currency, or sector to create their own diversified portfolio. Investors may also compare these options to other fixed income securities such as treasury notes, depending on their risk and return preferences.

The platform regularly highlights strong issuers like BMW Finance, Crédit Agricole, and B.A.T. Netherlands Finance, all of which offer compelling combinations of safety, yield, and liquidity. Whether you’re seeking stable income, planning for the long term, or simply want to understand how corporate bonds fit into your overall strategy, Bondfish can guide you through every step — from research to portfolio construction.

By helping investors evaluate fixed income opportunities transparently, Bondfish makes it easier to find the right balance between lower risk and meaningful returns in today’s dynamic bond market.