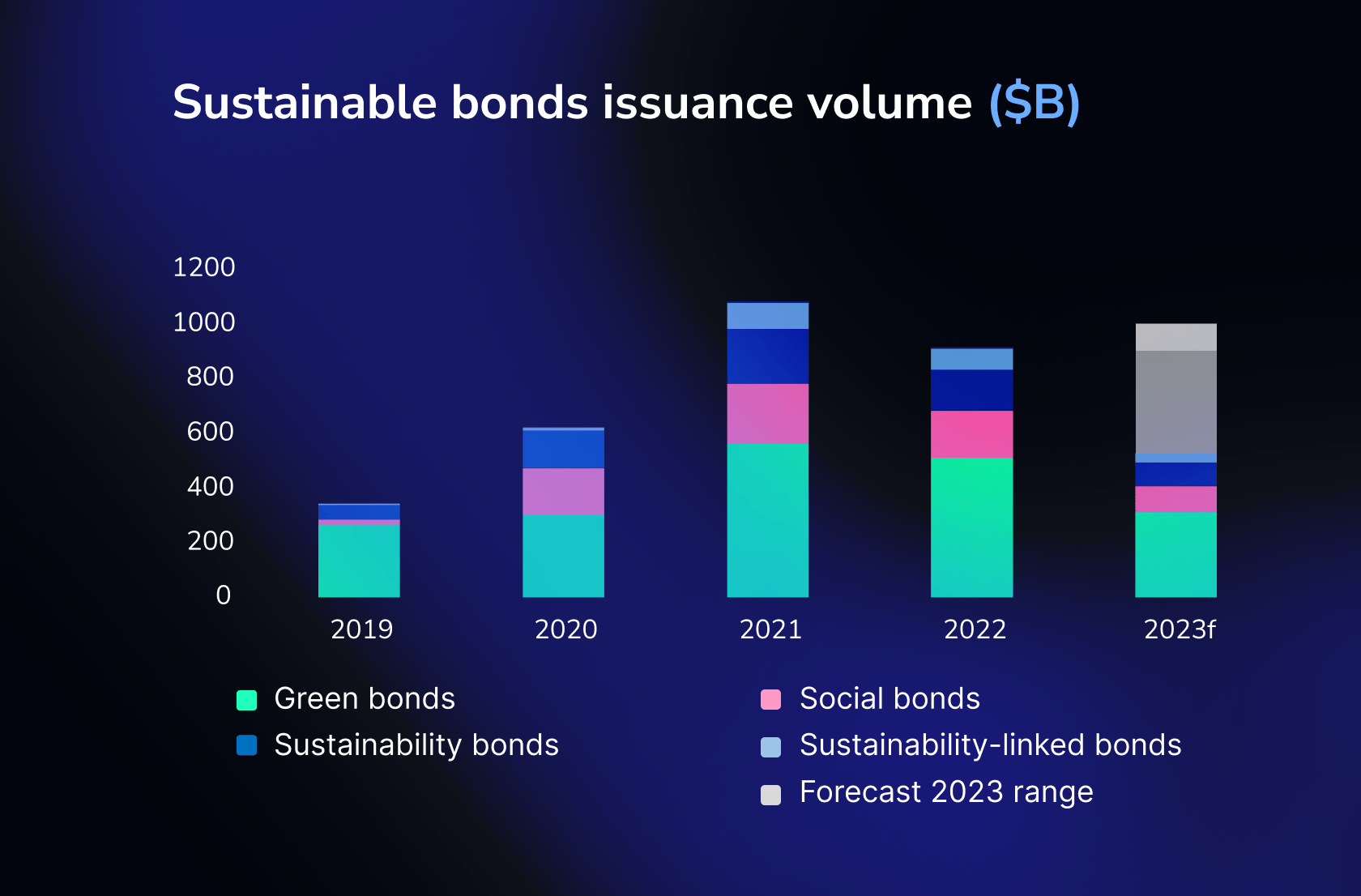

Sustainability bonds include Green, Social, Sustainability, and Sustainability-linked bonds.

The ESG bond market has steadily grown, surpassing $4 trillion by June 2023.

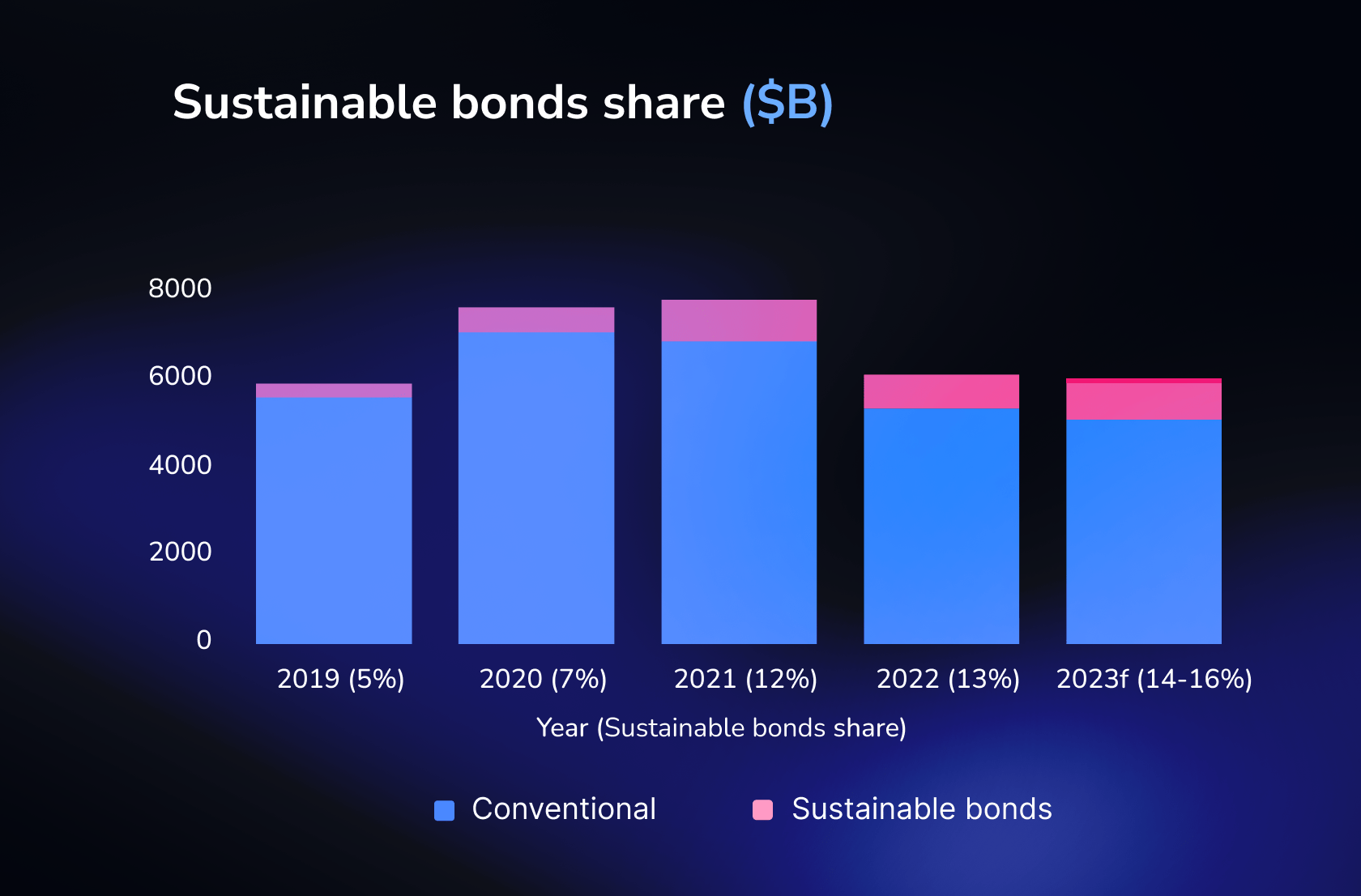

Sustainability bonds share is anticipated to exceed 14% of total global bond issuance this year.

Challenges in the sustainable bond market include "greenwashing," early development phase risks, and inherent credit risks.

Green, social along with other debt instruments focusing on sustainability, are gaining in significance in global fixed income markets. It becomes common trend to get investment strategies more and more aligned with internationally recognized sustainability goals such as The Paris Agreement or UN Sustainable Development Goals (SDG).

Sustainability term is closely aligned with ESG acronym. So firstly let’s get more background on this topic. Sustainable finance involves integrating environmental, social, and governance (ESG) factors into financial decision-making, promoting long-term investments in sustainable projects. This approach considers climate change, biodiversity preservation, pollution prevention, and social aspects like inclusiveness, labor relations, and human rights. In the EU, sustainable finance aligns with the European Green Deal's goals, aiming for economic growth while addressing environmental challenges and emphasizing transparency in managing ESG risks for a resilient financial system.

In recent years, the significance of ESG initiatives has risen with increasing awareness. Businesses that effectively embrace ESG principles can enjoy various advantages, such as gaining a competitive edge, attracting investors, enhancing financial performance, fostering customer loyalty, and establishing sustainable operations. An ESG score, alternatively termed an ESG rating, serves as a metric to assess how well organizations are implementing their ESG objectives, acknowledging the potential benefits it brings.

There are four types of bonds that are related to sustainability finance: Green bonds, Social bonds, Sustainability bonds, and Sustainability-linked bonds (or ESG bonds).

Green bonds are tailored to finance projects with positive environmental impacts. In this case proceeds are reserved to be exclusively used to finance specific new or existing green projects, such as renewable energy, energy efficiency, clean transportation, green buildings, wastewater management, and climate change adaptation. Green bonds are backed by the issuer’s entire balance sheet and usually abide to the Green Bond Principles (GBP) from the International Capital Market Association (ICMA). The GBP provides essential guidelines for transparent reporting on bonds' environmental objectives.

Proceeds from Social Bonds are reserved as well to be exclusively used to finance or refinance projects addressing social issues. Usually those are targeted to help specific social groups like those living below the poverty line, marginalized communities, migrants, unemployed individuals, women, sexual and gender minorities, people with disabilities, and displaced persons. Eligible project categories include, but are not limited to, initiatives related to food security and sustainable food systems, socioeconomic advancement, affordable housing, access to essential services, and affordable basic infrastructure. Additionally, they may involve affordable basic infrastructure projects. With the emergence of COVID-related bonds, funds have been made available for the mitigation of social problems associated with the pandemic.

Just like green bonds, the issuance of social bonds usually follows a set of voluntary guidelines known as the Social Bond Principles (SBP) from ICMA.

Sustainability bonds combine financing for both green and social projects. They can be unsecured or secured with collateral on a specific asset, issued by various entities, including companies, governments, and municipalities. Such bonds should adhere to Sustainability Bond Guidelines from ICMA, aligning with both GBP and SBP.

In general, 3 sets of above mentioned principles (GBP, SBP, SBG) developed by ICMA in 2014 are based on the same four core components:

Use of Proceeds: funds should be exclusively allocated to eligible green and social projects.

Process for Project Evaluation and Selection: issuer should communicate project objectives and eligibility.

Management of Proceeds: proceeds of the issuance must be carefully tracked.

Reporting: use of proceeds must be reported to investors periodically.

Sustainability-Linked Bonds’ proceeds are not specifically allocated for specific project financing but should be used for corporate purposes aligned with ESG activities. These bonds should be connected to relevant, measurable, and verifiable KPIs. Progress towards these KPIs influences the bond's coupon. These bonds incentivize companies to commit to sustainability, particularly aligning with UN SDGs or the Paris Agreement.

For this bond category ICMA have recently issued separate set of guidelines: Sustainability-Linked Principles (SLBP), that have been in implemented 2020 and are comprised from 5 main components:

Selection of Key Performance Indicators (KPIs).

Calibration of Sustainability Performance Targets (SPTs).

Bond characteristics.

Reporting.

Verification.

Sources: Environmental Finance Bond Database; S&P Global Ratings.

Volume of ESG bond issuance has been growing steadily over the years in line with the overall debt market. Total cumulative issuance volume has passed the $3 trillion-mark in September 2022. In less than one year in June 2023 it reached already $4 trillion, which is a sign of persistent growing popularity of these investment instruments among global investors. The share of sustainability bonds is also rising steadily, forecasted to surpass 14% of total global bond issuance this year.

Sources: Environmental Finance Bond Database; S&P Global Ratings.

So what exactly drives investors’ interest towards this debt market segment? Experts mostly are highlighting following factors:

Riding the ESG trend: The rise of sustainable bond issuance, driven by global standards and growing client interest in ESG practices, is further accelerated by the COVID-19 crisis. This includes increased issuance in social, SDG, and pandemic-related bonds, alongside the expanding green bond market.

Sustainability goals alignment: Sustainable bonds allow investors to align their portfolios with meaningful sustainability objectives, leveraging the mature and sizable global bond market to encourage companies to commit to sustainability during fundraising, fostering positive social and environmental impact.

Seizing opportunities while managing sustainability risks: Investors recognize the significance of ESG factors in evaluating global economies and markets, driving long-term opportunities and risks across asset classes during the decarbonisation of the economy.

In essence, we can view the development story of sustainability investments as a self-fulfilling prophecy: as the green agenda becomes more widespread among the general public, individual investors increasingly seek opportunities in ESG-compliant companies and projects. Consequently, more sustainability-linked instruments are issued annually to meet this growing demand. When the supply lags behind, such instruments exhibit better performance compared to the conventional segment. This, in turn, piques the interest of portfolio managers, prompting them to overweight green bonds in their portfolios, creating a reinforcing cycle.

Eventually, we believe, the sustainability agenda will either become widely accepted across a broad range of companies, or it may lose its significance due to a concept degradation, akin to what occurred with eco products, where customers are no longer motivated to overpay for the mythical label on food product packaging. The performance will show no discrepancies across the market. But in current development stage we expect accelerating growth in this segment to continue.

Despite emergence of guiding principles that reinforced the structure and integrity of sustainable bond market, the persistent challenge of bad practices among issuers remains quite pronounced. Main case of such bad practices is called “greenwashing” and involves issuers misrepresenting the positive environmental impact of bond proceeds. It is fuelled mainly by the broad criteria for defining a green bond, coupled with the absence of formal issuance guidelines in numerous emerging markets.

There are also factors that stem from the young development phase of sustainable bond market, which constitutes only a small portion of the larger fixed income market. Therefore, these investments may pose heightened liquidity and overconcentration risks for specific issuers, sectors, or regions.

Furthermore, akin to other fixed income instruments, sustainable bonds carry credit or default risk, signifying the potential for borrowers to fail in repaying the loan, leading to default. The extent of default risk hinges on the underlying credit quality of the issuer.

These challenges underscore the critical role of investment managers in thoroughly assessing security documentation to ascertain the true use of proceeds and the anticipated impact. Experienced investment advisers possess the expertise to adeptly navigate and mitigate these risks, aiming for appealing risk-adjusted returns.

To learn more about the European sustainable bonds and explore concrete issues in the lucrative segment you can use Bondfish bond screener, which also enables registered users to filter out green bonds.