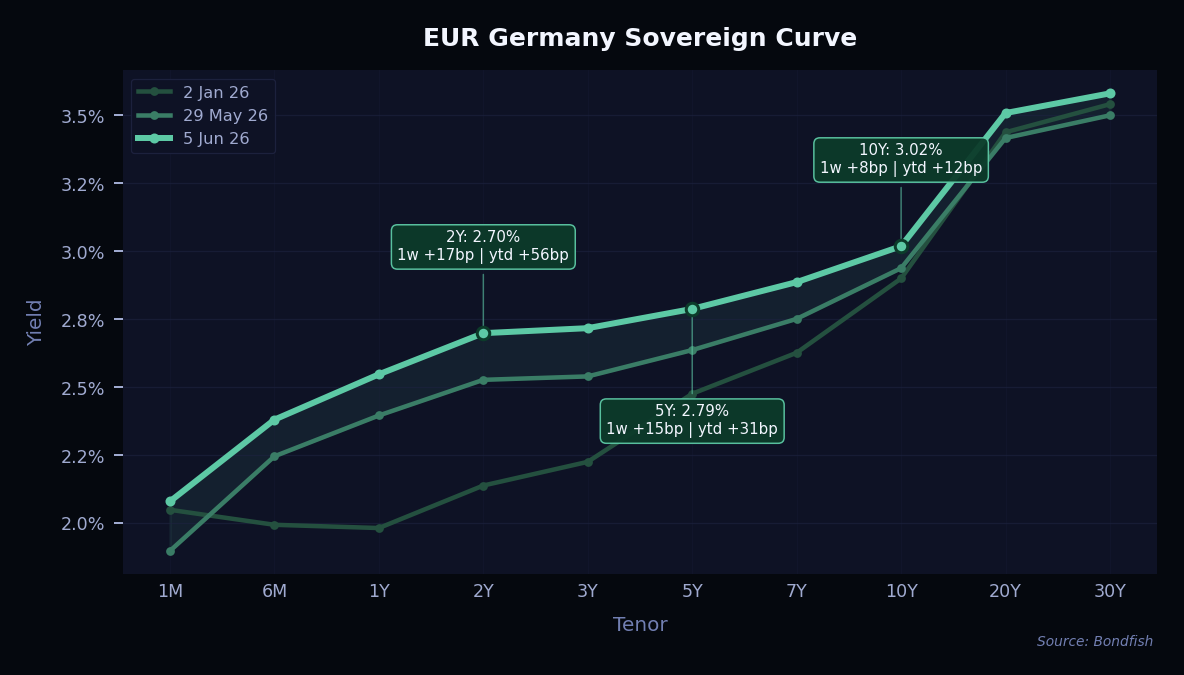

EUR — German Bund yields sold off sharply, with 2-year yields up around 16bp and the 10-year rising roughly 10bp. The front end bore the brunt as markets priced in a near-certain 25bp ECB rate hike at next week's meeting, which would bring the deposit rate to 2.25%. Stronger-than-expected core inflation across the eurozone added fuel to the move.

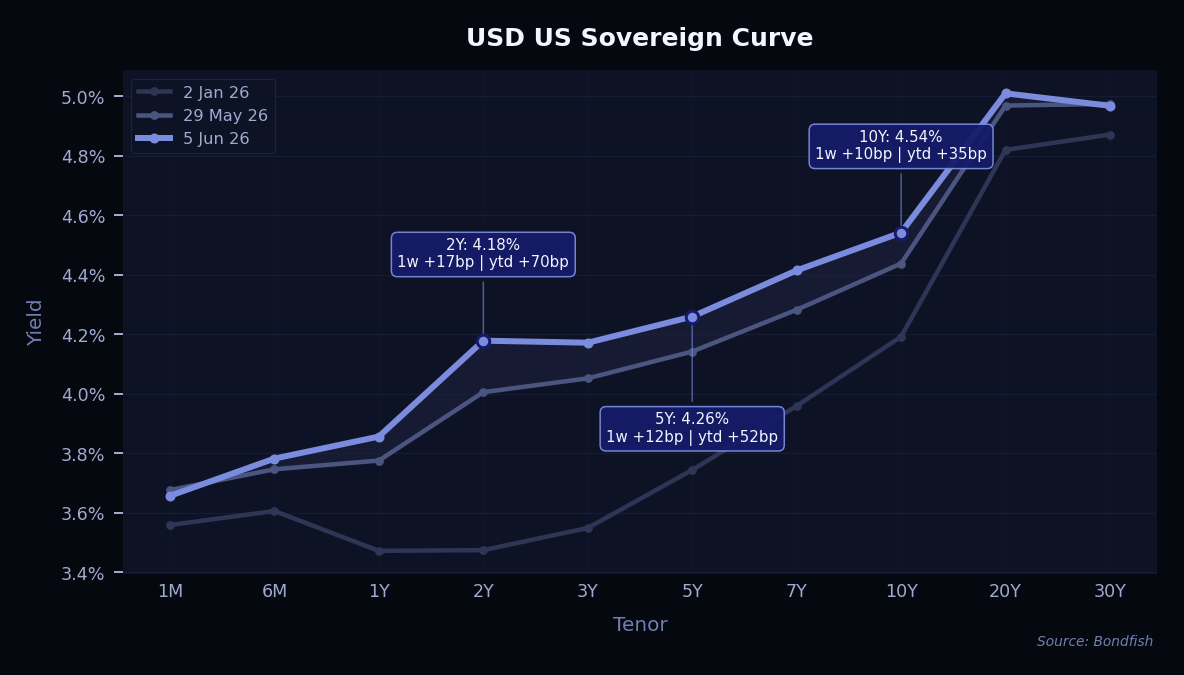

USD — US Treasury yields rose across the board, with shorter maturities hit hardest. The 2-year yield jumped around 14bp while the 10-year climbed roughly 9bp. The main trigger was Friday's jobs report — 172,000 new jobs were added in May, nearly double the 88,000 forecast — pushing markets to price at least one Fed rate hike by year-end. Stalled US-Iran ceasefire talks kept oil prices elevated, adding to the inflation-driven pressure on rates.

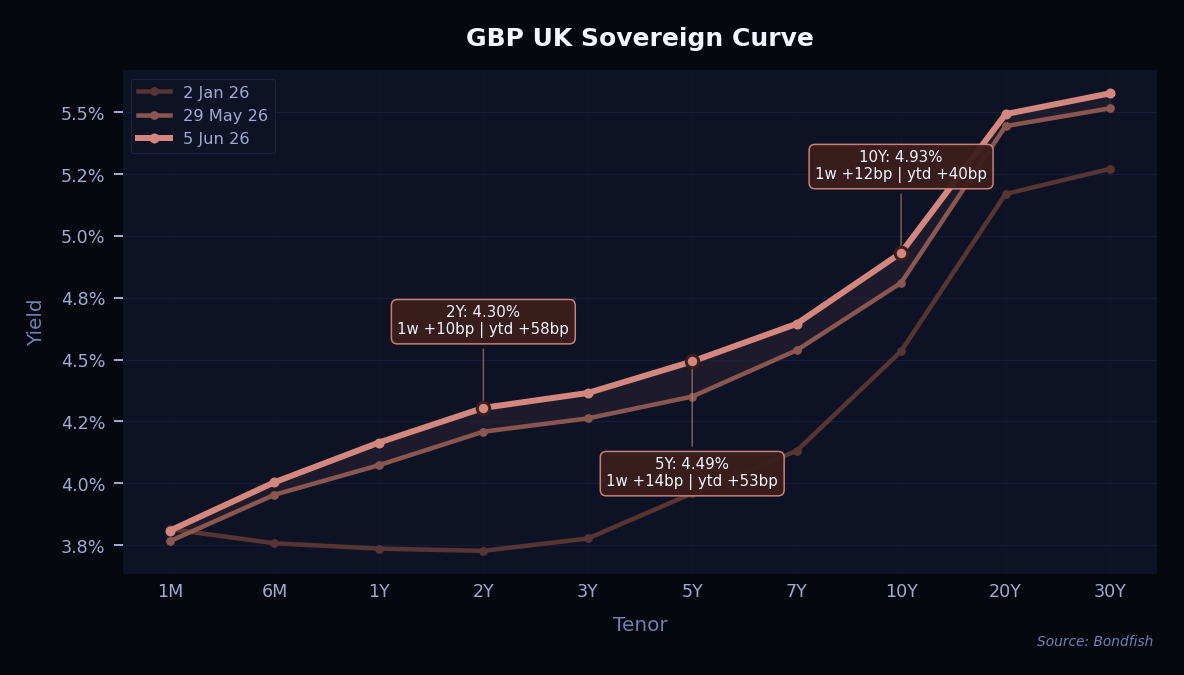

GBP — UK gilt yields followed the global trend, with 2-year yields up around 13bp and the 10-year rising about 9bp. Mixed signals from Bank of England officials added to the uncertainty — the Governor played down the need for hikes while a more hawkish colleague suggested tightening could come within weeks. With the Strait of Hormuz still effectively closed and energy prices staying high, markets now price nearly 50bp of BoE hikes by December.

Flowers Foods bonds led this week's gainers, up 5.47%, after S&P affirmed their BBB- investment-grade rating — though with the outlook revised to negative. Zambia's 2053 bond gained nearly 4% after a holdout creditor group holding more than 25% of the bonds agreed to join the revised tender offer at a higher price. B&M European Value Retail bonds gained around 1% in sterling after the company beat full-year earnings estimates on both revenue and EBITDA, sending its equity sharply higher on the day.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| Flowers Foods 6.2% Mar 2055 | USD | 5,47% | 7,38% | Medium |

|

Reason

S&P affirmed investment-grade rating, avoiding a downgrade; bond trading volume spiked sharply.

|

||||

| Zambia 0.5% Dec 2053 | USD | 3,72% | 0,69% | Very High |

|

Reason

Holdout creditor group owning 25%+ of bonds agreed to join revised tender offer at higher price.

|

||||

| Kronos Intnl 9.5% Mar 2029 | EUR | 1,74% | 11,15% | Very High |

|

Reason

No clear positive issuer catalyst.

|

||||

| Summer BC Holdco 5.875% Feb 2030 | EUR | 1,72% | 9,14% | Very High |

|

Reason

No clear positive issuer catalyst.

|

||||

| B&M European 6.5% Nov 2031 | GBP | 1,21% | 7,20% | High |

|

Reason

Full-year earnings beat expectations on revenue and EBITDA, sending equity sharply higher.

|

||||

| B&M European 8.125% Nov 2030 | GBP | 0,86% | 6,21% | High |

|

Reason

Full-year earnings beat expectations on revenue and EBITDA, sending equity sharply higher.

|

||||

| SKF 0.875% Nov 2029 | EUR | 0,83% | 2,53% | Medium |

|

Reason

No clear positive issuer catalyst.

|

||||

| Vesteda Finance 0.75% Oct 2031 | EUR | 0,81% | 2,55% | Low |

|

Reason

No clear positive issuer catalyst.

|

||||

| Iceland Bondco 4.375% May 2028 | GBP | 0,63% | 4,88% | Very High |

|

Reason

No clear positive issuer catalyst.

|

||||

Cable One was the week's worst performer, down 5.75%, as persistent subscriber losses and declining sales reinforced growing concerns about the cable sector's business model. Goodyear dropped nearly 4% after issuing new senior notes to refinance existing debt, adding pressure on outstanding bonds. Virgin Media Finance fell 3.19% after Fitch downgraded the company to B+, citing leverage above 6x and heavy ongoing network investment expected to continue through 2029.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| Cable One 4% Nov 2030 | USD | -5,75% | 16,79% | Very High |

|

Reason

Persistent subscriber losses and declining sales reflect a deteriorating cable business model.

|

||||

| Goodyear 5.625% Apr 2033 | USD | -3,85% | 8,68% | Very High |

|

Reason

Company issued new senior notes to refinance existing debt, adding pressure on outstanding bonds.

|

||||

| Virgin Media Fin 3.75% Jul 2030 | EUR | -3,19% | 8,01% | Very High |

|

Reason

Fitch downgraded the company to B+ citing leverage above 6x and heavy ongoing network investment.

|

||||

| Slovakia 2% Oct 2047 | EUR | -2,54% | 4,30% | Low |

|

Reason

High duration and modest spread repricing.

|

||||

| Republic of France 0.1% Jul 2047 | EUR | -1,95% | 2,04% | Very Low |

|

Reason

High duration and modest spread repricing.

|

||||

| Greece 1.875% Jan 2052 | EUR | -1,91% | 4,37% | Medium |

|

Reason

High duration and modest spread repricing.

|

||||

| United Kingdom 3.5% Jul 2068 | GBP | -1,34% | 5,48% | Very Low |

|

Reason

High duration and modest spread repricing.

|

||||

| SW Finance 4.5% Mar 2052 | GBP | -1,15% | 6,80% | Medium |

|

Reason

High duration and modest spread repricing.

|

||||

| UPS 5.125% Feb 2050 | GBP | -1,13% | 6,12% | Low |

|

Reason

High duration and modest spread repricing.

|

||||

Note: only long-term senior unsecured ratings were taken into account.

| Issuer | Agency | Change |

| ACI Rover Parent | S&P | B+ → BB- |

| American Trailer World | S&P | B- → CCC+ |

| Authentic Brands | S&P | B+ → BB- |

| Aveanna Healthcare | S&P | B- → B |

| Banco Cooperativo Espanol | Fitch | BBB → BBB+ |

| Beazer Homes USA | S&P | B → B- |

| Caja Rural de Granada S Coop de Credito | Fitch | BBB → BBB+ |

| California Resources | Fitch | B+ → BB- |

| CD&R Smokey Buyer | S&P | B- → CCC+ |

| China Hongqiao | S&P | BB → BB+ |

| China Huadian | Fitch | A- → A |

| China Huaneng | Fitch | A- → A |

| Conair | S&P | SD → CCC+ |

| Dell Technologies | S&P | BBB → BBB+ |

| DXC Technology | Moody's | Baa2 → Baa3 |

| Elavon Financial Services DAC | Fitch | AA- → A+ |

| Emeria SASU | Fitch | B- → CCC+ |

| Golden Energy And Resources | Fitch | B+ → B |

| Hellenic Telecommunications Organization | S&P | BBB+ → A- |

| Huaneng Power International | Fitch | A- → A |

| Ingenovis Health | S&P | SD → CCC+ |

| International Flavors & Fragrances | S&P | BBB- → BBB |

| Ivanti Software | S&P | CCC+ → CCC |

| Kyndryl | Moody's | Baa2 → Baa3 |

| LABL | S&P | D → CCC+ |

| Legence | S&P | B+ → BB- |

| LG Electronics | S&P | BBB → BBB+ |

| National Grid | Fitch | BBB- → BBB |

| National Grid Electricity Transmission | Fitch | BBB+ → A- |

| Republic of Maldives | Fitch | CC → CCC- |

| Republic of South Africa | Fitch | BB- → BB |

| Sammaan Capital | S&P | B+ → BB- |

| Shanghai Electric Power | Fitch | BBB+ → A- |

| State Power Investment | Fitch | A- → A |

| System1 | S&P | CCC+ → CC |

| Sytral | S&P | A+ (new) |

| Telefonaktiebolaget LM Ericsson | Moody's | Baa3 (new) |

| Urban One | S&P | CCC+ → SD |

| US Bank Trust Co NA | Fitch | AA- → A+ |

| Vmed O2 UK | Fitch | BB- → B+ |

| Volcan Cia Minera SAA | Fitch | B → B+ |

| Wabash National | S&P | B → B- |

| Wema Bank | Fitch | B- → B |

| West Technology | S&P | SD → CCC- |

| Yangzhou Economic and Technological Development Zone Development | S&P | BB+ → BBB- |

It was a quiet week for European supply. Investment grade issuance came in at just €9bn — the weakest opening week of June since 2022. High yield was similarly subdued at €2.4bn. On the IG side, notable deals included SSE printing two hybrid bonds totalling €1.3bn, OMV issuing a €750m perpetual, and Covea bringing a €750m 30-year. In high yield, Dufry priced a €400m 7-year at 4.625%, Renault raised €750m at 4.125%, and IQVIA printed €950m at 4.625%. Despite the slow week, fund flows turned positive — euro IG saw €624m of inflows and high yield attracted €296m.

| Issuer | Size | Term | Yield | Risk Level |

| Abertis Infraestructuras | EUR 0,75bn |

6Y | 3,8% | Medium |

|

ISIN (CUSIP)

XS3399007288

|

||||

| African Development Bank | EUR 1,2bn |

7Y | 3,1% | Very Low |

|

ISIN (CUSIP)

XS3402832441

|

||||

| Akbank | USD 0,50bn |

10Y | 8,2% | Very High |

|

ISIN (CUSIP)

XS3394857984

|

||||

| Ameriprise Financial | USD 0,75bn |

PERP | 4,8–5,3% | Low |

|

ISIN (CUSIP)

US03076CAR79

|

||||

| Andalucia, Autonomous Community Of | EUR 0,50bn |

8Y | 3,4% | Low |

|

ISIN (CUSIP)

ES0000090987

|

||||

| Antares Holdings | USD 0,60bn |

5Y | 6,8% | Medium |

|

ISIN (CUSIP)

US03666HAJ05

|

||||

| Arch Capital Group | USD 2,0bn |

10–30Y | 5,3–6,0% | Low |

|

ISIN (CUSIP)

03939AAB3…03939AAC1

|

||||

| Ati | USD 0,45bn |

7Y | 5,9% | High |

|

ISIN (CUSIP)

US01741RAP73

|

||||

| B&G Foods | USD 0,47bn |

5Y | 11,6% | Very High |

|

ISIN (CUSIP)

USU07409AE25

|

||||

| Bahrain, Kingdom Of | USD 1,0bn |

10Y | 7,1% | Very High |

|

ISIN (CUSIP)

XS3381699902

|

||||

| Banca Monte Dei Paschi Di Siena Spa | EUR 0,50bn |

3Y | 3,3% | Medium |

|

ISIN (CUSIP)

IT0005713612

|

||||

| Bank Gospodarstwa Krajowego | EUR 2,0bn |

8–15Y | 3,8–4,6% | Low |

|

ISIN (CUSIP)

XS3304272217…XS3401963502

|

||||

| Bank Leumi Le-Israel B.M | USD 1,0bn |

10Y | 5,7% | Medium |

|

ISIN (CUSIP)

IL0012416785

|

||||

| Bank Of New Zealand | USD 1,0bn |

5Y | 4,8%; FLOAT | Low |

|

ISIN (CUSIP)

USQ1269WAC93

|

||||

| Blue Owl Technology Finance | USD 0,50bn |

3Y | 6,7% | Medium |

|

ISIN (CUSIP)

095924AD8

|

||||

| BNG Bank | EUR 1,2bn |

7Y | 3,1% | Very Low |

|

ISIN (CUSIP)

XS3395922506

|

||||

| BPCE | USD 0,60bn |

5Y | FLOAT, +100bp | Low |

|

ISIN (CUSIP)

FR00140176N2

|

||||

| BPCE | EUR 1,5bn |

6Y | 3,2% | Very Low |

|

ISIN (CUSIP)

FR0014018XB6

|

||||

| British Columbia, Province Of | GBP 1,0bn |

6Y | 4,7% | Very Low |

|

ISIN (CUSIP)

XS3402723400

|

||||

| Canadian Imperial Bank Of Commerce | EUR 1,2bn |

6Y | 3,2% | Very Low |

|

ISIN (CUSIP)

XS3401887057

|

||||

| Castilla Y Leon, Autonomous Community Of | EUR 0,50bn |

8Y | 3,4% | Low |

|

ISIN (CUSIP)

ES0001351628

|

||||

| Cemex | USD 1,5bn |

10Y | 5,8% | Medium |

|

ISIN (CUSIP)

US151290CD37

|

||||

| Clariant International Financial Services Luxembourg | EUR 0,50bn |

6Y | 4,3% | Very High |

|

ISIN (CUSIP)

XS3311989787

|

||||

| Close Brothers Finance | GBP 0,25bn |

5Y | 5,8% | Medium |

|

ISIN (CUSIP)

XS3401772747

|

||||

| Consolidated Edison | USD 1,3bn |

10–30Y | 5,2–5,9% | Low |

|

ISIN (CUSIP)

209111GQ0…209111GR8

|

||||

| Rabobank | GBP 0,60bn |

5Y | 5,1% | Low |

|

ISIN (CUSIP)

XS3404437991

|

||||

| Rabobank | USD 1,8bn |

2–10Y | 4,3–5,1%; FLOAT | Very Low |

|

ISIN (CUSIP)

US21688ABW18…US21688ABZ49

|

||||

| Covea Cooperations | EUR 0,75bn |

30Y | 4,6% | Low |

|

ISIN (CUSIP)

FR0014018VQ8

|

||||

| Credit Agricole | GBP 0,65bn |

8Y | 5,4% | Low |

|

ISIN (CUSIP)

FR0014018ZG0

|

||||

| Credit Agricole Public Sector | EUR 0,75bn |

10Y | 3,5% | Very Low |

|

ISIN (CUSIP)

FR0014019154

|

||||

| Credit Mutuel Arkea | EUR 0,50bn |

11Y | 4,3% | Medium |

|

ISIN (CUSIP)

FR0014018V39

|

||||

| Crelan Home Loan Scf | EUR 0,50bn |

8Y | 3,4% | Very Low |

|

ISIN (CUSIP)

FR0014019139

|

||||

| Deutsche Pfandbriefbank | EUR 0,50bn |

4Y | 3,1% | Very Low |

|

ISIN (CUSIP)

DE000A3827A0

|

||||

| Dominion Energy | USD 0,82bn |

10Y | 5,4% | Medium |

|

ISIN (CUSIP)

US25746UEB17

|

||||

| Dorman Products | USD 0,45bn |

8Y | 6,2% | High |

|

ISIN (CUSIP)

USU25788AA55

|

||||

| Dufry One | EUR 0,40bn |

7Y | 4,6% | High |

|

ISIN (CUSIP)

XS3401887487

|

||||

| Duke Energy Carolinas | USD 2,4bn |

5–30Y | 4,7–5,8% | Very Low |

|

ISIN (CUSIP)

US26442CBR43…US26442CBT09

|

||||

| DZ Hyp | EUR 1,0bn |

10Y | 3,3% | Very Low |

|

ISIN (CUSIP)

DE000A4DFKT2

|

||||

| Empresa Distribuidora De Electricidad De Mendoza | USD 0,30bn |

7Y | 10,8% | Very High |

|

ISIN (CUSIP)

USP37213AH17

|

||||

| Essential Properties | USD 0,40bn |

10Y | 5,6% | Medium |

|

ISIN (CUSIP)

25746UEB1

|

||||

| European Investment Bank | EUR 5,0bn |

10Y | 3,2% | Very Low |

|

ISIN (CUSIP)

EU000A4EV1G4

|

||||

| Export Finance Australia | USD 1,8bn |

5–10Y | 4,2–4,6% | Very Low |

|

ISIN (CUSIP)

XS3382707985…XS3400621085

|

||||

| Export-Import Bank Of Korea | GBP 0,50bn |

3Y | 4,5% | Very Low |

|

ISIN (CUSIP)

XS3389684773

|

||||

| Fairfax Financial Holdings | USD 0,75bn |

30Y | 6,2% | Medium |

|

ISIN (CUSIP)

USC33461AQ46

|

||||

| Goodyear Tire & Rubber | USD 1,0bn |

6Y | 8,9% | Very High |

|

ISIN (CUSIP)

US382550BT77

|

||||

| Green Palm Bidco Sarl | USD 1,5bn |

15–20Y | 6,0–6,5% | Very Low |

|

ISIN (CUSIP)

XS3394864170…XS3394864501

|

||||

| Hammerson | EUR 0,35bn |

5Y | 3,9% | Medium |

|

ISIN (CUSIP)

XS3392861913

|

||||

| Hessen, State Of | EUR 0,50bn |

7Y | FLOAT | Very High |

|

ISIN (CUSIP)

DE000A1RQFF4

|

||||

| Hkt Capital | USD 0,65bn |

10Y | 5,2% | Medium |

|

ISIN (CUSIP)

XS3397211908

|

||||

| Hubbell | USD 1,9bn |

5–10Y | 4,8–5,3% | Medium |

|

ISIN (CUSIP)

US443510AM41…US443510AP71

|

||||

| Iifl Finance | USD 0,50bn |

3Y | 7,6% | Very High |

|

ISIN (CUSIP)

USY3R78RMD40

|

||||

| ING Belgium | EUR 0,75bn |

5Y | 3,0% | Very Low |

|

ISIN (CUSIP)

BE0390354265

|

||||

| Inter-American Development Bank | USD 3,0bn |

5Y | 4,3% | Very Low |

|

ISIN (CUSIP)

US4581X0FA13

|

||||

| IQVIA | EUR 0,95bn |

7Y | 4,6% | High |

|

ISIN (CUSIP)

XS3315365398

|

||||

| KBC Verzekeringen | EUR 0,50bn |

10Y | 4,4% | Very High |

|

ISIN (CUSIP)

BE6374729836

|

||||

| KfW | GBP 0,60bn |

6Y | 4,5% | Very Low |

|

ISIN (CUSIP)

XS3403817003

|

||||

| Kutxabank | EUR 0,50bn |

6Y | 3,6% | Low |

|

ISIN (CUSIP)

ES0243307024

|

||||

| Kvika Banki Hf | EUR 0,15bn |

4Y | 4,5% | Medium |

|

ISIN (CUSIP)

XS3399022758

|

||||

| Latvia, Republic Of | EUR 1,0bn |

7Y | 3,5% | Low |

|

ISIN (CUSIP)

XS3395907705

|

||||

| Lloyds Banking Group | GBP 0,75bn |

7Y | 5,5% | Low |

|

ISIN (CUSIP)

XS3397151815

|

||||

| Macquarie Bank | USD 1,2bn |

11Y | 5,8% | Very Low |

|

ISIN (CUSIP)

55608RCD0

|

||||

| Mapfre | EUR 0,50bn |

11Y | 4,5% | Very High |

|

ISIN (CUSIP)

ES0224244139

|

||||

| Marex Group | USD 0,50bn |

PERP | 7,7% | High |

|

ISIN (CUSIP)

XS3388192935

|

||||

| Massachusetts Mutual Life Insurance | USD 1,0bn |

30Y | 6,0% | Low |

|

ISIN (CUSIP)

USU57576AQ07

|

||||

| Mastercard | USD 5,0bn |

2–10Y | 4,3–5,0%; FLOAT | Very Low |

|

ISIN (CUSIP)

US57636QBJ22…US57636QBM50

|

||||

| MTR | EUR 3,0bn |

8–20Y | 3,3–4,2% | Very Low |

|

ISIN (CUSIP)

HK0001306932…HK0001306957

|

||||

| National Grid | USD 0,75bn |

10Y | 5,4% | Medium |

|

ISIN (CUSIP)

636274AG7

|

||||

| National Securities Clearing | USD 1,8bn |

2–5Y | 4,4–4,7%; FLOAT | Very Low |

|

ISIN (CUSIP)

U7000RAP7…U7000RAR3

|

||||

|

ISIN (CUSIP)

XS3405659833

|

||||

| Nationwide Building Society | EUR 0,50bn |

11Y | 4,1% | Medium |

|

ISIN (CUSIP)

XS3393974228

|

||||

| Noble Finance Ii | USD 0,80bn |

8Y | 6,2% | Very High |

|

ISIN (CUSIP)

USU7359PAC78

|

||||

| Nordea Kiinnitysluottopankki Oyj | EUR 1,5bn |

4–10Y | 2,9–3,3% | Very Low |

|

ISIN (CUSIP)

XS3401022580…XS3401025765

|

||||

| North-Rhine Westphalia, State Of | USD 1,5bn |

5Y | 4,3% | Very Low |

|

ISIN (CUSIP)

XS3402929528

|

||||

| OMV | EUR 0,75bn |

PERP | 4,6% | Medium |

|

ISIN (CUSIP)

XS3401027118

|

||||

| Outfront Media Capital | USD 0,50bn |

8Y | 6,0% | Very High |

|

ISIN (CUSIP)

USU6833PAG64

|

||||

| Pacific Gas And Electric | USD 2,2bn |

5–30Y | 5,1–6,3% | Medium |

|

ISIN (CUSIP)

US694308LC93…US694308LE59

|

||||

| Pinnacle West Capital | USD 0,50bn |

3Y | 4,7% | Medium |

|

ISIN (CUSIP)

723484

|

||||

| Prudential Financial | USD 0,75bn |

30Y | 6,2% | Medium |

|

ISIN (CUSIP)

US744320BQ47

|

||||

| Public Service Enterprise Group | USD 0,50bn |

5Y | 4,8% | Medium |

|

ISIN (CUSIP)

US744573BC96

|

||||

| QXO | USD 3,0bn |

5–8Y | 6,5–6,9% | Very High |

|

ISIN (CUSIP)

USU7504AAA89…USU7504AAB62

|

||||

| Sammons Financial Group | USD 0,75bn |

10Y | 6,1% | Medium |

|

ISIN (CUSIP)

79588TAG5

|

||||

| Santander Holdings USA | USD 2,5bn |

4–11Y | 5,0–5,7% | Medium |

|

ISIN (CUSIP)

US80282KBS42…US80282KBU97

|

||||

| Southern Power | USD 0,60bn |

5Y | 4,8% | Medium |

|

ISIN (CUSIP)

843646AZ3

|

||||

| SSE | EUR 1,3bn |

PERP | 4,4–4,8% | Medium |

|

ISIN (CUSIP)

XS3310370799…XS3310370955

|

||||

| State Of Baden-Wuerttemberg | EUR 1,0bn |

15Y | 3,5% | Very Low |

|

ISIN (CUSIP)

DE000A3H26B2

|

||||

| Svenska Handelsbanken Ab | USD 1,8bn |

3–5Y | 4,5–4,7%; FLOAT | Very Low |

|

ISIN (CUSIP)

US86959NAW92…US86959NAY58

|

||||

| Synchrony Financial | USD 0,50bn |

PERP | 7,2% | High |

|

ISIN (CUSIP)

US87165BBA08

|

||||

| Technip Energies | EUR 0,50bn |

7Y | 4,0% | Very High |

|

ISIN (CUSIP)

XS3317598053

|

||||

| Teleflex | USD 0,50bn |

6Y | 5,9% | High |

|

ISIN (CUSIP)

USU87934AC64

|

||||

| TS Shipping Invest As | USD 0,10bn |

4Y | 7,5% | Very High |

|

ISIN (CUSIP)

NO0013673921

|

||||

| United Group | EUR 0,30bn |

7Y | FLOAT, +325bp | Very High |

|

ISIN (CUSIP)

XS327482793

|

||||

| Venture Global Lng | USD 2,2bn |

8–10Y | 6,4–6,6% | High |

|

ISIN (CUSIP)

92332YAG6…92332YAH4

|

||||

| Volkswagen Bank Gmbh | EUR 0,50bn |

2Y | FLOAT, +63bp | Low |

|

ISIN (CUSIP)

XS3402822210

|

||||

| Whirlpool | USD 2,0bn |

5–8Y | 7,5–7,9% | High |

|

ISIN (CUSIP)

USU9633LAA45…USU9633LAB28

|

||||

| Wisconsin Electric Power | USD 0,80bn |

5–10Y | 4,5–5,1% | Low |

|

ISIN (CUSIP)

US976656CX49…US976656CY22

|

||||

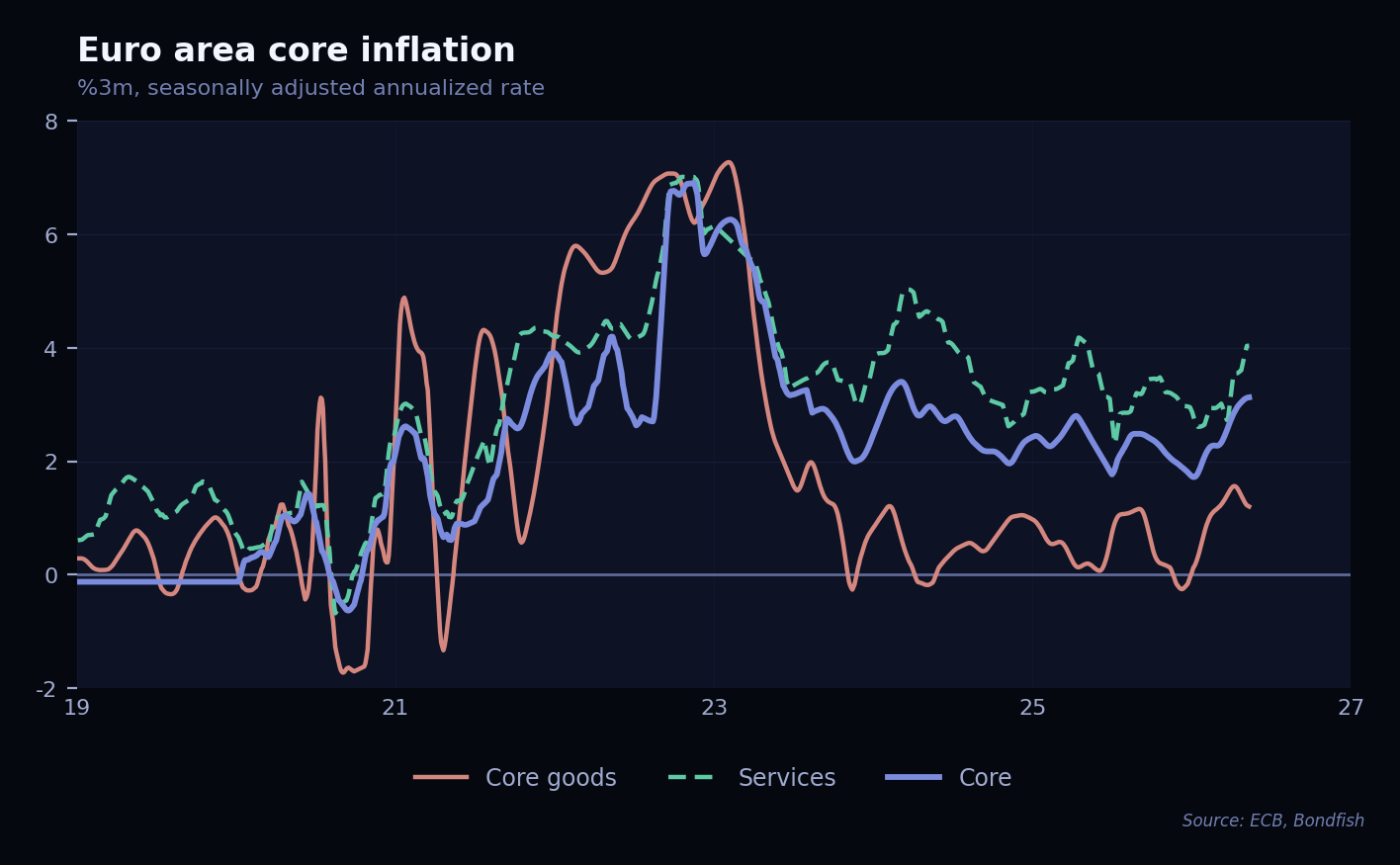

After a sharp rise in 2022, euro area core inflation has fallen back to around 2–2.5%. The main reason for the drop is core goods — things like clothes and appliances — which stopped getting more expensive as supply chains recovered. Services — think restaurants, travel, and rent — are a different story: prices there are still rising and have started picking up again in 2026, driven by higher wages. This is the key concern for the ECB ahead of next week's meeting, as the overall inflation picture looks better but services keep pushing back.