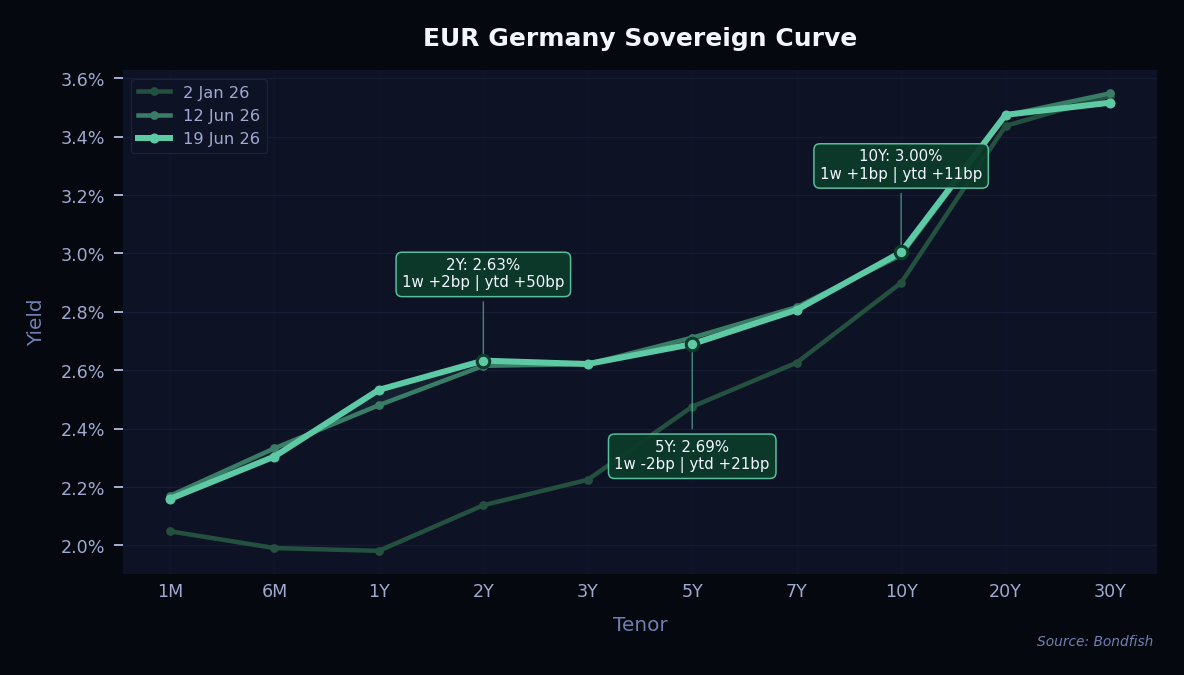

European yields were little changed, with no fresh catalyst to move them. With the European Central Bank widely expected to leave rates on hold, short-dated German yields edged up only slightly and longer maturities were flat to marginally lower. Signs of de-escalation in the Middle East calmed energy markets, which helped keep inflation expectations — and the curve — broadly steady.

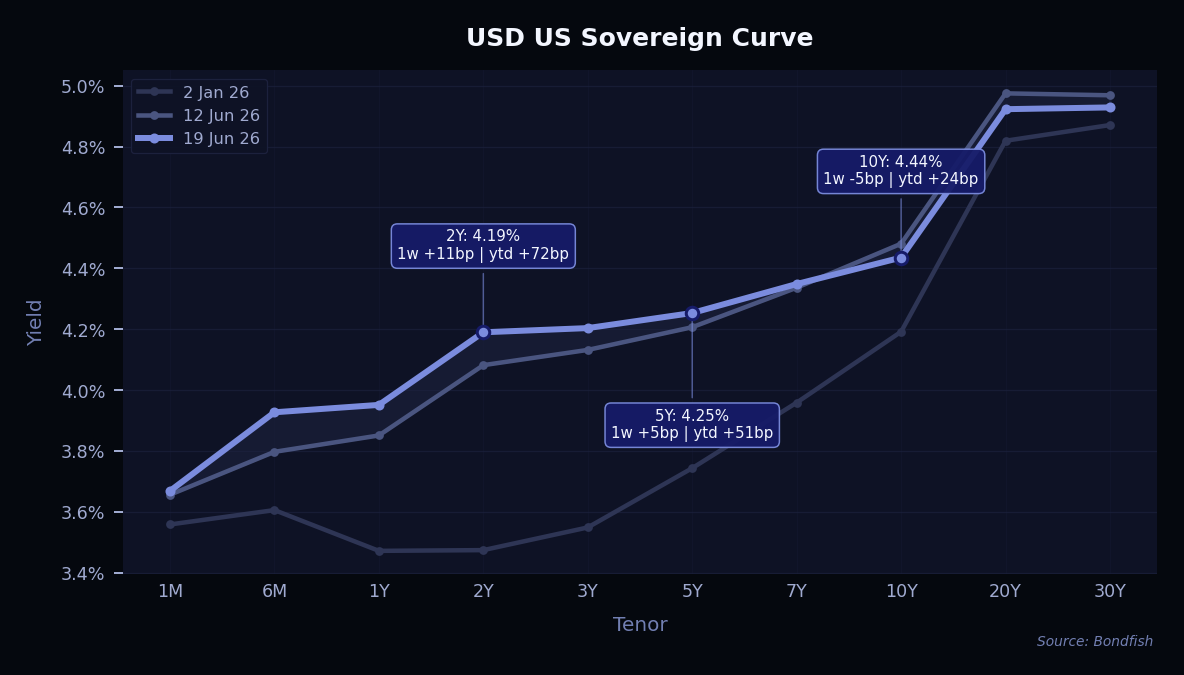

The big event was the Federal Reserve meeting — the first chaired by new Fed Chair Kevin Warsh. The Fed left interest rates unchanged, and investors listened closely for how the new chair would set the tone. With the Fed signalling it is in no hurry to cut while keeping a close eye on inflation, short-dated Treasury yields rose. At the long end, growing hopes for an end to the US-Iran conflict eased fears of an oil-price shock and pulled yields slightly lower — so the curve flattened, with the gap between short and long rates narrowing.

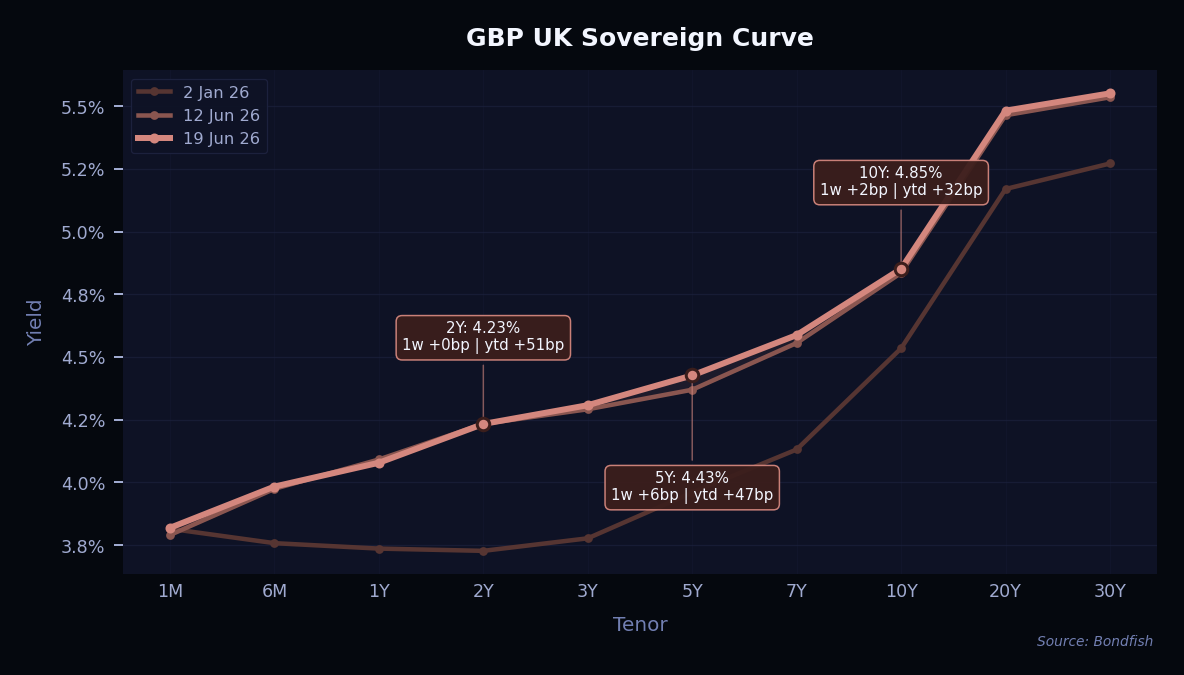

UK gilt yields drifted slightly higher across the board. With few domestic surprises, the move mainly echoed the global mood — central banks staying cautious while inflation proves sticky — rather than anything specific to Britain. The changes were small and fairly even along the curve.

The week's biggest gainers were a mixed group, helped by a calmer global backdrop as hopes grew for an end to the US-Iran conflict. Ukraine's 2035 bond led the way after its central bank held interest rates steady for a third meeting, pointing to progress toward peace in the Middle East and steady foreign aid. Wabash National rose after DA Davidson upgraded the company to Buy and sharply raised its share price target. Fiserv gained following a leadership change, with a long-serving executive taking over as chief executive. Mobico Group climbed after signing revised German rail contracts that should improve its operating profile.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| Ukraine 0% Feb 2035 | USD | 7,22% | 10,02% | VeryHigh |

|

Reason

The central bank held its key rate for a third meeting, citing Middle East peace progress and steady foreign-aid inflows

|

||||

| Wabash National 4.5% Oct 2028 | USD | 6,77% | 8,81% | VeryHigh |

|

Reason

DA Davidson upgraded the company to Buy and more than doubled its share price target, sending the stock sharply higher

|

||||

| Fiserv 4.4% Jul 2049 | USD | 5,49% | 5,93% | Medium |

|

Reason

The CEO stepped down after thirteen months and a long-time executive was promoted to lead the company immediately

|

||||

| TenneT Netherlan 1.125% Jun 2041 | EUR | 4,48% | 3,21% | Low |

|

Reason

No clear positive issuer catalyst

|

||||

| Mobico Group 3.625% Nov 2028 | GBP | 2,61% | 7,40% | VeryHigh |

|

Reason

Newly signed German rail contracts extended one route and shortened loss-making ones, improving the operating profile

|

||||

| Holcim Finance 1.375% Oct 2036 | EUR | 2,19% | 3,83% | Medium |

|

Reason

No clear positive issuer catalyst

|

||||

| Banque Postale 2.25% Oct 2028 | EUR | 2,12% | 2,28% | Medium |

|

Reason

No clear positive issuer catalyst

|

||||

| Legal Genral Fin 5.875% Dec 2031 | GBP | 0,97% | 4,63% | Low |

|

Reason

No clear positive issuer catalyst

|

||||

| TVL Finance 10.25% Apr 2028 | GBP | 0,44% | 14,25% | VeryHigh |

|

Reason

No clear positive issuer catalyst

|

||||

Losses were generally small and concentrated in longer-dated bonds. Whirlpool fell the most after it raised two billion dollars of new senior secured notes, which pushes existing bondholders further down the queue for repayment. Cameroon's 2032 bond slipped after the World Bank trimmed its growth forecast for Sub-Saharan Africa, citing higher energy costs and weaker demand. Peugeot (GIE PSA) (which we mentioned in our Top Picks) also drifted lower. The declines mostly reflected longer maturities and slightly higher yields rather than company-specific problems.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| Whirlpool 5.75% Mar 2034 | USD | -2,28% | 10,00% | High |

|

Reason

Two billion dollars of new senior secured notes were issued, subordinating existing bondholders and weighing on bond prices

|

||||

| Time Warner Cbl 5.875% Nov 2040 | USD | -2,22% | 7,14% | Medium |

|

Reason

No clear negative issuer catalyst

|

||||

| Charter Commn 5.5% Apr 2063 | USD | -1,87% | 7,41% | Medium |

|

Reason

No clear negative issuer catalyst; the ultra-long bond fell on its high duration as spreads widened modestly

|

||||

| Commerzbank 0.05% May 2029 | EUR | -1,39% | 2,86% | VeryLow |

|

Reason

No clear negative issuer catalyst

|

||||

| Bayerische Landesbank 0.62% May 2031 | EUR | -1,19% | 3,65% | Low |

|

Reason

No clear negative issuer catalyst

|

||||

| Peugeot (GIE PSA) 6% Sep 2033 | EUR | -1,16% | 4,45% | Medium |

|

Reason

No clear negative issuer catalyst

|

||||

| Cameroon 5.95% Jul 2032 | EUR | -1,14% | 8,39% | VeryHigh |

|

Reason

The World Bank cut its Sub-Saharan Africa growth forecast as higher energy costs and weak external demand bite

|

||||

Note: only long-term senior unsecured ratings were taken into account.

It was a busy week for upgrades, which outnumbered downgrades by a wide margin. The most notable move came from Suntory, the Japanese drinks group, which was lifted into the A category. Cybersecurity firm Crowdstrike crossed into investment grade, while Spanish retailer El Corte Ingles and tower operator SBA Communications also climbed a notch. A notable high-yield name, Xerox, climbed out of selective default (SD) back to CCC+. It had been marked in default only days earlier, after buying back some of its 2028 bonds below face value, and the rating was restored once the agency pointed to cost savings and progress integrating its Lexmark acquisition — though the outlook stays negative. On the downside, the cuts were concentrated in smaller, lower-rated companies such as Aventiv, Flexsys and Mountain Province Diamonds, several of which moved deeper into distressed territory. There were few downgrades among large, well-known issuers.

| Issuer | Agency | Change |

| Accor | Fitch | BBB- → BBB |

| Alexandria Real Estate Equities | Moody's | Baa1 → Baa2 |

| Aventiv Technologies | S&P | CCC- → CC |

| Banco de Desenvolvimento de Minas Gerais | Moody's | B1 → Ba3 |

| Banco Latinoamericano de Comercio Exterior | S&P | BBB → BBB+ |

| Bank Handlowy w Warszawie | Fitch | A- → A+ |

| Biscuit | Fitch | RD → CCC |

| Brazos Permian II | S&P | B+ → BBB- |

| China Hainan Rubber Industry | Fitch | BBB → BBB+ |

| Constantia Flexibles | S&P | B- (new) |

| Contemporary Amperex Technology | Fitch | A- → A |

| Criteria Caixa | Fitch | BBB+ → A- |

| Crowdstrike | S&P | BB+ → BBB- |

| Dynasty Acquisition | S&P | BB- → BB |

| El Corte Ingles | S&P | BBB- → BBB |

| Flexsys | S&P | CCC+ → CCC- |

| Hainan State Farms Investment | Fitch | BBB → BBB+ |

| Hefei Industry Investment | Fitch | BBB → BBB+ |

| House of HR | S&P | B → B- |

| HOWOGE | Fitch | AA- → AA+ |

| Intrum | S&P | CCC+ → B- |

| Jiangxi Provincial Water Conservancy Investment | Moody's | Baa1 → A3 |

| Jiangxi Railway & Aviation Investment | Moody's | A3 → A2 |

| Liftoff Mobile | S&P | B- → BB- |

| MAG DS | S&P | B- → CCC |

| Martin Marietta Materials | Fitch | BBB → BBB+ |

| Mountain Province Diamonds | S&P | CCC- → SD |

| Pluspetrol | Fitch | BBB+ → BBB |

| Public Power | S&P | BB- → BB |

| SBA Communications | S&P | BBB- → BBB |

| Scotts Miracle-Gro | S&P | B+ → BB- |

| Securus | S&P | CCC- → CC |

| Sensience | S&P | SD → CCC+ |

| Shandong Land Development | Fitch | BBB+ → A- |

| Suntory | S&P | BBB+ → A- |

| Viavi Solutions | S&P | B+ → BB |

| Wan Hai Lines | Moody's | Baa3 (new) |

| Xerox | S&P | SD → CCC+ |

| Yuexiu Transport Infrastructure | Fitch | BBB → BBB+ |

| ZoomInfo Technologies | S&P | BB → BB- |

New bond supply stayed busy even as the summer slowdown began. Companies rushed to borrow while spreads sat near their tightest levels in years and investors looked for places to put cash to work. Technology giant NVIDIA dominated the week with a massive 21.5 billion dollar multi-part deal. Other large sales came from Vodafone, Qatar Energy, NextEra Energy and Barclays, alongside a string of European banks such as BBVA, Intesa Sanpaolo and BNP Paribas. Investor demand was strong, helped by growing optimism around an end to the US-Iran conflict. Floating-rate deals were especially popular, as buyers positioned for the chance that interest rates stay higher for longer.

| Issuer | Size | Term | Yield | Risk Level |

| ADI Escrow Issuer | USD 0,40bn |

8Y | 7,1% | High |

|

ISIN (CUSIP)

USU00693AA60

|

||||

| Africa Finance Corporation | USD 0,50bn |

5Y | 5,5% | Low |

|

ISIN (CUSIP)

XS3296851010

|

||||

| Anglian Water Services Financing | EUR 0,70bn |

10Y | 4,4% | Medium |

|

ISIN (CUSIP)

XS3413969059

|

||||

| Athens International Airport | EUR 0,50bn |

7Y | 3,8% | Medium |

|

ISIN (CUSIP)

XS3325244963

|

||||

| Atmos Energy | USD 0,70bn |

6Y | 4,8% | Low |

|

ISIN (CUSIP)

049560BF1

|

||||

| Ayvens | EUR 0,50bn |

6Y | 3,5% | Low |

|

ISIN (CUSIP)

FR0014019BT2

|

||||

| BBVA | EUR 2,2bn |

3–7Y | 2,9–3,1% | Very Low |

|

ISIN (CUSIP)

ES0413211B41…ES0413211B58

|

||||

| Banco Comercial Portugues | EUR 0,50bn |

12Y | 4,2% | Medium |

|

ISIN (CUSIP)

PTBCPOOM0034

|

||||

| Banco Mercantil del Norte | USD 0,75bn |

PERP | 8,0–8,4% | High |

|

ISIN (CUSIP)

USP1400MAF51…USP1400MAG35

|

||||

| Banco Montepio | EUR 0,35bn |

5Y | 3,7% | Medium |

|

ISIN (CUSIP)

PTCMGBOM0045

|

||||

| Banco Santander | EUR 1,0bn |

7Y | 3,7% | Low |

|

ISIN (CUSIP)

XS3417309021

|

||||

| Bank AlJazira | USD 0,50bn |

PERP | 6,5% | Very High |

|

ISIN (CUSIP)

XS3401945517

|

||||

| Barclays | USD 4,5bn |

4–11Y | 4,9–5,6% | Low |

|

ISIN (CUSIP)

US06738EDL65…US06738EDN22

|

||||

| BAWAG P.S.K. | EUR 0,50bn |

3Y | 3,1% | Low |

|

ISIN (CUSIP)

XS3413306617

|

||||

| Bayerische Landesbank | EUR 0,50bn |

3Y | 2,8% | Very Low |

|

ISIN (CUSIP)

DE000BYL0J59

|

||||

| Beazer Homes USA | USD 0,40bn |

6Y | 8,0% | Very High |

|

ISIN (CUSIP)

07556QBV6

|

||||

| Birkenstock | EUR 0,90bn |

7Y | 4,5% | High |

|

ISIN (CUSIP)

XS3410944709

|

||||

| BNP Paribas | EUR 1,0bn |

10Y | 4,0% | Low |

|

ISIN (CUSIP)

FR00140199V7

|

||||

| BPCE | EUR 1,0bn |

8Y | 3,9% | Low |

|

ISIN (CUSIP)

FR0014019BB0

|

||||

| Caisse de Refinancement de l'Habitat | EUR 0,75bn |

7Y | 3,3% | Very Low |

|

ISIN (CUSIP)

FR0014019DU6

|

||||

| California Resources | USD 0,55bn |

8Y | 7,2% | Very High |

|

ISIN (CUSIP)

USU1303AAK26

|

||||

| Canadian Imperial Bank of Commerce | EUR 1,4bn |

2Y | FLOAT, +40bp | Low |

|

ISIN (CUSIP)

XS3420476452

|

||||

| Canary Islands | EUR 0,50bn |

10Y | 3,5% | Very High |

|

ISIN (CUSIP)

ES0000093502

|

||||

| Charlotte Buyer | USD 0,50bn |

5Y | 8,0% | Very High |

|

ISIN (CUSIP)

USU15921AA47

|

||||

| China Education Group Holdings | USD 0,20bn |

3Y | 6,0% | Very High |

|

ISIN (CUSIP)

XS3256590251

|

||||

| CPI Property Group | EUR 0,55bn |

PERP | 9,2% | Very High |

|

ISIN (CUSIP)

XS3412577515

|

||||

| Credit Agricole Italia | EUR 1,0bn |

11Y | 3,6% | Very Low |

|

ISIN (CUSIP)

IT0005715724

|

||||

| EEW Energy from Waste | EUR 0,56bn |

3Y | 4,0% | Medium |

|

ISIN (CUSIP)

XS3385465482

|

||||

| Equipmentshare | USD 1,4bn |

PERP | 7,1% | Very High |

|

ISIN (CUSIP)

USU26947AE81

|

||||

| European Energy | EUR 0,10bn |

1000Y | 10,5% | Very High |

|

ISIN (CUSIP)

DK0030576582

|

||||

| Experian Finance US | USD 1,0bn |

10Y | 5,4% | Low |

|

ISIN (CUSIP)

USU3010WAA63

|

||||

| Ferrovie dello Stato Italiane | EUR 0,65bn |

5Y | 3,3% | Medium |

|

ISIN (CUSIP)

XS3420368998

|

||||

| First Abu Dhabi Bank | EUR 0,75bn |

4Y | 3,5% | Very Low |

|

ISIN (CUSIP)

XS3420391628

|

||||

| First-Citizens Bank | USD 0,75bn |

3Y | 5,1% | Medium |

|

ISIN (CUSIP)

US337967AA13

|

||||

| Fiserv | EUR 1,0bn |

4–8Y | 3,8–4,3% | Medium |

|

ISIN (CUSIP)

XS3410940897…XS3410941192

|

||||

| HDFC Bank | USD 0,75bn |

5Y | 5,1% | Medium |

|

ISIN (CUSIP)

XS3418550631

|

||||

| HT Troplast | EUR 0,43bn |

5Y | 7,6% | Very High |

|

ISIN (CUSIP)

XS3415269490

|

||||

| Hybar | USD 0,40bn |

8Y | 7,4% | Very High |

|

ISIN (CUSIP)

USU4485JAA98

|

||||

| Hyundai Capital America | EUR 0,55bn |

6Y | 3,7% | Low |

|

ISIN (CUSIP)

XS3319132513

|

||||

| Hyundai Capital America | USD 2,4bn |

2–7Y | 4,6–5,3% | Low |

|

ISIN (CUSIP)

US44891CEM10…US44891CEQ24

|

||||

| Iberdrola Finanzas | EUR 1,5bn |

4–10Y | 3,2–3,8% | Medium |

|

ISIN (CUSIP)

XS3418565829…XS3418566124

|

||||

| Intesa Sanpaolo | EUR 1,2bn |

8Y | 3,8% | Medium |

|

ISIN (CUSIP)

IT0005717589

|

||||

| Investitionsbank des Landes Brandenburg | EUR 0,25bn |

3Y | 2,8% | Very Low |

|

ISIN (CUSIP)

DE000A460NF8

|

||||

| ISB Rheinland-Pfalz | EUR 0,50bn |

10Y | 3,3% | Very Low |

|

ISIN (CUSIP)

DE000A460KN8

|

||||

| Iron Mountain | USD 1,5bn |

8Y | 6,2% | High |

|

ISIN (CUSIP)

USU46009AQ64

|

||||

| KBC Groep | GBP 0,50bn |

6Y | 5,1% | Low |

|

ISIN (CUSIP)

BE0390361336

|

||||

| Lanxess | EUR 0,50bn |

5Y | 4,6% | High |

|

ISIN (CUSIP)

XS3402928637

|

||||

| Latvenergo | EUR 0,30bn |

7Y | 4,2% | Medium |

|

ISIN (CUSIP)

XS3412686563

|

||||

| Mediobanca | EUR 0,50bn |

6Y | 3,2% | Very Low |

|

ISIN (CUSIP)

IT0005717944

|

||||

| MM Mirage Bluewater II | USD 0,55bn |

3Y | 9,0% | Very High |

|

ISIN (CUSIP)

NO0013756403

|

||||

| Monitchem Holdco 3 | EUR 0,62bn |

5Y | 8,0% | Very High |

|

ISIN (CUSIP)

XS3420263629

|

||||

| NextEra Energy Capital Holdings | USD 3,8bn |

30–40Y | 6,0–6,6% | Medium |

|

ISIN (CUSIP)

US65339KEF30…US65339KEH95

|

||||

| NVIDIA | USD 21,5bn |

2–30Y | 4,3–5,6% | Very Low |

|

ISIN (CUSIP)

US67066GAP90…US67066GAT13

|

||||

| Nykredit Realkredit | EUR 0,75bn |

7Y | 3,9% | Low |

|

ISIN (CUSIP)

DK0030566781

|

||||

| Orange | EUR 0,85bn |

PERP | 4,4% | Medium |

|

ISIN (CUSIP)

FR00140194B0

|

||||

| OTP Bank | EUR 1,0bn |

10Y | 4,7% | High |

|

ISIN (CUSIP)

XS3406852536

|

||||

| Paccar Financial | USD 0,30bn |

3Y | 4,3% | Low |

|

ISIN (CUSIP)

69371RU53

|

||||

| Paprec Holding | EUR 0,40bn |

4–6Y | -- | Very High |

|

ISIN (CUSIP)

XS3111830959…XS3111831254

|

||||

| Republic of the Philippines | USD 2,5bn |

6–25Y | 4,7–5,8% | Medium |

|

ISIN (CUSIP)

US718286DN44…US718286DL87

|

||||

| PKO Bank Polski | EUR 0,50bn |

10Y | 4,1% | Medium |

|

ISIN (CUSIP)

XS3404490883

|

||||

| Qatar Energy | USD 3,5bn |

3Y | 4,6% | Very High |

|

ISIN (CUSIP)

XS3401028785

|

||||

| Raiffeisenlandesbank Oberösterreich | EUR 0,50bn |

5Y | 3,0% | Very Low |

|

ISIN (CUSIP)

AT0000A3VG25

|

||||

| Sammons Financial Group Global Funding | USD 0,50bn |

5Y | 5,1% | Low |

|

ISIN (CUSIP)

US79587K2F60

|

||||

| Seadrill Finance | USD 0,70bn |

8Y | 6,8% | Very High |

|

ISIN (CUSIP)

USG8001GAC36

|

||||

| Snam | EUR 0,75bn |

10Y | 3,9% | Medium |

|

ISIN (CUSIP)

XS3406814445

|

||||

| Southern Copper | USD 1,2bn |

10Y | 5,4% | Medium |

|

ISIN (CUSIP)

US84265VAK17

|

||||

| Supernova Invest | EUR 0,30bn |

5Y | 4,5% | Medium |

|

ISIN (CUSIP)

XS3415292989

|

||||

| Synergy Infrastructure Holdings | USD 0,45bn |

8Y | 7,0% | Very High |

|

ISIN (CUSIP)

USU8077RAB43

|

||||

| TAP Air Portugal | EUR 0,35bn |

5Y | 4,9% | High |

|

ISIN (CUSIP)

PTTAPBOM0015

|

||||

| Unicaja Banco | EUR 0,70bn |

7Y | 3,8% | Medium |

|

ISIN (CUSIP)

ES0280907066

|

||||

| UniCredit Bank Austria | EUR 0,75bn |

6Y | 3,1% | Very Low |

|

ISIN (CUSIP)

AT000B050000

|

||||

| UniCredit | EUR 0,60bn |

2Y | FLOAT, +38bp | Low |

|

ISIN (CUSIP)

IT0005717902

|

||||

| Union Electric | USD 0,50bn |

30Y | 5,8% | Low |

|

ISIN (CUSIP)

US906548DD17

|

||||

| Versuni | EUR 0,55bn |

7Y | 5,8% | Very High |

|

ISIN (CUSIP)

XS3418671189

|

||||

| Vittoria Assicurazioni | EUR 0,20bn |

10Y | 4,8% | Medium |

|

ISIN (CUSIP)

XS3402829652

|

||||

| Vodafone Group | USD 3,5bn |

5–30Y | 4,8–6,1% | Medium |

|

ISIN (CUSIP)

US92857WCC29…US92857WCE84

|

||||

| Well Link Life Insurance | USD 0,20bn |

10Y | 8,0% | High |

|

ISIN (CUSIP)

XS3389599310

|

||||

| Wolters Kluwer | EUR 0,50bn |

7Y | 3,7% | Very High |

|

ISIN (CUSIP)

XS3395917761

|

||||

| Zurich Finance | USD 0,50bn |

7Y | 5,0% | Very Low |

|

ISIN (CUSIP)

XS3418658756

|

||||

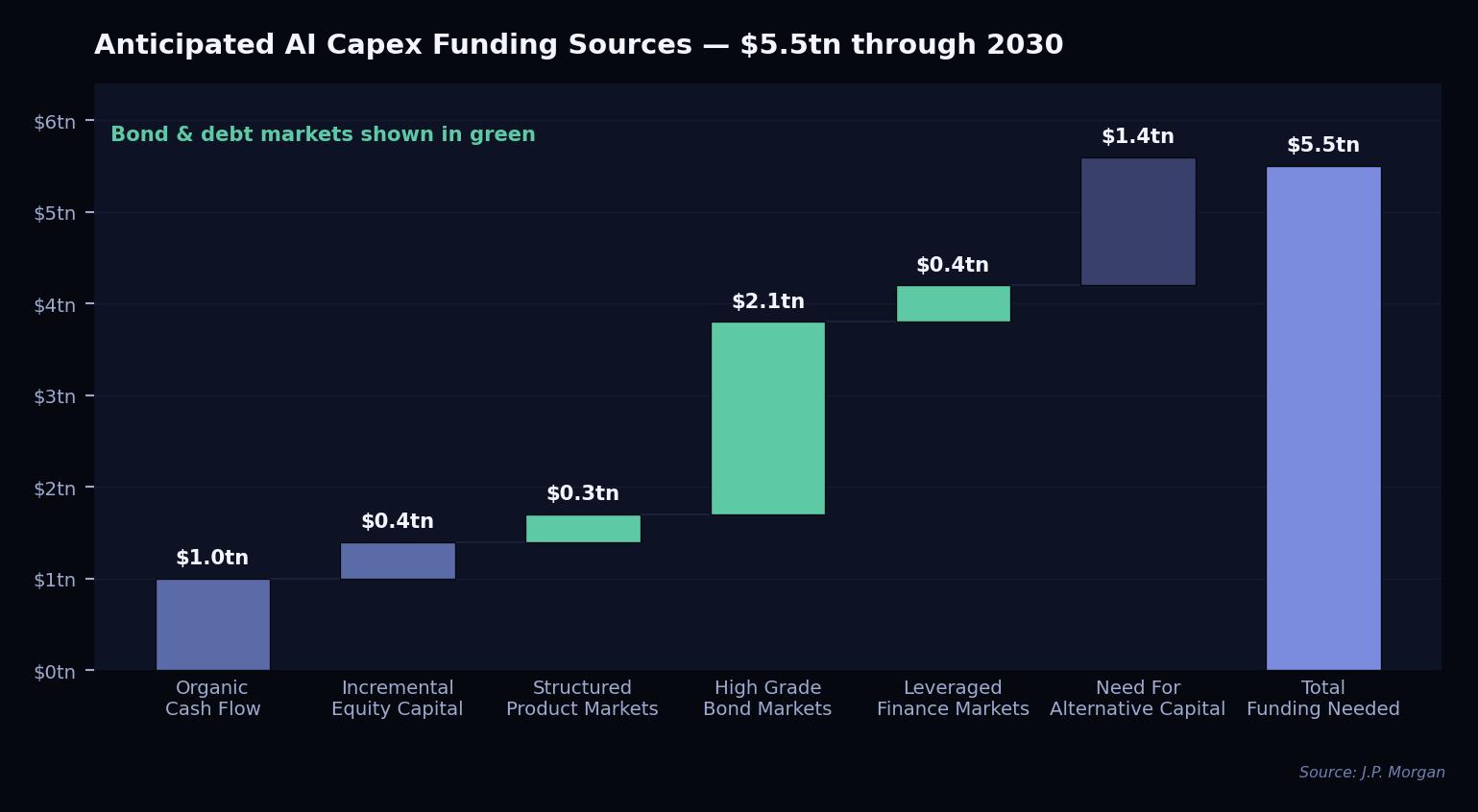

This week's chart shows how the AI boom is likely to be paid for. By J.P. Morgan's estimates, building out AI data centers will cost around $5.5 trillion over the next five years, and the chart maps where that money will come from. Companies can cover about $1.0 trillion from their own cash flow and roughly $0.4 trillion by issuing new shares. The rest leans heavily on borrowing: about $2.1 trillion from high-grade bonds, $0.4 trillion from leveraged finance and $0.3 trillion from structured products. That still leaves around $1.4 trillion that J.P. Morgan expects to come from alternative sources of capital. The takeaway for bond investors is clear — bonds are set to do most of the heavy lifting, pointing to a large wave of new issuance in the years ahead.

.png)