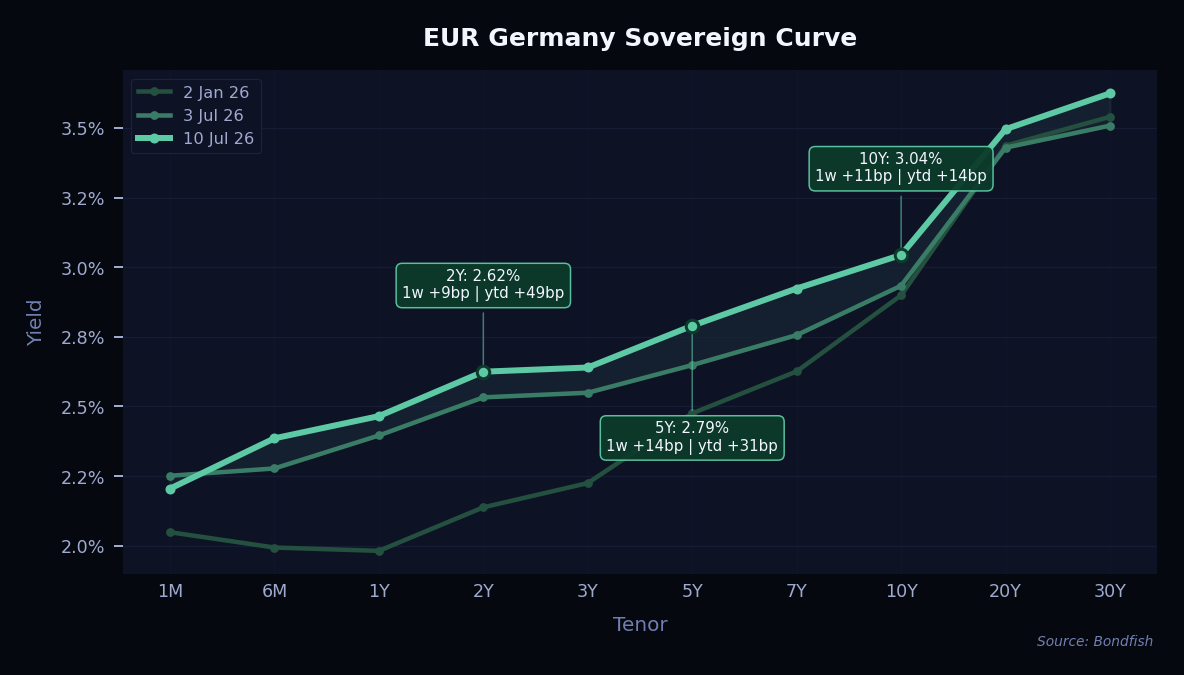

German government bond yields rose across the whole curve this week. The trigger was a fresh flare-up in US–Iran tensions, which pushed energy prices and inflation worries back to the front of investors’ minds. That prompted a broad sell-off in government bonds, lifting the 10-year Bund yield about 13 basis points to just above 3%. The move was fairly even across maturities, with the 2-year and 5-year also up around 11 basis points. With the risk of a bigger energy shock seen as contained, yields settled near the top of their recent range rather than breaking out.

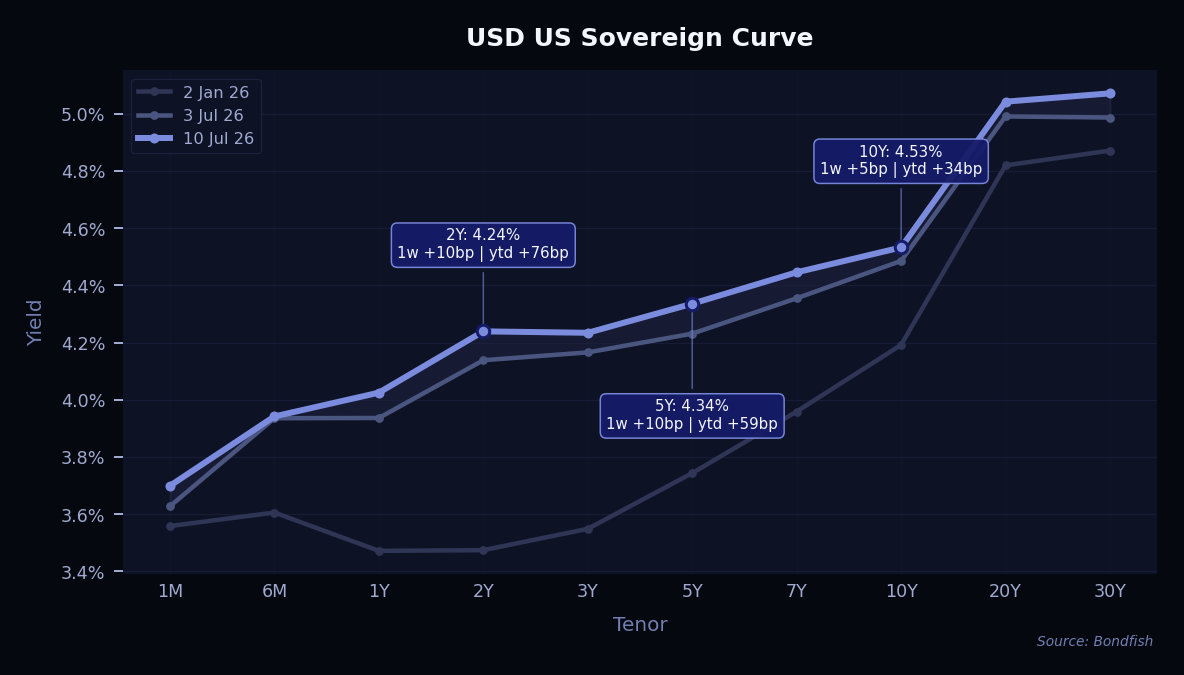

US Treasury yields climbed too, for much the same reason. Renewed Middle East tensions revived inflation concerns and led investors to trim bets on near-term Federal Reserve rate cuts. The 10-year yield rose about 8 basis points to 4.56%, while shorter maturities moved up a touch more. Minutes from the last Fed meeting added little new direction. Long-dated yields stayed high, partly because rising Japanese government yields have kept upward pressure on global long-term rates.

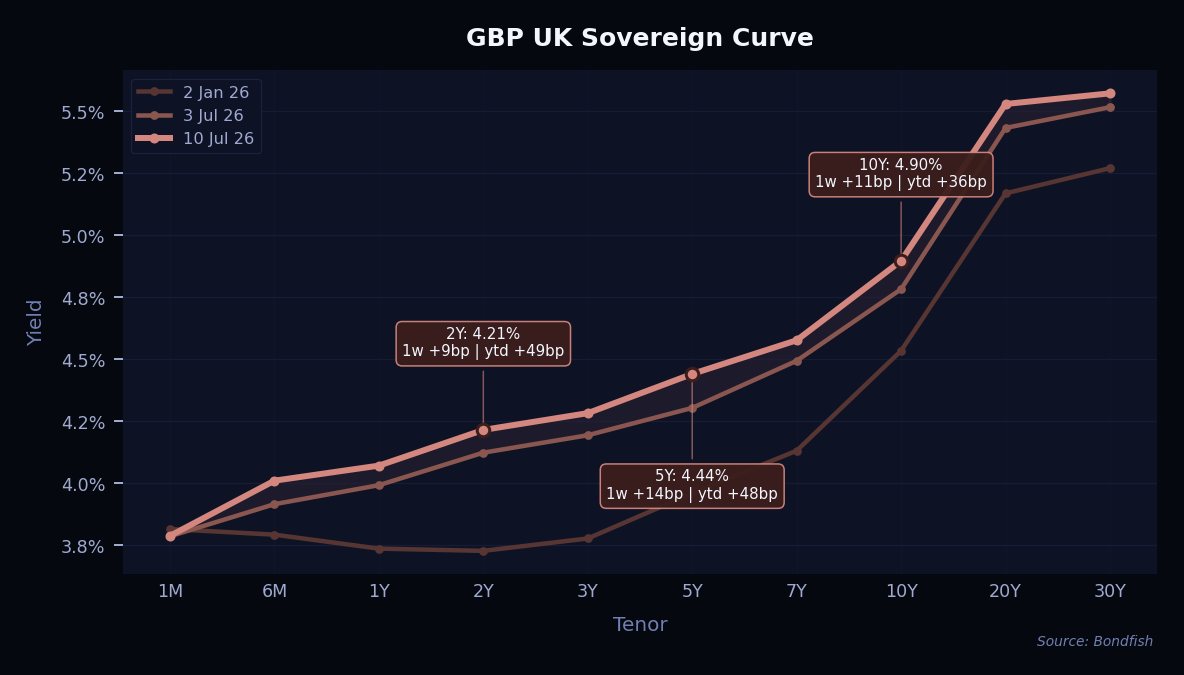

UK gilt yields followed the same global pattern, rising 9 to 11 basis points across most of the curve. The energy-driven jump in inflation expectations was the main driver here as well. On top of that, gilts still carry a small extra yield premium tied to uncertainty about the UK’s medium-term public finances. The 10-year gilt yield ended the week near 4.88%.

The current preference is to lean into European government bonds — both German Bunds and UK gilts — on the view that this yield spike fades as energy risks stay contained, favouring European bonds over their US equivalents.

This week’s biggest gainers were concentrated in shorter-dated and higher-yielding bonds, which were largely shielded from the sell-off at the long end of the curve. Ukraine’s sovereign bonds led the way, with Ukraine 0% 2036 and Ukraine 4.5% 2034 both rising around 2% and Ukraine 4.5% 2035 close behind. The high-yield People US 7.625% 2032 also featured near the top. Steady demand for income helped these prices push higher even as government yields rose.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| Ukraine 0% Feb 2036 | USD | 2,53% | 9,65% | VeryHigh |

| Ukraine 4.5% Feb 2034 | USD | 1,98% | 11,23% | VeryHigh |

| People US 7.625% Jun 2032 | USD | 1,94% | 8,20% | VeryHigh |

| Ukraine 4.5% Feb 2035 | USD | 1,58% | 11,31% | VeryHigh |

| Alliant En Fin 5.4% Jun 2027 | USD | 1,34% | 2,77% | Medium |

| KFW 1% Oct 2026 | USD | 1,27% | -1,71% | VeryLow |

| Adecoagro 7.5% Jul 2032 | USD | 1,24% | 8,23% | VeryHigh |

| Southern Co Gas 6% Oct 2034 | USD | 1,20% | 4,99% | Medium |

| RELIANCE STANDARD LIFE 2.75% Jan 2027 | USD | 1,19% | 2,52% | Low |

| Beazer Homes USA 7.5% Mar 2031 | USD | 1,18% | 6,73% | VeryHigh |

The losers were almost all very long-dated, high-quality corporate bonds — the part of the market most sensitive to rising long-term yields. Amazon.com 4.1% 2062, Meta Platforms 5.4% 2054 and Meta Platforms 5.6% 2053 all fell around 4%, along with Amazon.com 4.25% 2057. A wave of fresh long-dated supply from these same issuers added to the pressure on their existing bonds. The single worst performer was CSN Inova 6.75% 2028, down more than 5% on company-specific concerns.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| CSN Inova 6.75% Jan 2028 | USD | -5,34% | 24,21% | VeryHigh |

| Amazon.com 4.1% Apr 2062 | USD | -4,33% | 6,13% | VeryLow |

| Meta Platforms 5.4% Aug 2054 | USD | -4,15% | 6,58% | VeryLow |

| Meta Platforms 5.6% May 2053 | USD | -4,12% | 6,60% | VeryLow |

| Amazon.com 4.25% Aug 2057 | USD | -4,11% | 6,12% | VeryLow |

| Oracle 5.375% Sep 2054 | USD | -4,06% | 7,55% | Medium |

| Oracle 6% Aug 2055 | USD | -4,03% | 7,58% | Medium |

| Oracle 5.55% Feb 2053 | USD | -3,95% | 7,57% | Medium |

| Meta Platforms 5.55% Aug 2064 | USD | -3,94% | 6,75% | VeryLow |

| Oracle 4% Nov 2047 | USD | -3,89% | 7,37% | Medium |

Note: only long-term senior unsecured ratings were taken into account.

Upgrades outnumbered downgrades this week, 17 to 13. The standout upgrade was Syngenta, lifted two notches to A-, alongside a one-notch rise for Spanish lender CaixaBank to A+. On the downside, Oracle slipped one step to BBB-, keeping it only just inside investment grade, while Harley-Davidson was cut to BB+ and now sits in high-yield territory. Cosmetics group Coty was also downgraded a notch.

| Issuer | Agency | Change |

| Andre Maggi Participacoes | Fitch | BB- → B+ |

| Athletico | S&P | CCC+ → CC |

| Banistmo | Fitch | BB+ → BB |

| Banque Tuniso-Koweitienne de Developpement | Fitch | CCC- → CCC |

| BWX Technologies | S&P | BB → BB+ |

| CaixaBank | Fitch | A → A+ |

| Century Communities | S&P | BB → BB- |

| CNPC Finance HK | Moody's | A2 → A1 |

| Cosan | S&P | BB- → B+ |

| Coty | S&P | BB+ → BB |

| E.Sun Financial | Moody's | A2 → A3 |

| First Bancorp | Fitch | BB+ → BBB- |

| FS Bioenergia | Fitch | BB- → B+ |

| Harley-Davidson | S&P | BBB- → BB+ |

| Intermediate Dutch | S&P | B → B+ |

| JSW Steel | Fitch | BB → BB+ |

| Kawasan Industri Jababeka Tbk PT | Fitch | B- → B |

| Navoiyuran State Enterprise | S&P | BB- → BB |

| NES Fircroft Bondco | S&P | B+ → B |

| Oracle | S&P | BBB → BBB- |

| Padagis | Fitch | B+ → B |

| Popular | Fitch | BBB- → BBB |

| Poseidon Bidco SASU | S&P | SD → CCC- |

| Quincy Health | S&P | SD → CCC- |

| Sinopec Century Bright Capital Investment | Moody's | A2 → A1 |

| Syngenta | Fitch | BBB → A- |

| Syniverse | S&P | B- → CCC |

| Tianjin Rail Transit | S&P | BBB+ (new) |

| Uzauto Motors AJ | Fitch | BB- → BB |

| Watergate Software | S&P | BB → BB+ |

Primary markets were exceptionally busy. The headline deal came from Amazon, which returned with a jumbo, multi-part offering stretching from 2 to 40 years across both dollars and euros. Governments and agencies were also active, including a large European Union dual-tranche sale, new KfW dollar bonds and a three-part Italy dollar deal. Utilities and banks rounded out the supply, with names such as Enel, TenneT and Accenture all tapping the market. Demand was firm throughout, and strong fund inflows into both investment-grade and high-yield credit helped absorb the heavy issuance.

| Issuer | Size | Term | Yield | Risk Level |

| Accenture Capital | USD 5,0bn |

3–10Y | 4,8–5,6%; FLOAT | Very Low |

|

ISIN (CUSIP)

US00440KAF03…US00440KAJ25

|

||||

| Action Logement Services | EUR 0,80bn |

10Y | 4,1% | Very High |

|

ISIN (CUSIP)

FR0014019WJ9

|

||||

| Agence Francaise de Developpement | EUR 1,0bn |

15Y | 4,4% | Low |

|

ISIN (CUSIP)

FR0014019UO3

|

||||

| Air Philippines | USD 0,30bn |

5Y | 8,0% | High |

|

ISIN (CUSIP)

USG7261AAA72

|

||||

| Ajman Tier 1 Sukuk | USD 0,30bn |

PERP | 6,5% | Very High |

|

ISIN (CUSIP)

XS3310391878

|

||||

| Amazon | EUR 3,0bn |

2Y | 2,8%; FLOAT, +35bp | Very Low |

|

ISIN (CUSIP)

XS3317524950

|

||||

| Amazon | USD 147,7bn |

2–40Y, PERP | 1,1–80,8%; FLOAT | Low |

|

ISIN (CUSIP)

US023135CD60…US023135EH56

|

||||

| Anglian Water Services Financing | GBP 0,15bn |

7Y | 5,4% | Medium |

|

ISIN (CUSIP)

XS3225307902

|

||||

| Aroundtown | EUR 0,85bn |

5Y | 4,2% | Very High |

|

ISIN (CUSIP)

XS3440165937

|

||||

| Autozone | USD 0,85bn |

5Y | 5,0% | Medium |

|

ISIN (CUSIP)

US053332BN18

|

||||

| Babcock International Group | GBP 0,25bn |

5Y | 5,2% | Very High |

|

ISIN (CUSIP)

XS3437585022

|

||||

| Bank Of Montreal | USD 2,0bn |

3Y | 4,4% | Very Low |

|

ISIN (CUSIP)

USC0623PJD18

|

||||

| Bank Pekao | EUR 0,50bn |

11Y | 4,3% | Very High |

|

ISIN (CUSIP)

XS3438593926

|

||||

| Banque Federative Du Credit Mutuel | USD 3,2bn |

3–6Y | 4,8–5,2%; FLOAT | Very Low |

|

ISIN (CUSIP)

06675DCW0

|

||||

| State of Berlin | EUR 0,50bn |

7Y | 3,0% | Very Low |

|

ISIN (CUSIP)

DE000A4DE9P1

|

||||

| Bpifrance | EUR 1,5bn |

7Y | 3,4% | Very Low |

|

ISIN (CUSIP)

FR0014019RX0

|

||||

| Bulgaria | EUR 2,5bn |

6–19Y | 3,5–4,7% | Medium |

|

ISIN (CUSIP)

XS2890420834…XS3124393367

|

||||

| Canadian Imperial Bank Of Commerce | USD 0,50bn |

61Y | 6,8% | Medium |

|

ISIN (CUSIP)

US13607Q7E68

|

||||

| Cirsa Finance | EUR 0,50bn |

6Y | 4,6% | High |

|

ISIN (CUSIP)

XS3436174372

|

||||

| Commercial Bank of Dubai | USD 0,60bn |

PERP | 6,6% | Very High |

|

ISIN (CUSIP)

XS3323686728

|

||||

| Deere Funding Canada | USD 0,30bn |

5Y | 4,9% | Low |

|

ISIN (CUSIP)

US2442GAAB82

|

||||

| Deutsche Bank | EUR 1,0bn |

6Y | 3,7% | Medium |

|

ISIN (CUSIP)

DE000A5GS0P0

|

||||

| Enel Finance International | USD 2,5bn |

3–10Y | 4,7–5,5% | Medium |

|

ISIN (CUSIP)

USN3070QAE63…USN3070QAG12

|

||||

| Energy Transfer | USD 1,8bn |

30–31Y | 6,5–6,7% | Medium |

|

ISIN (CUSIP)

US29273VBM19

|

||||

| European Financial Stability Facility | EUR 2,5bn |

4Y | 3,0% | Very Low |

|

ISIN (CUSIP)

EU000A2SCAJ7

|

||||

| European Outlet Mall Venture | EUR 0,75bn |

5Y | 4,3% | Medium |

|

ISIN (CUSIP)

XS3415298838

|

||||

| European Union | EUR 11,0bn |

5–20Y | 2,9–4,0% | Very Low |

|

ISIN (CUSIP)

EU000A4EXVK3…EU000A4ES497

|

||||

| Figure Technologies | USD 0,60bn |

5Y | 8,5% | Very High |

|

ISIN (CUSIP)

USU3170FAA94

|

||||

| Fr Midco | EUR 0,78bn |

6Y | FLOAT, +300bp | Very High |

|

ISIN (CUSIP)

XS3439943203

|

||||

| Fubon Bank (Hong Kong) | USD 0,30bn |

10Y | 5,5% | Very High |

|

ISIN (CUSIP)

XS3420731666

|

||||

| Guardian Life Global Funding | USD 0,70bn |

3Y | 4,7% | Very Low |

|

ISIN (CUSIP)

40139MBS9

|

||||

| Hungary | EUR 1,5bn |

11Y | 4,3% | Medium |

|

ISIN (CUSIP)

XS3435288769

|

||||

| Intercorp Peru | USD 0,30bn |

PERP | 5,7% | Medium |

|

ISIN (CUSIP)

USP5625XAD68

|

||||

| International Finance | EUR 1,0bn |

7Y | 3,1% | Very Low |

|

ISIN (CUSIP)

XS3440163569

|

||||

| International Finance | USD 2,0bn |

5Y | 4,3% | Very Low |

|

ISIN (CUSIP)

USU4R844FS44

|

||||

| Italy | USD 6,0bn |

5–30Y | 4,6–6,1% | Medium |

|

ISIN (CUSIP)

XS3441656454…XS3441656702

|

||||

| Jefferies Financial Group | EUR 0,85bn |

7Y | 4,5% | Medium |

|

ISIN (CUSIP)

XS3435704575

|

||||

| KfW | USD 6,0bn |

3–7Y | 4,3–4,5% | Very Low |

|

ISIN (CUSIP)

US500769KR49…US500769KS22

|

||||

| Korea East West Power | USD 0,50bn |

6Y | 4,8% | Very High |

|

ISIN (CUSIP)

HK0001319182

|

||||

| South Korea | EUR 1,7bn |

3–7Y | 3,0–3,3% | Very Low |

|

ISIN (CUSIP)

XS3437347431…XS3437347787

|

||||

| KT Corp | USD 0,50bn |

3Y | 4,7% | Low |

|

ISIN (CUSIP)

USY49915BF08

|

||||

| Lloyds Bank Corporate Markets | EUR 0,50bn |

5Y | 3,4% | Very Low |

|

ISIN (CUSIP)

XS3435287365

|

||||

| Loxam | EUR 1,1bn |

5–6Y | 4,6–5,0% | Very High |

|

ISIN (CUSIP)

XS3439957682…XS3439957849

|

||||

| MBH Bank | EUR 0,50bn |

6Y | 5,5% | High |

|

ISIN (CUSIP)

XS3433787341

|

||||

| Mediocredito Centrale | EUR 0,50bn |

6Y | 3,8% | Very High |

|

ISIN (CUSIP)

IT0005723066

|

||||

| Mileway | EUR 1,5bn |

4–7Y | 4,0–4,4% | Medium |

|

ISIN (CUSIP)

XS3439307045…XS34393071283

|

||||

| National Grid North America | EUR 1,3bn |

5–11Y | 3,6–4,3% | Medium |

|

ISIN (CUSIP)

XS3441767442…XS3441768093

|

||||

| Nationwide Building Society | USD 1,8bn |

6–11Y | 5,1–5,5% | Low |

|

ISIN (CUSIP)

USG6398ADF15…USG6398ADG97

|

||||

| NRW Bank | EUR 1,0bn |

10Y | 3,4% | Very Low |

|

ISIN (CUSIP)

DE000NWB0B24

|

||||

| Province of Ontario | EUR 2,0bn |

10Y | 3,5% | Very Low |

|

ISIN (CUSIP)

XS3440171075

|

||||

| Paragon Bank | GBP 0,50bn |

3Y | FLOAT, +50bp | Very Low |

|

ISIN (CUSIP)

XS3432918335

|

||||

| Prosus | USD 1,6bn |

7–10Y | 5,5–5,9% | Medium |

|

ISIN (CUSIP)

USN7163RBG76…USN7163RBH59

|

||||

| Protective Life Global Funding | USD 0,35bn |

3Y | 4,8% | Very Low |

|

ISIN (CUSIP)

74368ECC2

|

||||

| PSP Capital | GBP 0,60bn |

5Y | 4,5% | Very Low |

|

ISIN (CUSIP)

XS3439216246

|

||||

| Public Storage Operating | USD 0,90bn |

6–10Y | 4,8–5,3% | Low |

|

ISIN (CUSIP)

74464AAG6…74464AAH4

|

||||

| Royal Bank Of Canada | USD 2,3bn |

3–6Y | 4,7–5,0%; FLOAT | Very Low |

|

ISIN (CUSIP)

US78017DAX66

|

||||

| SESI | USD 0,20bn |

PERP | 7,7% | Very High |

|

ISIN (CUSIP)

USU8151EAH90

|

||||

| Sixt | EUR 0,50bn |

4Y | 3,8% | Very High |

|

ISIN (CUSIP)

DE000A46Z700

|

||||

| South West Water Finance | GBP 0,35bn |

9–15Y | 3,8–6,1% | Medium |

|

ISIN (CUSIP)

XS3441669275…XS3433852269

|

||||

| SRC Sukuk | USD 2,8bn |

6–10Y | 5,1–5,5% | Very Low |

|

ISIN (CUSIP)

XS3422176308…XS3422176480

|

||||

| State Of Rhineland Palatinate | EUR 0,50bn |

2Y | 2,8% | Very Low |

|

ISIN (CUSIP)

DE000RLP1692

|

||||

| Sunbelt Rentals Holdings | USD 1,2bn |

4–10Y | 5,1–5,8% | Medium |

|

ISIN (CUSIP)

866966AB0…866966AA2

|

||||

| TenneT | EUR 3,5bn |

4–20Y | 3,3–4,7% | Medium |

|

ISIN (CUSIP)

XS3433863621…XS3433864355

|

||||

| Tesco Corporate Treasury Services | EUR 0,50bn |

8Y | 3,8% | Medium |

|

ISIN (CUSIP)

XS3437614228

|

||||

| Toyota Motor Credit | USD 1,6bn |

3–7Y | 4,5–5,0%; FLOAT | Low |

|

ISIN (CUSIP)

US89236TQD09…US89236TQF56

|

||||

| Trinidad & Tobago | USD 0,80bn |

12Y | 6,3% | High |

|

ISIN (CUSIP)

USP93960AM75

|

||||

| United States Steel | USD 1,2bn |

5Y | 5,2–5,7% | Medium |

|

ISIN (CUSIP)

USU9118RAC17…USU9118RAD99

|

||||

| Vesteda | EUR 0,50bn |

4Y | 3,8% | Low |

|

ISIN (CUSIP)

XS3441750711

|

||||