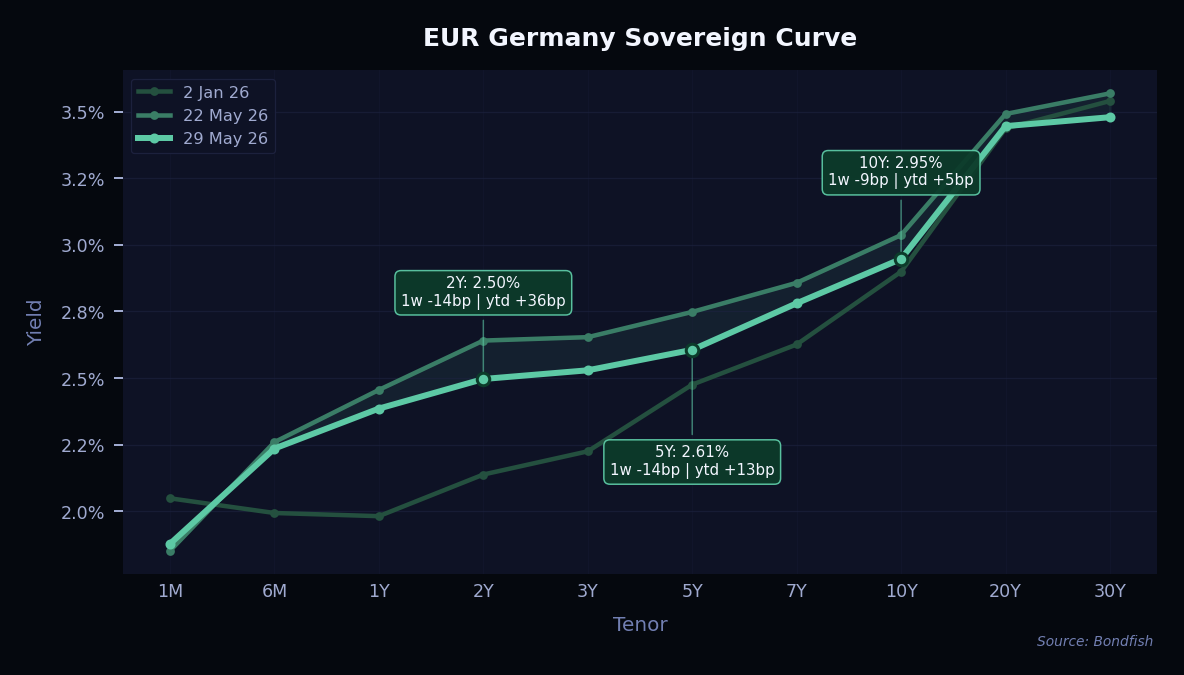

EUR: The main driver was the news about a possible US-Iran deal, which eased the energy-price fears that had pushed yields to recent highs — so yields fell, with most markets dropping about 10–20bp over two weeks. For German Bunds, the middle of the curve fell the most, leaving euro yields back near the low end of their recent range. One thing worth noting: bonds still move quite a bit with oil prices, but their link to natural gas prices has weakened. Overall, the shape of the German Bund curve looks about fair.

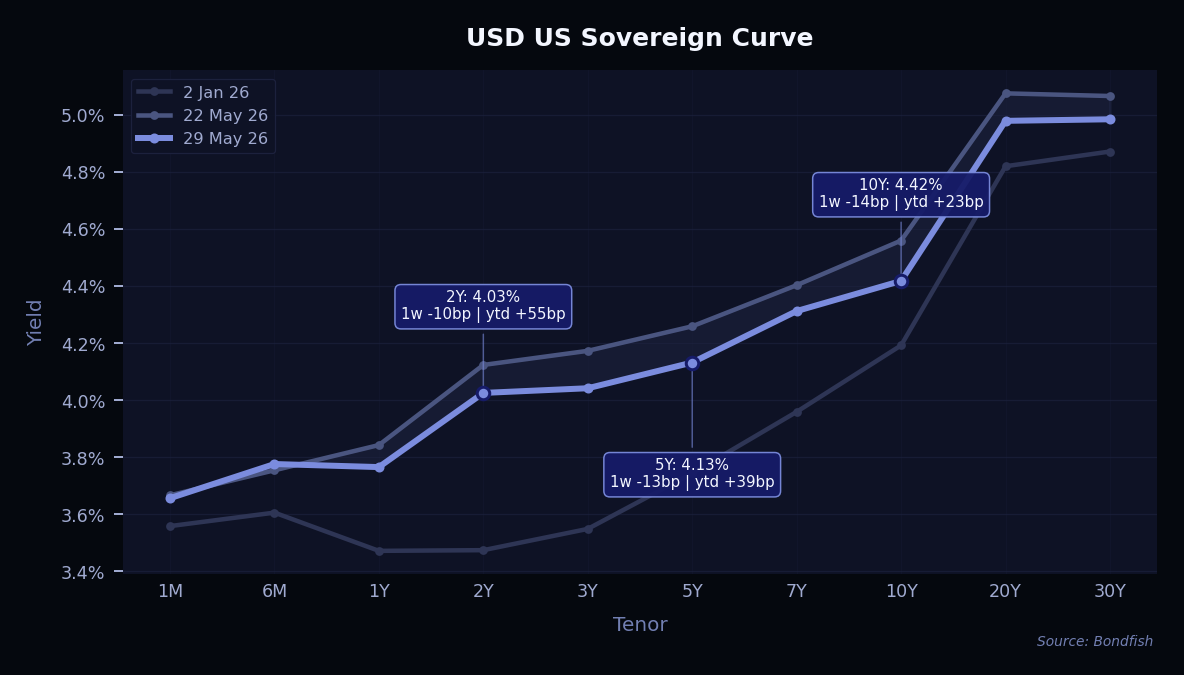

USD: Again, the same reason: hopes of a US-Iran deal calmed the energy-price fears that had lifted yields, so yields fell here too. For US Treasuries, the longer-dated bonds dropped the most while short bonds barely moved. Even after this fall, US yields are still near the top of their recent range and look expensive compared with other big government bond markets, so there probably isn't much more room for them to drop. If anything, the bigger risk from here is the gap between long and short yields getting smaller.

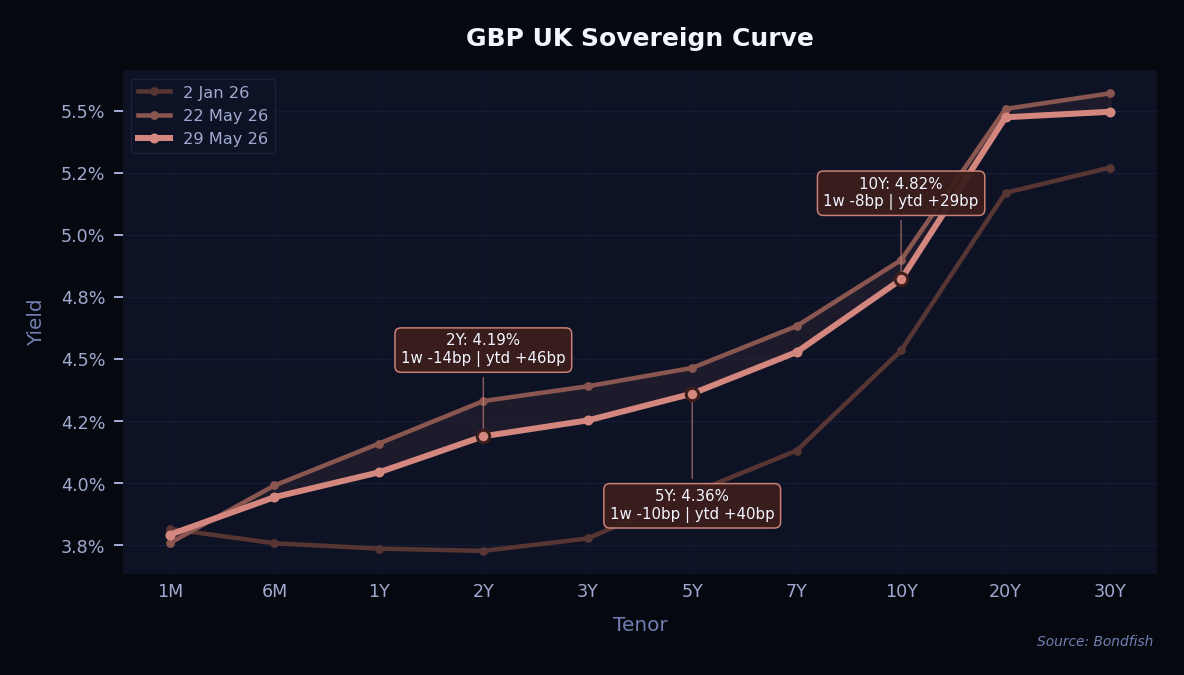

GBP: Same story here: the big reason yields fell was the news about a possible US-Iran deal. That news calmed fears about energy prices, and those fears were what had pushed yields up to their recent highs. So as the worry faded, yields came back down. UK gilts fell the most, helped on top of that by some weaker UK economic data and less political worry after the 7 May local elections. The middle of the curve (around 2–5 years) dropped the most, while very short and very long bonds moved less. After such a strong rally, the simple takeaway is that most of the move has already happened, so it makes sense to be careful and not bet too heavily on yields falling much further.

It was a calm week for credit, so the biggest gains came from company-specific news rather than the market as a whole. The standout was Kohl's 2045 bond, which rallied hard following a better-than-expected earnings update, while Ocado's 2030 bond rose on news of a new partnership with Asda. Long-dated Swiss government paper also jumped as the whole curve repriced lower: with inflation stuck near zero and markets leaning toward a possible return to negative rates, a late-May bill auction cleared at a negative yield (around −0.09%) on very strong demand, and that downshift was magnified in ultra-long, high-duration bonds. Romania's long-dated EUR debt firmed on continued fiscal-consolidation progress, with a sharply narrower budget deficit easing sovereign-downgrade risk. Elsewhere in Europe the moves were more modest, with names like Banque Postale edging higher.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| Kohls 5.55% Jul 2045 | USD | 6,67% | 9,73% | VeryHigh |

|

Reason

Kohl's reported better-than-expected Q1 earnings, with narrower loss and stable outlook.

|

||||

| Bell Tel Co 4.464% Apr 2048 | USD | 5,13% | 5,69% | Medium |

|

Reason

Bell Canada launched a debt tender offer and refinanced with new lower-cost bonds.

|

||||

| Switzerland 0.5% May 2058 | CHF | 4,35% | 0,57% | VeryLow |

|

Reason

Curve-wide repricing on possible SNB return to negative rates; ultra-long duration amplified the move.

|

||||

| Romania 4.625% Apr 2049 | EUR | 2,59% | 6,38% | Medium |

|

Reason

Romania's long-dated EUR bonds firmed over the week on continued fiscal-consolidation progress: January–April budget data (released May 26) showed the deficit narrowing ~57% y/y to 1.17% of GDP, keeping the country on track for its 6.2% full-year target and reinforcing receding sovereign-downgrade risk — the key spread-tightening catalyst for Romanian credit. The gain came despite, not because of, the Friday Galați drone strike, which is a risk-off headline that would normally pressure yields higher. Soft offsets (NBR's end-2026 inflation forecast raised to 5.5%, a weak May retail bond auction, and post-government-dismissal political noise) capped the move, leaving it a modest spread-driven rally rather than a broad repricing.

|

||||

| Banque Postale 2.25% Oct 2028 | EUR | 2,56% | 3,10% | Medium |

|

Reason

No clear positive issuer catalyst.

|

||||

| Vmed UK 4.5% Jul 2031 | GBP | 1,43% | 8,16% | High |

|

Reason

No clear positive issuer catalyst.

|

||||

| Gatwick Funding 3.25% Feb 2048 | GBP | 1,40% | 6,54% | Medium |

|

Reason

No clear positive issuer catalyst.

|

||||

| Ocado Group 11% Jun 2030 | GBP | 1,34% | 8,92% | VeryHigh |

|

Reason

Ocado signed a partnership with Asda to power its UK online grocery platform from 2027.

|

||||

On the losing side, the moves were small and mostly tied to single names, in keeping with the week's quiet tone. Whirlpool's 2030 bond fell after Fitch cut its rating to BB- and the company suspended its dividend. Transocean slipped on antitrust concerns over its proposed Valaris takeover. Bausch Health also weakened, while European names such as SIG and Eramet saw only mild losses. With overall spreads barely moving, none of the declines were dramatic.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| Bausch Health 7.25% May 2029 | USD | -1,23% | 19,98% | VeryHigh |

|

Reason

No clear negative issuer catalyst.

|

||||

| Transocean Intl 6.8% Mar 2038 | USD | -1,11% | 7,30% | VeryHigh |

|

Reason

Transocean's $5.8bn acquisition of Valaris raised antitrust concerns and leverage worries.

|

||||

| Whirlpool 6.125% Jun 2030 | USD | -1,11% | 7,82% | High |

|

Reason

Multiple rating agencies downgraded Whirlpool; company also suspended its dividend.

|

||||

| Eramet 6.5% Nov 2029 | EUR | -0,95% | 7,09% | VeryHigh |

|

Reason

No clear negative catalyst — the €500m capital increase (approved 27 May) is credit-supportive deleveraging, so the modest dip looks like a pullback after recent gains rather than a fresh negative, against a backdrop of ongoing operational and management challenges.

|

||||

| Thames Wtr Super 9.75% Oct 2027 | GBP | -0,49% | 2,34% | VeryHigh |

|

Reason

No clear negative issuer catalyst.

|

||||

| Kinepolis 2.75% Dec 2026 | EUR | -0,47% | 3,99% | VeryHigh |

|

Reason

No clear negative issuer catalyst.

|

||||

| Vanquis Banking 8.875% Jan 2032 | GBP | -0,37% | 5,26% | VeryHigh |

|

Reason

Vanquis launched a tender for existing bonds and issued new debt, creating supply pressure.

|

||||

| Aviva 6.125% Nov 2036 | GBP | -0,17% | 5,39% | Medium |

|

Reason

Aviva launched a tender offer and issued new bonds, creating near-term supply pressure.

|

||||

The headline downgrade of the week was Baffinland Iron Mines slipping into default at D from S&P, while NTT lost its single-A status, cut to BBB+ by S&P, and Telesat Canada was pushed deeper into distress at CC. On the upgrade side, India led the way: Moody's lifted Reliance Industries to Baa1 and Tata Steel to Baa2. Uber Technologies pushed further into investment grade at BBB+ from S&P, while Fitch raised YPF to B-, nudging the Argentine energy group up out of the triple-C area.

Note: only long-term senior unsecured ratings were taken into account.

| Issuer | Agency | Change |

| Aena SME | Moody's | A2 → A1 |

| Allwyn | S&P | BB (new) |

| Anglogold Ashanti | S&P | BB+ → BBB- |

| ASM International | S&P | BB+ → BBB- |

| Assemblin Caverion | Fitch | B → B+ |

| Baffinland Iron Mines | S&P | CCC- → D |

| C&S Group Enterprises | S&P | B → B- |

| C&S Wholesale Grocers | S&P | B → B- |

| Centrient | S&P | B → B- |

| Century Aluminum | S&P | B- → B |

| Cleco Power | Fitch | BBB → BBB+ |

| Conair | S&P | CCC+ → SD |

| Emerald Technologies US Acquisitionco | S&P | D → CCC |

| Enstall | S&P | D → CCC+ |

| Gulfside Supply | S&P | B → B- |

| Hanwha General Insurance | S&P | A → A+ |

| Hanwha Life Insurance | S&P | A → A+ |

| Infosys | Moody's | Baa1 → A2 |

| Ingenovis Health | S&P | CC → SD |

| InterCement Participacoes | Fitch | B- (new) |

| Interpipe | S&P | CCC → CCC+ |

| Kioxia | Fitch | BB+ → BBB- |

| McKesson Medical-Surgical Top | S&P | BB (new) |

| Medical Solutions Parent | S&P | CCC+ → CCC- |

| Myrrha SAS | S&P | B- → CCC+ |

| NTT | S&P | A- → BBB+ |

| Optiv | S&P | D → CCC+ |

| Oscar Acquisitionco | S&P | SD → CCC |

| Puma Energy Holdings Pte | Fitch | BB → BB+ |

| Reliance Industries | Moody's | Baa2 → Baa1 |

| REN - Redes Energeticas Nacionais SGPS | Moody's | Baa2 → Baa1 |

| Snap | S&P | B+ → BB- |

| Transgaz | Fitch | BBB- → BBB |

| Tata Consultancy Services | Moody's | Baa1 → A2 |

| Tata Steel | Moody's | Baa3 → Baa2 |

| Telesat Canada | S&P | CCC- → CC |

| Uber Technologies | S&P | BBB → BBB+ |

| Unipol Assicurazioni | Moody's | Baa2 → Baa1 |

| Viavi Solutions | Fitch | BB- → BB |

| Whirlpool | Fitch | BB → BB- |

| YPF | Fitch | CCC+ → B- |

Primary markets stayed busy despite month-end holidays. Governments led the way: Spain raised €13bn in a single 10-year deal, with Portugal, Austria, and Finland also pricing long-dated sovereign bonds. In investment-grade corporates, SAP was the standout with a four-part €3.5bn euro transaction, joined by RELX, AXA, and SCOR. Banks were active too — Goldman Sachs raised around $6.5bn across several dollar tranches, and several Canadian banks tapped the market. US high yield reopened modestly with deals from PBF, Avis, and Worthington Steel.

The pipeline ahead looks significantly heavier. Paramount's ~$50bn financing package for its Warner Bros. merger is one of the year's largest credit tests, while a surge of AI data-centre borrowing — including a $36bn deal linked to Anthropic — adds to already record supply levels. Around $35bn of US investment-grade and €35bn+ of European issuance are expected in the coming week alone.

| Issuer | Size | Term | Yield | Risk Level |

| Abanca | EUR 0,50bn |

8Y | 3,9% | Low |

|

ISIN (CUSIP)

ES0265936080

|

||||

| AEP Transmission Company | USD 0,65bn |

10Y | 5,3% | Low |

|

ISIN (CUSIP)

US00115AAT60

|

||||

| Agence Francaise De Developpement Epic | USD 2,0bn |

3Y | 4,4% | Low |

|

ISIN (CUSIP)

FR0014018VR6

|

||||

| Assicurazioni Generali Spa | EUR 0,75bn |

11Y | 4,4% | Medium |

|

ISIN (CUSIP)

XS3388195441

|

||||

| Austria, Republic Of | EUR 5,5bn |

5–15Y | 2,9–3,6% | Very Low |

|

ISIN (CUSIP)

AT0000A3V200…AT0000A3V234

|

||||

| Avis Budget Car Rental | USD 0,30bn |

7Y | 7,8% | Very High |

|

ISIN (CUSIP)

USU05375AV93

|

||||

| AXA | EUR 0,75bn |

30Y | 4,4% | Low |

|

ISIN (CUSIP)

XS3393830651

|

||||

| Banco De Credito Social Cooperativo | EUR 0,50bn |

6Y | 3,9% | Medium |

|

ISIN (CUSIP)

XS3396961289

|

||||

| Banco Santander | USD 1,5bn |

PERP | 7,2% | High |

|

ISIN (CUSIP)

US05971KAY55

|

||||

| Bank Of Georgia | USD 0,30bn |

5Y | 6,6% | High |

|

ISIN (CUSIP)

XS3391767103

|

||||

| Bank Of Montreal | EUR 2,0bn |

3–7Y | 2,9–3,2% | Very Low |

|

ISIN (CUSIP)

XS3397036123…XS3397036396

|

||||

| Bank Polska Kasa Opieki | EUR 0,75bn |

4Y | 3,7% | Very High |

|

ISIN (CUSIP)

XS3394773538

|

||||

| Bankinter | EUR 0,75bn |

8Y | 3,8% | Very High |

|

ISIN (CUSIP)

ES0213679OV1

|

||||

| BBVA Mexico | USD 1,0bn |

5Y | 5,4% | Medium |

|

ISIN (CUSIP)

USP2000GAB97

|

||||

| Bell Canada | USD 0,65bn |

10Y | 5,5% | Medium |

|

ISIN (CUSIP)

US0778FPAS85

|

||||

| BKS Bank | EUR 0,25bn |

5Y | 4,1% | Very High |

|

ISIN (CUSIP)

AT0000A3USG1

|

||||

| BNG Bank | EUR 1,2bn |

7Y | 3,1% | Very Low |

|

ISIN (CUSIP)

XS3395922506

|

||||

| Bocom Leasing Management Hong Kong | USD 0,75bn |

3Y | FLOAT, +48bp | Low |

|

ISIN (CUSIP)

XS3392169754

|

||||

| Borr Ihc | USD 1,1bn |

6Y | 9,0% | Very High |

|

ISIN (CUSIP)

USG1467FAH67

|

||||

| BPCE | USD 2,8bn |

6–11Y | 5,2–5,8% | Low |

|

ISIN (CUSIP)

USF11494CR43…USF11494CS26

|

||||

| BT Finance | EUR 0,85bn |

8Y | 3,9% | Medium |

|

ISIN (CUSIP)

XS3392699396

|

||||

| Carrefour | EUR 0,75bn |

8Y | 4,0% | Very High |

|

ISIN (CUSIP)

FR0014018Q93

|

||||

| Cassa Depositi E Prestiti Spa | EUR 0,75bn |

5Y | 3,3% | Medium |

|

ISIN (CUSIP)

IT0005713042

|

||||

| Co-Operative Group | GBP 0,35bn |

6Y | 8,2% | Very High |

|

ISIN (CUSIP)

XS3392868256

|

||||

| Commerzbank | EUR 0,75bn |

7Y | 3,8% | Medium |

|

ISIN (CUSIP)

DE000CZ46CR1

|

||||

| Credito Emiliano Spa | EUR 0,50bn |

6Y | 3,6% | Medium |

|

ISIN (CUSIP)

XS3395932489

|

||||

| DNB Bank Asa | GBP 0,60bn |

6Y | 5,1% | Very Low |

|

ISIN (CUSIP)

XS3400932599

|

||||

| Element Fleet Management | USD 0,50bn |

3Y | 4,8% | Medium |

|

ISIN (CUSIP)

USC3318LAH45

|

||||

| European Stability Mechanism | EUR 2,0bn |

5Y | 2,9% | Very Low |

|

ISIN (CUSIP)

EU000A1Z99Z8

|

||||

| Bosnia and Herzegovina | EUR 0,80bn |

5Y | 5,2% | Very High |

|

ISIN (CUSIP)

XS3385959302

|

||||

| Finland, Republic Of | USD 1,5bn |

10Y | 55,9% | Very Low |

|

ISIN (CUSIP)

XS3396019336

|

||||

| Florida Power & Light | USD 1,6bn |

30–40Y | 5,8–5,9% | Very Low |

|

ISIN (CUSIP)

US341081HD24…US341081HE07

|

||||

| Gecina | EUR 0,50bn |

5Y | 3,5% | Low |

|

ISIN (CUSIP)

FR0014018W12

|

||||

| Hana Securities | USD 0,30bn |

5Y | 5,0% | Very High |

|

ISIN (CUSIP)

XS3344489755

|

||||

| Hera Spa | EUR 0,50bn |

6Y | 3,6% | Medium |

|

ISIN (CUSIP)

XS3350935774

|

||||

| Ithaca Energy | EUR 0,15bn |

PERP | 5,5% | Very High |

|

ISIN (CUSIP)

XS3186903756

|

||||

| Iutecredit Finance Sarl | EUR 0,14bn |

5Y | 12,0% | Very High |

|

ISIN (CUSIP)

XS3047514446

|

||||

| Kommunalbanken Norway | USD 1,5bn |

5Y | 4,2% | Very Low |

|

ISIN (CUSIP)

XS3395953998

|

||||

| La Banque Postale | EUR 0,65bn |

8Y | 4,0% | Medium |

|

ISIN (CUSIP)

FR0014018T74

|

||||

| Licheng International Development | USD 0,15bn |

3Y | 4,8% | Very High |

|

ISIN (CUSIP)

XS3393614873

|

||||

| Madrid, Community Of | EUR 0,50bn |

5Y | 3,0% | Low |

|

ISIN (CUSIP)

ES00001010T9

|

||||

| National Australia Bank | USD 3,0bn |

3–11Y, PERP | 4,4–5,6%; FLOAT | Very Low |

|

ISIN (CUSIP)

US632525CT68…USQ6535DCS10

|

||||

| National Bank Of Canada | USD 1,0bn |

6Y | 4,9% | Very Low |

|

ISIN (CUSIP)

63307A3Q6

|

||||

| Natwest Group | GBP 0,50bn |

PERP | 7,5% | Medium |

|

ISIN (CUSIP)

XS3394864766

|

||||

| Navient | USD 0,50bn |

5Y | 9,4% | High |

|

ISIN (CUSIP)

US63938CAR97

|

||||

| Nederlandse Waterschapsbank | EUR 1,0bn |

7Y | 3,1% | Very Low |

|

ISIN (CUSIP)

XS3398041338

|

||||

| Neo Next+ Energy | USD 0,75bn |

5Y | 6,6% | Very High |

|

ISIN (CUSIP)

NO0013754648

|

||||

| New York Life Global Funding | USD 0,70bn |

10Y | 5,2% | Very Low |

|

ISIN (CUSIP)

64952XFS5

|

||||

| NGPL Pipeco | USD 0,72bn |

10Y | 5,6% | Medium |

|

ISIN (CUSIP)

U6536EAG1

|

||||

| Nokia Oyj | EUR 0,50bn |

6Y | 3,7% | Medium |

|

ISIN (CUSIP)

XS3397145767

|

||||

| Northwestern Mutual Global Funding | USD 0,70bn |

5Y | 4,7% | Very Low |

|

ISIN (CUSIP)

66815M3B1

|

||||

| Nutrien | USD 1,0bn |

5–10Y | 4,9–5,4% | Medium |

|

ISIN (CUSIP)

US67077MBG24…US67077MBH07

|

||||

| Oman Arab Bank Saog | USD 0,40bn |

PERP | 6,8% | Medium |

|

ISIN (CUSIP)

XS3303713310

|

||||

| Ontario, Province Of | USD 3,0bn |

10Y | 4,9% | Very Low |

|

ISIN (CUSIP)

US683234D471

|

||||

| OTP Bank | EUR 0,50bn |

7Y | 3,4% | Low |

|

ISIN (CUSIP)

XS3392853902

|

||||

| PBF Holding Company | USD 0,50bn |

8Y | 7,2% | High |

|

ISIN (CUSIP)

USU70453AJ15

|

||||

| Polardc | EUR 0,80bn |

4Y | FLOAT, +600bp | Very High |

|

ISIN (CUSIP)

NO0013752949

|

||||

| Portugal, Republic Of | EUR 3,0bn |

20Y | 3,9% | Low |

|

ISIN (CUSIP)

PTOTEEOE0019

|

||||

| Principal Financial Group | USD 0,40bn |

11Y | 5,3% | Medium |

|

ISIN (CUSIP)

US74251VAW28

|

||||

| Quebec, Province Of | USD 3,0bn |

10Y | 4,7% | Very Low |

|

ISIN (CUSIP)

US748148SJ30

|

||||

| Regions Bank | USD 1,0bn |

3Y | 4,8% | Medium |

|

ISIN (CUSIP)

US759187JX65

|

||||

| Relx Finance Bv | EUR 1,5bn |

3–8Y | 3,3–3,9% | Low |

|

ISIN (CUSIP)

XS3317606419…XS3317607060

|

||||

| SAP | EUR 3,5bn |

2–7Y | 3,1–3,5%; FLOAT, +33bp | Low |

|

ISIN (CUSIP)

XS3393867810…XS3393869782

|

||||

| Scor | EUR 0,50bn |

30Y | 4,5% | Low |

|

ISIN (CUSIP)

FR0014018PB2

|

||||

| Skandinaviska Enskilda Banken Ab | USD 0,60bn |

PERP | 6,8% | Medium |

|

ISIN (CUSIP)

XS3394042322

|

||||

| Smith & Nephew | EUR 0,50bn |

12Y | 4,3% | Medium |

|

ISIN (CUSIP)

XS3384821834

|

||||

| Spain, Kingdom Of | EUR 13,0bn |

10Y | 3,4% | Low |

|

ISIN (CUSIP)

ES0000012S22

|

||||

| Standard Chartered | USD 1,0bn |

PERP | 7,0% | Medium |

|

ISIN (CUSIP)

USG84228HJ04

|

||||

| Stellantis Financial Services Us | USD 2,5bn |

3–5Y | 5,4–5,8% | Medium |

|

ISIN (CUSIP)

USU8586FAD07…USU8586FAE89

|

||||

| Suedzucker International Finance Bv | EUR 0,40bn |

5Y | 4,5% | Medium |

|

ISIN (CUSIP)

XS3393874436

|

||||

| Swedbank Hypotek Ab | EUR 1,0bn |

7Y | 3,1% | Very Low |

|

ISIN (CUSIP)

XS3400528116

|

||||

| Sydbank A/S | EUR 0,50bn |

5Y | 3,7% | Low |

|

ISIN (CUSIP)

XS3391818963

|

||||

| Triodos Bank | EUR 0,25bn |

11Y | 5,6% | High |

|

ISIN (CUSIP)

XS3386634391

|

||||

| UBS | EUR 1,2bn |

6Y | 3,4% | Very Low |

|

ISIN (CUSIP)

XS3393866259

|

||||

| UBS | USD 1,5bn |

4Y | 4,7% | Very Low |

|

ISIN (CUSIP)

US90261AAJ16

|

||||

| UBS Switzerland | EUR 0,75bn |

3Y | 3,3% | Very Low |

|

ISIN (CUSIP)

CH1331113469

|

||||

| Valeo | EUR 0,60bn |

7Y | 5,0% | High |

|

ISIN (CUSIP)

FR0014018J35

|

||||

| Veralto | USD 0,72bn |

6Y | 4,8% | Medium |

|

ISIN (CUSIP)

US92338CAP86

|

||||

| Volkswagen Financial Services | GBP 0,35bn |

3Y | 5,2% | Medium |

|

ISIN (CUSIP)

XS3398382674

|

||||

| Worthington Steel | USD 0,70bn |

7Y | 7,8% | High |

|

ISIN (CUSIP)

USU46013AA33

|

||||

| Yiwu State Owned Capital Operation | USD 0,35bn |

3Y | 4,3% | Very High |

|

ISIN (CUSIP)

XS3376923549

|

||||

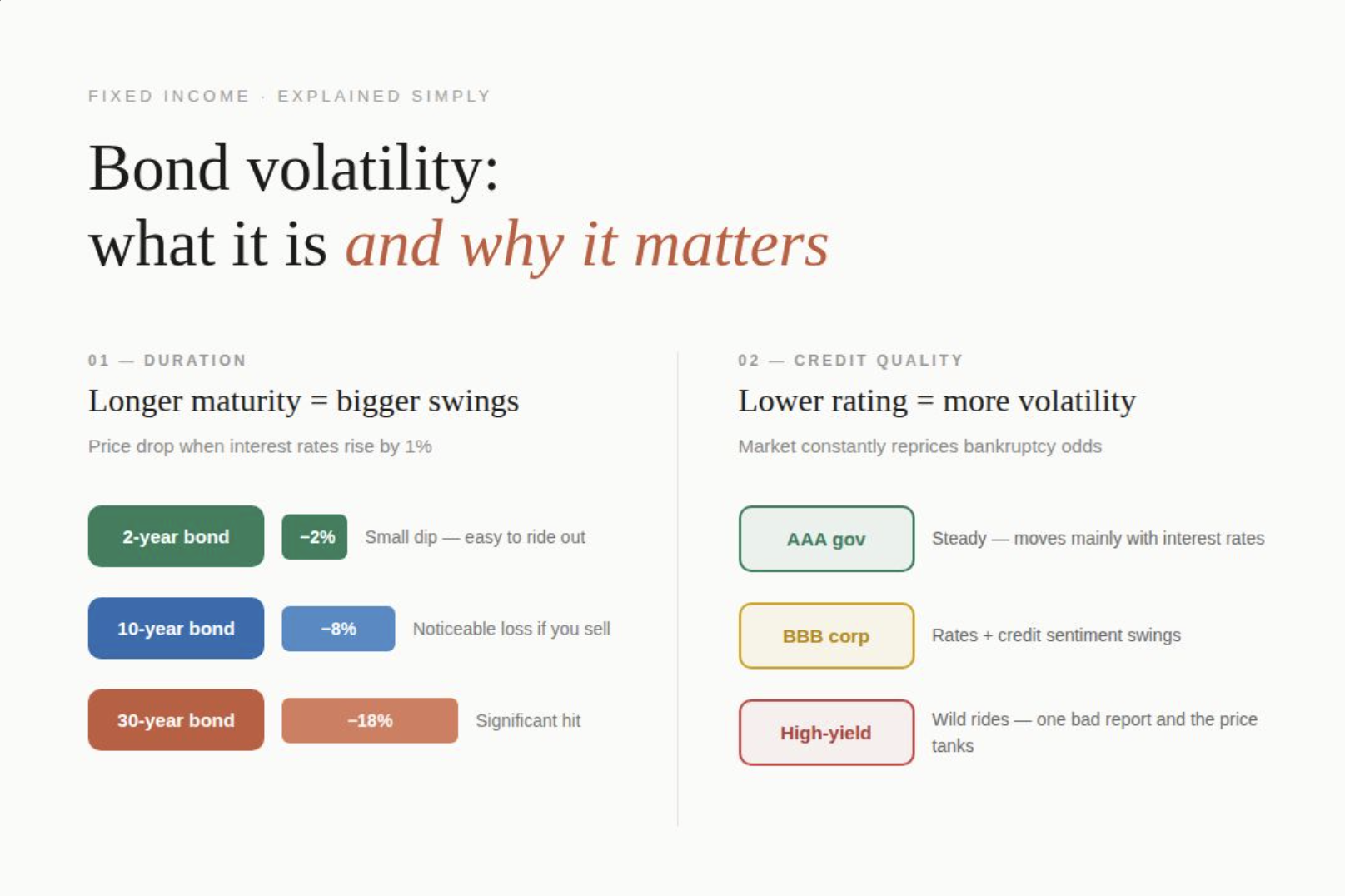

A common question in investment circles is why bond volatility should matter at all if the principal is returned in full at maturity. Two factors drive it. The first is duration: the longer the maturity, the more a bond's price moves when rates change — a 30-year bond swings far more than a 2-year. The second is credit quality: lower-rated issuers are more volatile, as the market continually reprices the odds of default, and a single weak earnings report or downgrade can shift sentiment quickly. The catch is that holding to maturity is not guaranteed. Liquidity needs can force an early sale at whatever price the secondary market offers. So the decision to buy a bond should rest on more than yield — it should also weigh how likely an early exit might be, and how far the price could move against the holder if one becomes necessary.