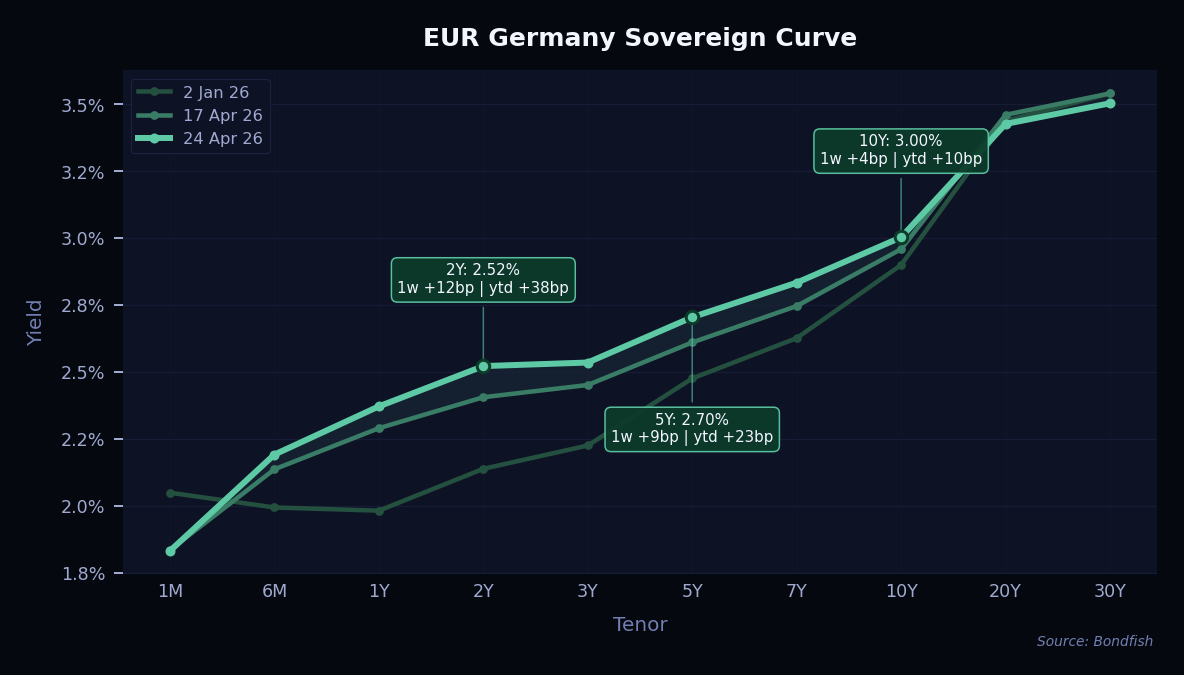

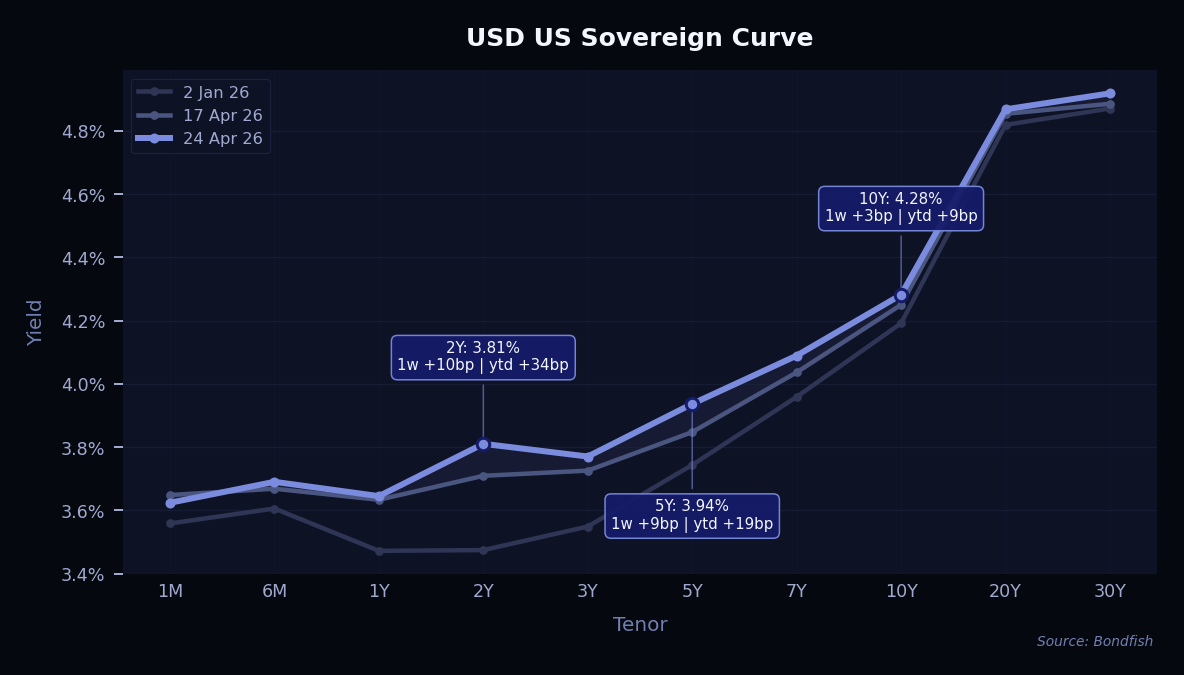

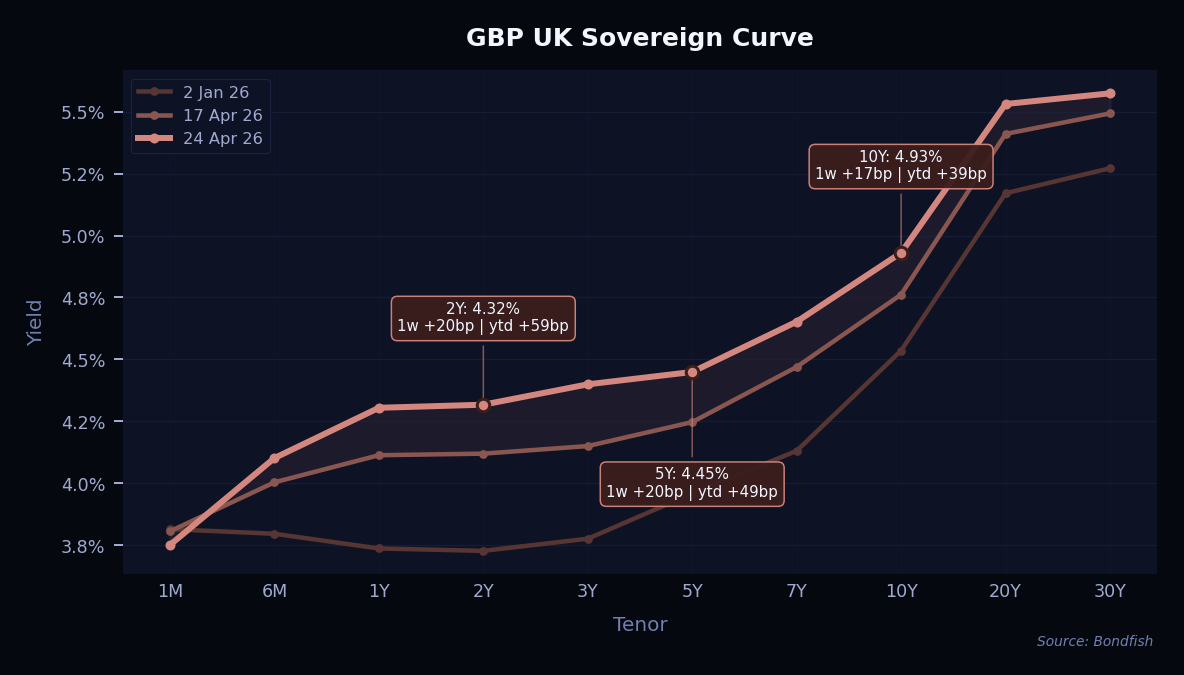

Developed market yield curves moved higher during the week as investors reacted to renewed pressure from energy prices and persistent uncertainty around the Middle East conflict. The market treated the ceasefire extension more as a fragile pause than a clear path to resolution, keeping inflation risks in focus. European and UK rates were especially sensitive to higher natural gas prices, while UK yields also faced additional pressure from stronger inflation, labour market and business activity data. Central banks are still expected to stay on hold in the near term, but markets moved closer to pricing a longer period of restrictive policy. In this environment, shorter-duration bonds may remain more resilient, while longer-dated bonds could stay volatile until energy and geopolitical risks become clearer.

Credit markets were mixed but broadly resilient this week. Investment-grade spreads moved slightly tighter as lower volatility and strong earnings helped investor sentiment. However, higher government bond yields limited total returns, especially for longer-duration bonds. The front end of the credit curve also lagged, partly because demand was softer and recent issuance was heavy in bank bonds. Overall, investors still showed interest in high-quality credit, but the market looked more selective. With spreads already close to recent tight levels, further gains may depend on stable rates, solid earnings and no renewed escalation in energy or geopolitical risks.

Below are the bonds with the strongest weekly price appreciation.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| TopBuild 3.625% Mar 2029 | USD | 3,20% | 3,66% | High |

|

Reason

QXO acquisition at 23% premium eliminates refinancing risk; $17bn deal closing Q3 2026 with committed debt financing secured.

|

||||

| Eramet 6.5% Nov 2029 | EUR | 2,24% | 7,46% | VeryHigh |

|

Reason

Mine halt mitigates cash burn from Indonesian production quota cuts; potential sovereign wealth fund stake purchase provides capital relief.

|

||||

| Odeon Finco 7.5% Feb 2029 | USD | 2,15% | 14,67% | VeryHigh |

|

Reason

Refinancing $425m debt at lower rates; redemption of 12.75% notes reduces annual interest burden and extends maturity profile.

|

||||

| iHeartCommns 10.875% May 2030 | USD | 2,11% | 18,25% | VeryHigh |

|

Reason

Preliminary merger talks with Sirius XM combine largest radio owner with largest satellite radio service; scale synergies expected.

|

||||

| Armor Holdco 8.5% Nov 2029 | USD | 2,06% | 8,89% | VeryHigh |

|

Reason

No clear positive issuer catalyst

|

||||

| Intrum Investmen 8.5% Sep 2030 | EUR | 1,64% | 12,33% | VeryHigh |

|

Reason

No clear positive issuer catalyst

|

||||

| Future PLC 6.75% Jul 2030 | GBP | 1,48% | 9,24% | High |

|

Reason

No clear positive issuer catalyst

|

||||

| Eramet 7% May 2028 | EUR | 1,47% | 6,97% | VeryHigh |

|

Reason

Mine halt mitigates cash burn from Indonesian production quota cuts; potential sovereign wealth fund stake purchase provides capital relief.

|

||||

| Iceland Bondco 4.375% May 2028 | GBP | 0,59% | 5,33% | VeryHigh |

|

Reason

Evoke acquisition by Bally's Intralot eliminates standalone company risk; deal provides liquidity event and creditor protection through acquirer.

|

||||

The following bonds experienced the sharpest weekly declines.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| FMC 6.375% May 2053 | USD | -5,55% | 8,97% | High |

|

Reason

Analyst downgrade citing mounting fundamental stress; restructuring actions slow to drive earnings and cash flow recovery.

|

||||

| FMC 4.5% Oct 2049 | USD | -4,76% | 8,41% | High |

|

Reason

Analyst downgrade citing mounting fundamental stress; restructuring actions slow to drive earnings and cash flow recovery.

|

||||

| ASGN 4.625% May 2028 | USD | -3,81% | 7,54% | High |

|

Reason

Q1 EPS missed by 30%; weak Q2 guidance suggests AI demand impact on software implementation work margins.

|

||||

| Whirlpool 4.5% Jun 2046 | USD | -3,71% | 7,80% | High |

|

Reason

Q1 appliance shipments down high-single digits; soft discretionary demand and 6.5% mortgage rates pressure North American market.

|

||||

| Whirlpool 4.6% May 2050 | USD | -3,69% | 7,64% | High |

|

Reason

Q1 appliance shipments down high-single digits; soft discretionary demand and 6.5% mortgage rates pressure North American market.

|

||||

| Argentina 3.875% Jul 2035 | EUR | -3,33% | 9,74% | VeryHigh |

|

Reason

Modest spread repricing

|

||||

| COMMUNITY HEALTH SYSTEMS 9.75% Jan 2034 | USD | -3,22% | 9,09% | VeryHigh |

|

Reason

Q1 adjusted loss of $0.48 significantly missed estimates; weak healthcare labor markets pressure operator margins and patient volume.

|

||||

| Mobico Group 4.875% Sep 2031 | EUR | -2,91% | 10,02% | VeryHigh |

|

Reason

No clear negative issuer catalyst

|

||||

| Avis Budget Car 8.375% Jun 2032 | USD | -2,72% | 7,74% | VeryHigh |

|

Reason

Stock collapsed 70% with no clear catalyst after 600% surge; valuation deemed unsustainable by analysts; short squeeze unwound.

|

||||

Note: only long-term senior unsecured ratings were taken into account.

| Issuer | Agency | Change |

| AEGEA Saneamento e Participacoes | S&P | B+ → B |

| Air Baltic | S&P | B- → CCC+ |

| API Holdings III | S&P | CCC+ → CCC |

| Arxis | Fitch | B+ → BB |

| BCPE Ulysses Intermediate | Fitch | B → B- |

| BRB Banco de Brasilia | Fitch | CCC → CC |

| British Columbia Hydro & Power Authority | Fitch | AA+ → AA- |

| CECONOMY | S&P | BB- → BB |

| City of Katowice | Fitch | BBB+ → A- |

| Dairy Farmers of America | S&P | BBB → BBB+ |

| Heritage Grocers | S&P | B- → CCC+ |

| Japan Tobacco | S&P | A+ → A |

| Kaman | Fitch | B+ → BB |

| Kimberly-Clark de Mexico SAB de CV | Fitch | A → A- |

| Lakeland | S&P | CCC+ (new) |

| LBM Acquisition | Fitch | B → B- |

| Liberty Interactive | Fitch | CCC+ → D |

| Life Time | Fitch | BB- → BB |

| Lithuania | Fitch | A → A+ |

| MoneyGram International | Fitch | B → B- |

| Mountain Province Diamonds | S&P | CCC → CCC- |

| NOVA Chemicals | S&P | BB- → BBB- |

| Oesterreichische Aerzte-und Apothekerbank AG/Wien | Fitch | BBB+ → BBB |

| Pacific Gas and Electric | S&P | BB → BB+ |

| Peak Jersey Holdco | S&P | CCC → B- |

| PG&E | S&P | BB → BB+ |

| Qnnect | Fitch | B+ → BB |

| Quantic Corporate | Fitch | B+ → BB |

| Quantic Electronics | Fitch | B+ → BB |

| QVC | Fitch | CCC+ → D |

| Recycle & Resource Operations Pty | S&P | CCC → CCC- |

| Reno de Medici | Fitch | RD → CC |

| Republic of Mozambique | Fitch | CCCu → CCu |

| Sanders Industries | Fitch | B+ → BB |

| SiriusPoint | S&P | BBB → BBB+ |

| Smiths | S&P | BBB+ → BBB |

| StoneX | S&P | BB- → BB |

| Therapy Brands | S&P | CCC+ → CCC- |

| VB Verbund-Beteiligung eG | Fitch | BBB+ → BBB |

New issuance remained active but more selective this week. In the US investment-grade market, supply slowed to around $18bn after a much heavier previous week, but April issuance still reached about $114–115bn, making it the busiest April since 2020. Large deals continued to find strong demand, with AT&T raising $6bn and Blackstone’s BCRED placing $850mn of bonds with solid order books. Europe is also expected to stay active, with €25–40bn of issuance expected next week. Still, investors are becoming more selective. Higher-quality issuers continue to access the market smoothly, while riskier borrowers and private-credit-linked names face more scrutiny amid concerns about software loans, refinancing risk and weaker recoveries.

| Issuer | Size | Term | Yield | Risk Level |

| Abertis Infraestructuras Finance Bv | EUR 0,50bn |

PERP | 4,8% | High |

|

ISIN (CUSIP)

XS3315415243

|

||||

| Aircastle | USD 0,65bn |

5Y | 5,1% | Medium |

|

ISIN (CUSIP)

USG01340AD38

|

||||

| Alliander | EUR 1,0bn |

5–10Y | 3,3–3,8% | Low |

|

ISIN (CUSIP)

XS3359749481…XS3359749564

|

||||

| Amprion Gmbh | EUR 1,0bn |

30Y | 4,4–4,9% | Medium |

|

ISIN (CUSIP)

DE000A46ZYH0…DE000A46ZYJ6

|

||||

| Argan | EUR 0,50bn |

4Y | 3,8% | Very High |

|

ISIN (CUSIP)

FR0014017JX1

|

||||

| At&T | USD 6,0bn |

7–41Y | 4,9–6,3% | Medium |

|

ISIN (CUSIP)

US00206RNG38…US00206RNQ10

|

||||

| Banca Sella Holding Spa | EUR 0,30bn |

5Y | 3,7% | Very High |

|

ISIN (CUSIP)

IT0005707085

|

||||

| Banco Santander | EUR 0,50bn |

5Y | 3,0% | Very Low |

|

ISIN (CUSIP)

ES04139000F6

|

||||

| Banco Santander | GBP 0,75bn |

7Y | 5,6% | Low |

|

ISIN (CUSIP)

XS3359635391

|

||||

| Blackstone Private Credit Fund | USD 0,85bn |

5Y | 6,2% | Medium |

|

ISIN (CUSIP)

09261HCC9

|

||||

| Bng Bank | USD 1,5bn |

5Y | 4,0% | Very Low |

|

ISIN (CUSIP)

XS3358362278

|

||||

| Caisse Des Depots Et Consignations | EUR 1,0bn |

5Y | 3,1% | Very Low |

|

ISIN (CUSIP)

FR00140183Y5

|

||||

| Commonwealth Bank Of Australia | USD 1,8bn |

3Y | 4,0% | Very Low |

|

ISIN (CUSIP)

USQ2704MAP34

|

||||

| Core Scientific Finance I | USD 3,3bn |

5Y | 7,9% | Very High |

|

ISIN (CUSIP)

USU2062LAA99

|

||||

| Crc Insurance Group | USD 0,20bn |

PERP | 7,0% | Very High |

|

ISIN (CUSIP)

USU69869AA06

|

||||

| Danaher | EUR 3,0bn |

2–12Y | 3,3–4,0%; FLOAT, +38bp | Low |

|

ISIN (CUSIP)

XS3352082930…XS3352084803

|

||||

| Dangote Fertilizer | USD 0,75bn |

5Y | 7,8% | Very High |

|

ISIN (CUSIP)

USV2754PAA22

|

||||

| Deutsche Telekom | EUR 1,5bn |

7–12Y | 3,4–4,0% | Medium |

|

ISIN (CUSIP)

XS3356130073…XS3356130826

|

||||

| Edged Compute | USD 1,3bn |

5Y | 7,5% | High |

|

ISIN (CUSIP)

USU2781AAA35

|

||||

| Enquest | USD 0,68bn |

5Y | 10,1% | Very High |

|

ISIN (CUSIP)

USG315APAM05

|

||||

| European Investment Bank | EUR 4,0bn |

3Y | 2,7% | Very Low |

|

ISIN (CUSIP)

EU000A4ETUZ1

|

||||

| Gb Ait Buyer | USD 0,50bn |

8Y | 8,8% | Very High |

|

ISIN (CUSIP)

USU3702PAA40

|

||||

| Gohl Capital | USD 1,2bn |

PERP | 7,6–8,3% | Medium |

|

ISIN (CUSIP)

XS3357500472…XS3357513533

|

||||

| Goodman Australia Finance Pty | EUR 0,60bn |

7Y | 3,9% | Medium |

|

ISIN (CUSIP)

XS3356038003

|

||||

| Goodman Us Finance Seven | USD 0,60bn |

10Y | 5,3% | Medium |

|

ISIN (CUSIP)

USU3826PAA58

|

||||

| Grand City Properties Finance Sarl | EUR 0,60bn |

PERP | 5,8% | Very High |

|

ISIN (CUSIP)

XS3362208079

|

||||

| Highmark | USD 0,40bn |

10Y | 5,8% | Medium |

|

ISIN (CUSIP)

USU4323TAC90

|

||||

| Informa | EUR 0,50bn |

6Y | 3,9% | Medium |

|

ISIN (CUSIP)

XS3324619231

|

||||

| International Finance Facility For Immunisation | USD 1,0bn |

5Y | 4,1% | Very Low |

|

ISIN (CUSIP)

XS3358317132

|

||||

| Jerrold Finco | GBP 0,30bn |

6Y | 8,5% | High |

|

ISIN (CUSIP)

XS3309691999

|

||||

| Jyske Bank A/S | EUR 0,50bn |

6Y | 3,7% | Very High |

|

ISIN (CUSIP)

XS3358396763

|

||||

| Kapla Holding Sas | EUR 0,80bn |

6–7Y | 5,1%; FLOAT, +300bp | Very High |

|

ISIN (CUSIP)

XS3356048812

|

||||

| Kaspi.Kz Ao | USD 0,60bn |

5Y | 5,9% | Medium |

|

ISIN (CUSIP)

XS3310367738

|

||||

| Korea Ocean Business | USD 0,30bn |

3Y | FLOAT, +65bp | Very Low |

|

ISIN (CUSIP)

XS3342075796

|

||||

| Landeskreditbank Baden Wuerttemberg Foerderbank | GBP 0,50bn |

3Y | FLOAT, +100bp | Very Low |

|

ISIN (CUSIP)

XS3358409681

|

||||

| Landeskreditbank Baden Wuerttemberg Foerderbank | USD 0,75bn |

4Y | FLOAT, +100bp | Very Low |

|

ISIN (CUSIP)

XS3358410184…XS3358410184

|

||||

| Liberty Mutual Group | USD 0,75bn |

10Y | 5,3% | Medium |

|

ISIN (CUSIP)

USU52932BT37

|

||||

| Lottomatica Group Spa | EUR 0,77bn |

6Y | 4,6% | High |

|

ISIN (CUSIP)

XS3318840223

|

||||

| Mineral Resources | USD 1,3bn |

6–8Y | 6,0–6,2% | High |

|

ISIN (CUSIP)

USQ60976AF65…USQ60976AG49

|

||||

| Nk Kazakhstan Temir Zholy Ao | USD 1,0bn |

5–10Y | 5,0–5,4% | Medium |

|

ISIN (CUSIP)

XS3353982112…XS3353982385

|

||||

| Nordea Bank Abp | EUR 1,0bn |

5Y | 3,3% | Very Low |

|

ISIN (CUSIP)

XS3357292930

|

||||

| Oesterreichische Kontrollbank | EUR 1,0bn |

5Y | 2,9% | Very Low |

|

ISIN (CUSIP)

XS3358410697

|

||||

| Omers Finance | USD 1,0bn |

5Y | 4,1% | Very Low |

|

ISIN (CUSIP)

US68218UAB44

|

||||

| Pearson Funding | GBP 0,35bn |

10Y | 6,3% | Medium |

|

ISIN (CUSIP)

XS3357258758

|

||||

| Prologis | USD 1,2bn |

5–10Y | 4,4–5,0% | Low |

|

ISIN (CUSIP)

US74340XCU37…US74340XCV10

|

||||

| Rede D'Or Finance Sarl | USD 0,50bn |

10Y | 6,5% | High |

|

ISIN (CUSIP)

USL7915TAE21

|

||||

| Rentokil Terminix Funding | USD 0,50bn |

5Y | 4,8% | Medium |

|

ISIN (CUSIP)

USG7500HAA35

|

||||

| Riverstone International Holdings | USD 0,15bn |

10Y | 7,1% | Very High |

|

ISIN (CUSIP)

XS3334205112

|

||||

| Sanofi | EUR 2,3bn |

3–11Y | 3,0–3,8% | Very Low |

|

ISIN (CUSIP)

FR0014016SU0…FR0014016SX4

|

||||

| Schleswig-Holstein, State Of | EUR 1,0bn |

10Y | 3,2% | Very Low |

|

ISIN (CUSIP)

DE000SHFM1J8

|

||||

| Shuifa International Holdings Bvi | USD 0,20bn |

3Y | 4,5% | Medium |

|

ISIN (CUSIP)

XS3340536104

|

||||

| State Street | USD 1,5bn |

6–11Y | 4,6–5,1% | Very Low |

|

ISIN (CUSIP)

US857477DF72…US857477DG55

|

||||

| Svenska Handelsbanken Ab | EUR 1,0bn |

7Y | 3,6% | Very Low |

|

ISIN (CUSIP)

XS3358268251

|

||||

| Tdc Brands (Nuuday A/S) | EUR 0,55bn |

5Y | 8,0% | Very High |

|

ISIN (CUSIP)

XS3358347634

|

||||

| Terumo | USD 0,50bn |

5Y | 4,5% | Very High |

|

ISIN (CUSIP)

XS3327684414

|

||||

| Tokyo, Metropolitan Of | USD 1,0bn |

5Y | 4,2% | Very High |

|

ISIN (CUSIP)

XS3327917962

|

||||

| Truist Financial | USD 2,0bn |

6–11Y | 4,7–5,3% | Medium |

|

ISIN (CUSIP)

US89788MAX02…US89788MAY84

|

||||

| Turkiye Ihracat Kredi Bankasi As | USD 0,65bn |

3Y | 6,2% | High |

|

ISIN (CUSIP)

XS3357256208

|

||||

| Var Energi Asa | EUR 0,75bn |

60Y | 5,1% | High |

|

ISIN (CUSIP)

XS3304274189

|

||||

| Vistajet Malta Finance | USD 0,53bn |

6Y | 8,9% | Very High |

|

ISIN (CUSIP)

USX9816MAB64

|

||||

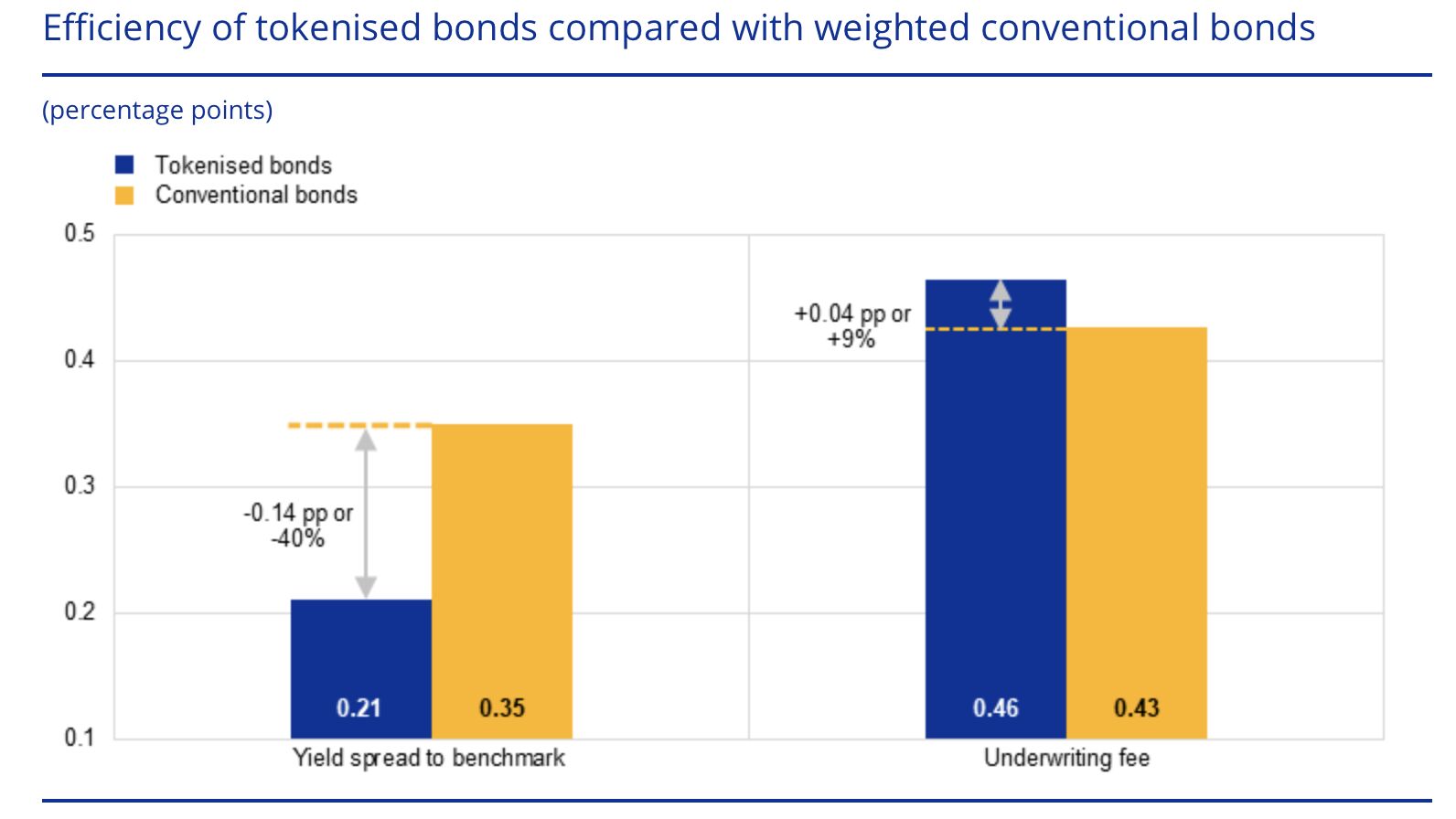

A recent European Central Bank study on tokenised bonds suggests that, although the market remains very small with fewer than 200 issues since 2018, the early evidence is already encouraging: tokenised bonds appear to trade with better liquidity and tighter yield spreads than comparable conventional bonds from the same issuer. One notable surprise is that underwriting fees were still slightly higher, even though tokenisation should in principle reduce intermediation costs over time. It is still early, but these are promising signs for a traditionally illiquid and infrastructure-heavy bond market that clearly needs better accessibility and efficiency. Source: ECB Macroprudential Bulletin, “Tokenisation in finance: a focus on bond markets”.