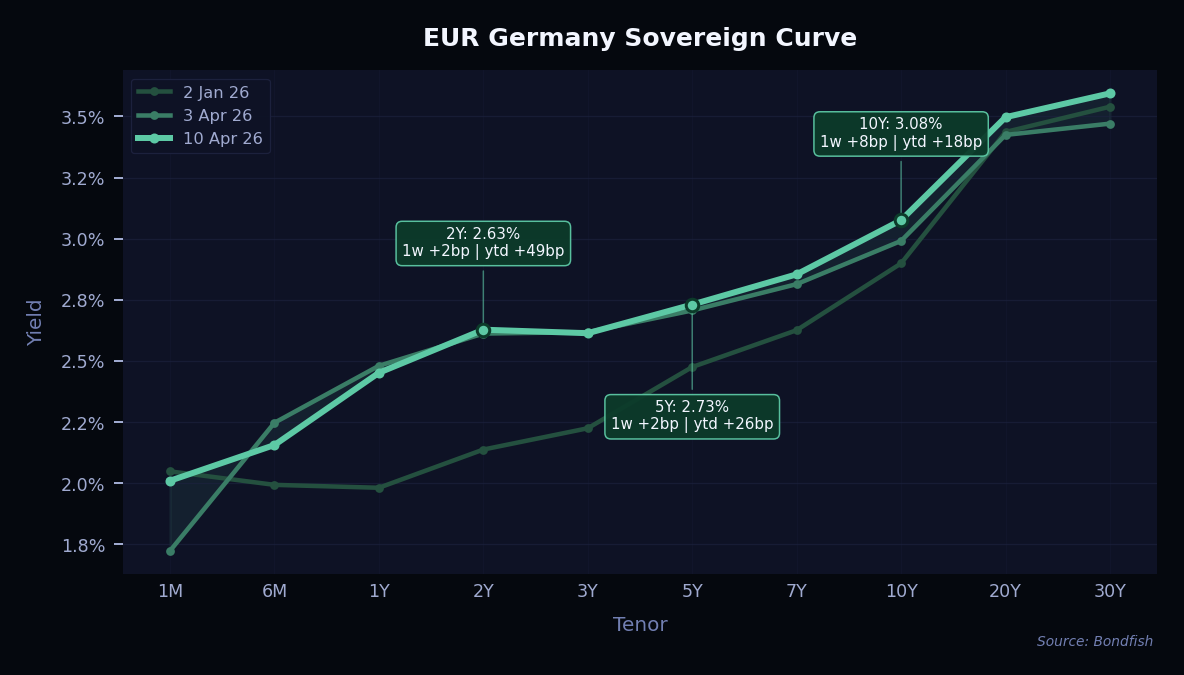

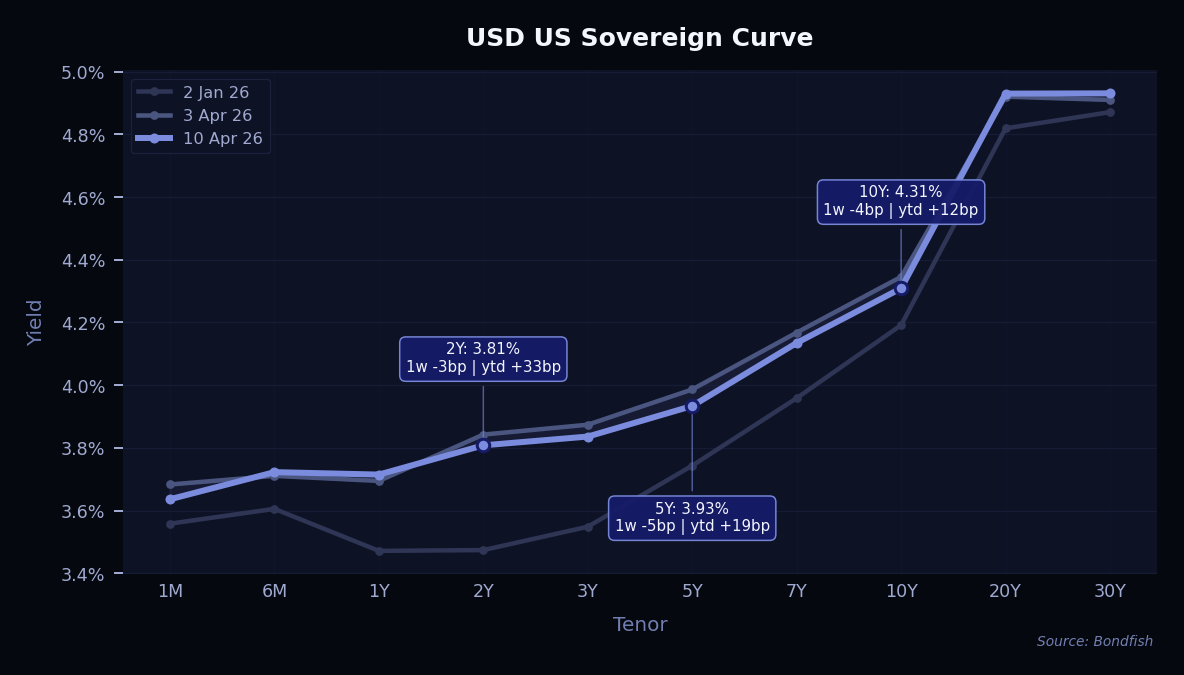

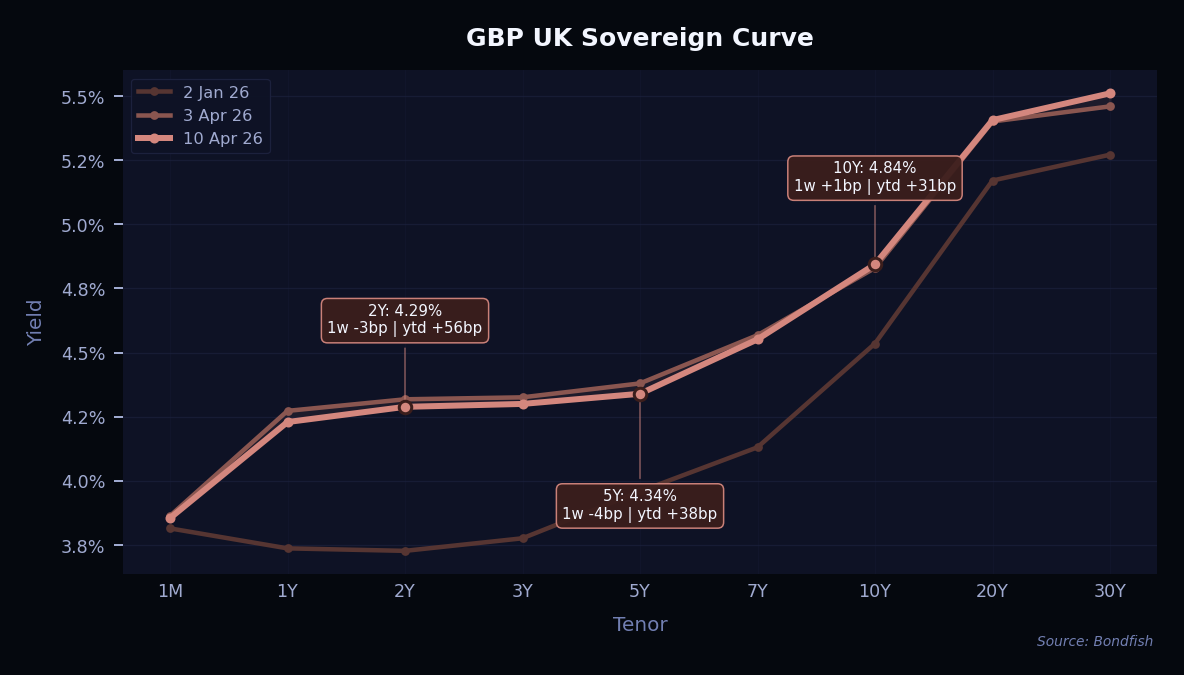

Developed market yield curves moved in different directions this week as investors balanced some relief from the Middle East ceasefire against the risk that energy prices, especially gas in Europe, may stay elevated for longer. The main message from the market was that the shock has eased, but not disappeared. US yields were helped by this partial relief, while the UK market stayed more mixed. In Europe, the move was firmer at the long end, as investors remained cautious that sticky energy prices could keep inflation pressure alive and limit room for rate cuts. Overall, the tone suggests that markets are no longer pricing a full stress scenario, but they are also not ready to fully reverse the earlier repricing while geopolitical and energy uncertainty remains high. For allocation, we remain cautious on duration for now, with a preference for shorter maturities in Europe, while long-dated bonds are becoming more interesting for long-term investors as yields stay elevated.

Credit markets recovered this week as ceasefire headlines supported risk sentiment and helped spreads tighten, especially in Europe. The rebound was also helped by cash that had stayed on the sidelines and moved back into the market after the initial shock. In the US, the move was more measured, with credit supported by still-high yields and expectations that earnings and company fundamentals remain solid. At the same time, the tone stayed cautious. Investors are still watching energy prices, shipping disruption and the risk that the recent rally may have already priced in too much good news.

Below are the bonds with the strongest weekly price appreciation.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| iHeartCommns 10.875% May 2030 | USD | 11,16% | 21,99% | VeryHigh |

|

Reason

Management changes and content expansion supported sentiment.

|

||||

| Kohls 5.125% May 2031 | USD | 6,12% | 9,89% | VeryHigh |

|

Reason

Tariff refund upside.

|

||||

| PacifiCorp 7.375% Sep 2055 | USD | 4,71% | 7,12% | Medium |

|

Reason

PacifiCorp appeal win reduced wildfire liability concerns.

|

||||

| Paramount Global 6.875% Apr 2036 | USD | 4,43% | 7,63% | High |

|

Reason

Paramount reduced its debt commitments for the Warner Bros.

|

||||

| PacifiCorp 7.125% Aug 2056 | USD | 4,15% | 7,17% | Medium |

|

Reason

PacifiCorp appeal win reduced wildfire liability concerns.

|

||||

| FMC 6.375% May 2053 | USD | 3,99% | 8,32% | High |

|

Reason

EU herbicide approval improved growth outlook.

|

||||

| Discovery Com 6.35% Jun 2040 | USD | 3,86% | 8,77% | High |

|

Reason

Merger financing progress and shareholder support.

|

||||

| Heimstaden 7.361% Jan 2031 | EUR | 2,39% | 7,11% | VeryHigh |

|

Reason

Asset sale supported deleveraging expectations.

|

||||

| Samhallsbyggnads 1.125% Sep 2029 | EUR | 2,15% | 7,61% | VeryHigh |

|

Reason

Bond buyback may have supported prices.

|

||||

| Eramet 6.5% Nov 2029 | EUR | 2,11% | 8,51% | VeryHigh |

|

Reason

The Duval family has appointed Lazard to explore options for their holding, including a potential sale.

|

||||

The following bonds experienced the sharpest weekly declines.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| Baxter Intl 4.5% Jun 2043 | USD | -3,31% | 6,87% | Medium |

|

Reason

High duration and modest spread repricing.

|

||||

| Germany 1.25% Aug 2048 | EUR | -3,21% | 3,56% | VeryLow |

|

Reason

High duration; long end of the curve repricing.

|

||||

| Spain 3.45% Jul 2066 | EUR | -2,65% | 4,20% | Low |

|

Reason

High duration; long end of the curve repricing.

|

||||

| Germany 1.8% Aug 2053 | EUR | -2,25% | 3,55% | VeryLow |

|

Reason

High duration; long end of the curve repricing.

|

||||

| Germany 1.8% Aug 2053 | EUR | -2,23% | 3,57% | VeryLow |

|

Reason

High duration; long end of the curve repricing.

|

||||

| Germany 2.9% Aug 2056 | EUR | -2,18% | 3,58% | VeryLow |

|

Reason

High duration; long end of the curve repricing.

|

||||

| Germany 2.5% Aug 2054 | EUR | -2,09% | 3,57% | VeryLow |

|

Reason

High duration; long end of the curve repricing.

|

||||

| Netherlands 3.5% Jan 2056 | EUR | -2,07% | 3,62% | VeryLow |

|

Reason

High duration; long end of the curve repricing.

|

||||

| Netherlands 2% Jan 2054 | EUR | -2,00% | 3,60% | VeryLow |

|

Reason

High duration; long end of the curve repricing.

|

||||

| Intuit 5.5% Sep 2053 | USD | -1,97% | 6,15% | Low |

|

Reason

High duration and modest spread repricing.

|

||||

Note: only long-term senior unsecured ratings were taken into account.

| Issuer | Agency | Change |

| Air Baltic | Fitch | CCC+ → CCC- |

| Altyn-Bank | Fitch | BBB → BBB+ |

| Amprion | Moody's | Baa1 → Baa2 |

| Aruba | S&P | BBB+ → A- |

| Australian Unity Healthcare Property Trust | Moody's | Baa1 → Baa3 |

| Banco Davivienda | S&P | BB → BB- |

| Banco de Bogota | S&P | BB → BB- |

| Bancolombia | S&P | BB → BB- |

| Bancolombia Panama | S&P | BB → BB- |

| Banistmo | S&P | BB → BB- |

| BCPE Empire | S&P | B- → B |

| British Columbia Investment Management | S&P | AAA → AA+ |

| Cantor Fitzgerald | Moody's | Baa3 (new) |

| City of Astana Kazakhstan | Fitch | BBB (new) |

| CNH Industrial | S&P | BBB+ → BBB |

| CNH Industrial Capital | S&P | BBB+ → BBB |

| CNH Industrial Capital Australia Pty | S&P | BBB+ → BBB |

| Colombia Titulos De Tesoreria | S&P | BB → BB- |

| Colombia Treasury Bill | S&P | BB → BB- |

| Colombian TES | S&P | BB → BB- |

| CoolSys | S&P | SD → CCC+ |

| Cornerstone Building Brands | S&P | B- → CCC+ |

| CPI Property | S&P | BB+ → BB |

| Crocs | Moody's | B2 → Ba3 |

| Diversified Healthcare Trust | Moody's | Caa1 → B3 |

| Ecopetrol | S&P | BB → BB- |

| Element Solutions | S&P | BB → BB+ |

| Enel Americas | S&P | BBB- → BB+ |

| Enel Colombia SA ESP | S&P | BBB- → BB+ |

| Financiera de Desarrollo Nacional | S&P | BB → BB- |

| Financiera de Desarrollo Territorial SA Findeter | S&P | BB → BB- |

| Franshion Brilliant | Moody's | Ba2 → Ba3 |

| FS KKR Capital | Fitch | BBB- → BB+ |

| Greenko Power II | Moody's | Ba2 → Ba3 |

| Greenko Wind Projects Mauritius | Moody's | Ba2 → Ba3 |

| Grupo Cibest | S&P | BB- → B+ |

| Grupo de Inversiones Suramericana | S&P | BB → BB- |

| Hess Midstream Operations | Fitch | BB+ → BBB- |

| IAMGOLD | Moody's | B3 → B2 |

| Isagen SA ESP | S&P | BB → BB- |

| Kazakhstan Electricity Grid Operating | S&P | BB+ → BBB- |

| Louisiana-Pacific | Fitch | BBB (new) |

| Manitowoc | S&P | B → B+ |

| Oleoducto Central | S&P | BB → BB- |

| OQ Chemicals Holding Drei | S&P | B- → CCC+ |

| Oxea | S&P | B- → CCC+ |

| OXEA International | S&P | B- → CCC+ |

| PVH | S&P | BBB- → BBB |

| Republic of Colombia | S&P | BB → BB- |

| Termocandelaria Power | S&P | BB → BB- |

| United PF | S&P | CCC+ → CCC- |

| University of British Columbia | S&P | A+ → A |

| Viridien | S&P | B- → B |

| Vue Entertainment International | S&P | CCC+ → B- |

| WestJet Airlines | Fitch | B → B- |

Primary markets reopened quickly after ceasefire headlines improved sentiment. Issuers used the calmer backdrop to come to market, with strong activity in both the US and Europe, and the pipeline for next week also looks busy, especially in high-grade and bank issuance. Demand remains strongest for large, high-quality borrowers, including AI-linked names, where investors still seem comfortable funding heavy capex plans. At the same time, the market is not fully open for everyone. Outside the strongest credits, issuers still need the right window and pricing discipline, as geopolitical risk and energy uncertainty continue to keep investors selective.

| Issuer | Size | Term | Yield | Risk Level |

| Abn Amro Bank | EUR 1,5bn |

5Y | 3,0% | Very Low |

|

ISIN (CUSIP)

XS3344463792

|

||||

| Banco Santander | USD 2,6bn |

3–5Y | 4,6–4,9%; FLOAT | Low |

|

ISIN (CUSIP)

US05971KAX72…US05971KAV17

|

||||

| Banco Santander Totta | EUR 0,75bn |

7Y | 3,2% | Very Low |

|

ISIN (CUSIP)

PTBSPKOM0022

|

||||

| Bank Of Montreal | GBP 1,0bn |

3Y | FLOAT, +50bp | Very Low |

|

ISIN (CUSIP)

XS3344408268

|

||||

| Banque Developpt Conseil Europe 9 | EUR 1,0bn |

7Y | 3,0% | Very Low |

|

ISIN (CUSIP)

XS3344655512

|

||||

| Belfius Banque | EUR 0,75bn |

6Y | 4,0% | Low |

|

ISIN (CUSIP)

BE0390305747

|

||||

| Binzhou Guotou Overseas Investment | USD 0,10bn |

3Y | 6,0% | Very High |

|

ISIN (CUSIP)

XS3339013669

|

||||

| Cencosud | USD 0,50bn |

10Y | 5,9% | Medium |

|

ISIN (CUSIP)

USP2205JAX83

|

||||

| Chobani | USD 0,80bn |

8Y | 6,4% | Very High |

|

ISIN (CUSIP)

USU1703HAD99

|

||||

| Clariane | EUR 0,50bn |

5Y | 6,9% | Very High |

|

ISIN (CUSIP)

XS3314100986

|

||||

| Commerzbank | EUR 2,0bn |

3–7Y | 2,9–3,5% | Very Low |

|

ISIN (CUSIP)

DE000CZ46CE9…DE000CZ46CC3

|

||||

| Congo, Democratic Republic Of | USD 1,2bn |

5–10Y | 8,8–9,5% | Very High |

|

ISIN (CUSIP)

XS3344646875…XS3344646958

|

||||

| Coreweave | USD 1,8bn |

6Y | 9,8% | Very High |

|

ISIN (CUSIP)

USU2069EAC40

|

||||

| Coventry Building Society (Cvb_P.L) | EUR 0,75bn |

5Y | 3,1% | Very Low |

|

ISIN (CUSIP)

XS3330164271

|

||||

| Credit Mutuel Home Loan Sfh | EUR 1,2bn |

7Y | 3,2% | Very Low |

|

ISIN (CUSIP)

FR0014017W96

|

||||

| Deutsche Bank | USD 1,0bn |

6Y | 5,1% | Medium |

|

ISIN (CUSIP)

25160PAS6

|

||||

| Dnb Boligkreditt As | USD 0,75bn |

5Y | 4,2% | Very Low |

|

ISIN (CUSIP)

XS3338901781

|

||||

| Dz Hyp | EUR 1,0bn |

5Y | 3,2% | Very Low |

|

ISIN (CUSIP)

DE000A4DFKS4

|

||||

| Efg International Finance (Luxembourg) S.A R.L. | EUR 0,50bn |

5Y | 3,9% | Low |

|

ISIN (CUSIP)

CH1548688279

|

||||

| Engie | EUR 1,0bn |

PERP | 4,4% | Medium |

|

ISIN (CUSIP)

FR0014016Z94

|

||||

| Engie | GBP 0,40bn |

PERP | 6,1% | Medium |

|

ISIN (CUSIP)

FR0014016ZB5

|

||||

| Erac Usa Finance | USD 3,0bn |

4–10Y | 4,5–5,3% | Low |

|

ISIN (CUSIP)

U29490BD7…U29490BC9

|

||||

| Eurazeo | EUR 0,50bn |

5Y | 4,7% | Medium |

|

ISIN (CUSIP)

FR0014017VR8

|

||||

| Eurofima European Company For The Financing Of Railroad Rolling Stock | EUR 0,50bn |

20Y | 3,8% | Very Low |

|

ISIN (CUSIP)

XS3337381399

|

||||

| Expedia Group | USD 1,0bn |

10Y | 5,6% | Medium |

|

ISIN (CUSIP)

30212PBM6

|

||||

| Finland, Republic Of | EUR 4,0bn |

10Y | 3,4% | Very Low |

|

ISIN (CUSIP)

FI4000602891

|

||||

| General Mills | EUR 1,7bn |

30Y | 4,9–5,4% | Medium |

|

ISIN (CUSIP)

XS3328596179…XS3328596336

|

||||

| Hochtief | EUR 0,90bn |

5–8Y | 3,8–4,1% | Very High |

|

ISIN (CUSIP)

DE000A2YN2V0…DE000A46ZW17

|

||||

| Italgas Spa | EUR 0,75bn |

6Y | 3,6% | Medium |

|

ISIN (CUSIP)

IT0005704207

|

||||

| Jbs | USD 0,50bn |

11–31Y | 5,6–6,4% | Medium |

|

ISIN (CUSIP)

USL56608AV11…USL56608AW93

|

||||

| Keb Hana Bank | EUR 0,60bn |

5Y | 3,2% | Very Low |

|

ISIN (CUSIP)

XS3343246644

|

||||

| KfW | EUR 5,0bn |

5Y | 2,9% | Very Low |

|

ISIN (CUSIP)

XS3344416287

|

||||

| Kommunalkredit Austria | EUR 0,50bn |

6Y | 3,3% | Very High |

|

ISIN (CUSIP)

AT0000A3TYA4

|

||||

| Landeskreditbank Baden Wuerttemberg Foerderbank | GBP 0,10bn |

5Y | 4,2% | Very Low |

|

ISIN (CUSIP)

XS3324593097

|

||||

| Lloyds Banking Group | GBP 0,50bn |

10Y | 5,7% | Medium |

|

ISIN (CUSIP)

XS3317581752

|

||||

| Marvell Technology | USD 1,0bn |

10Y | 5,3% | Medium |

|

ISIN (CUSIP)

573874

|

||||

| Mauritius Commercial Bank | USD 0,40bn |

5Y | 6,2% | Medium |

|

ISIN (CUSIP)

XS3326338566

|

||||

| Metropolitan Life Global Funding I | USD 1,1bn |

2Y | 4,3%; FLOAT | Very Low |

|

ISIN (CUSIP)

USU5922DEU29

|

||||

| Mizuho Bank | USD 7,5bn |

3–20Y | 4,4–5,8%; FLOAT | Low |

|

ISIN (CUSIP)

USJ45992RL07…USJ45992RQ93

|

||||

| Nederlandse Financierings-Maatschappij Voor Ontwlkkelingslanden N.V. (Fmo) | GBP 0,25bn |

2Y | FLOAT, +28bp | Very Low |

|

ISIN (CUSIP)

XS3343290204

|

||||

| Ontario, Province Of | USD 3,0bn |

5Y | 4,1% | Very Low |

|

ISIN (CUSIP)

US683234EW41

|

||||

| Poland, Republic Of | USD 6,0bn |

5–30Y | 4,6–6,2% | Low |

|

ISIN (CUSIP)

US857524AJ17…US857524AL62

|

||||

| Protective Life Global Funding | USD 0,60bn |

5Y | 4,8% | Very Low |

|

ISIN (CUSIP)

US74368ECB48

|

||||

| Qts Fayetteville I Dc1-2 | USD 4,6bn |

10Y | 5,7% | Medium |

|

ISIN (CUSIP)

U7471TAA6

|

||||

| Societe Generale | EUR 1,2bn |

8Y | 4,0% | Medium |

|

ISIN (CUSIP)

FR0014017V71

|

||||

| Societe Nationale Sncf | EUR 0,50bn |

10Y | 3,9% | Low |

|

ISIN (CUSIP)

FR0014017XI3

|

||||

| Softbank | EUR 1,2bn |

6–10Y | 3,9–4,5% | Medium |

|

ISIN (CUSIP)

XS3317460619…XS3317460700

|

||||

| Sparebanken Norge Boligkreditt | EUR 1,0bn |

5Y | 3,0% | Very Low |

|

ISIN (CUSIP)

XS3343433085

|

||||

| Stora Enso Oyj | EUR 1,0bn |

PERP | 5,6–6,0% | High |

|

ISIN (CUSIP)

XS3306627780…XS3306632517

|

||||

| Unedic | EUR 3,0bn |

6Y | 3,3% | Very Low |

|

ISIN (CUSIP)

FR0014017VS6

|

||||

| Unicredit Spa | EUR 1,0bn |

6Y | 3,8% | Medium |

|

ISIN (CUSIP)

IT0005704900

|

||||

| Univision Communications | USD 1,5bn |

7Y | 8,9% | Very High |

|

ISIN (CUSIP)

USU91505AZ76

|

||||

| Verbund | EUR 0,70bn |

7Y | 3,5% | Low |

|

ISIN (CUSIP)

XS3339795786

|

||||

| Vistra Operations Company | USD 4,0bn |

3–10Y | 4,6–5,6% | Medium |

|

ISIN (CUSIP)

USU9226VBD83…USU9226VBC01

|

||||

| Vonovia | EUR 1,0bn |

2Y | FLOAT, +60bp | Medium |

|

ISIN (CUSIP)

XS3344378339

|

||||

| Vseobecna Uverova Banka As | EUR 0,75bn |

4Y | 3,3% | Very Low |

|

ISIN (CUSIP)

SK4000029237

|

||||

The chart below shows the historically inverse relationship between long-term interest rates and European listed real estate. Using the EPRA ex-UK index as a proxy for continental European real estate, it illustrates how rising sovereign yields tend to put pressure on property valuations by increasing financing costs and pushing required yields higher. This dynamic was particularly visible during the 2022 ECB tightening cycle, when European listed real estate sold off sharply as rates moved higher. The relationship remains important because changes in long-term yields continue to be a key driver of sentiment and valuation across the real estate sector.