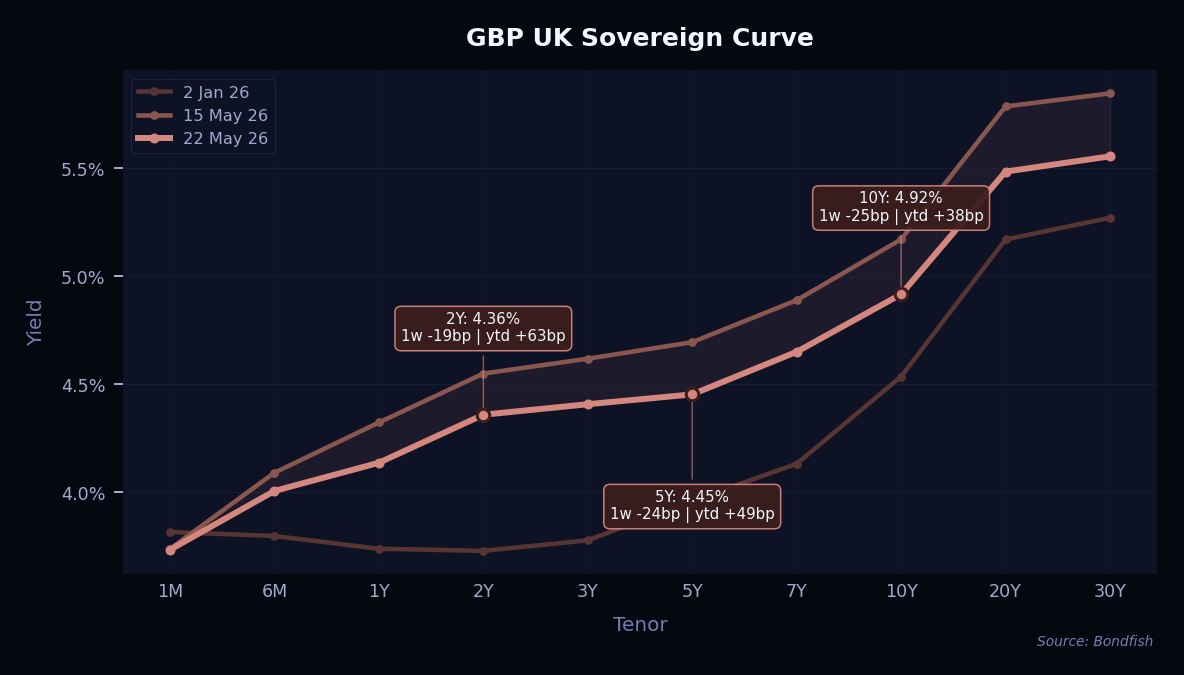

UK gilts staged a sharp rally this week as softer-than-expected April inflation and labour market data prompted markets to scale back near-term hike expectations from the Bank of England. The 2-year yield dropped 22bp to 4.33% while the 10-year fell 7bp to 4.90%, with markets now seeing a June hike as essentially off the table — only around 4bp is priced in. Investor reassurance came from comments by potential Labour leadership contender Andy Burnham, who signalled support for the existing fiscal rules, helping retrace much of the post-election weakness.

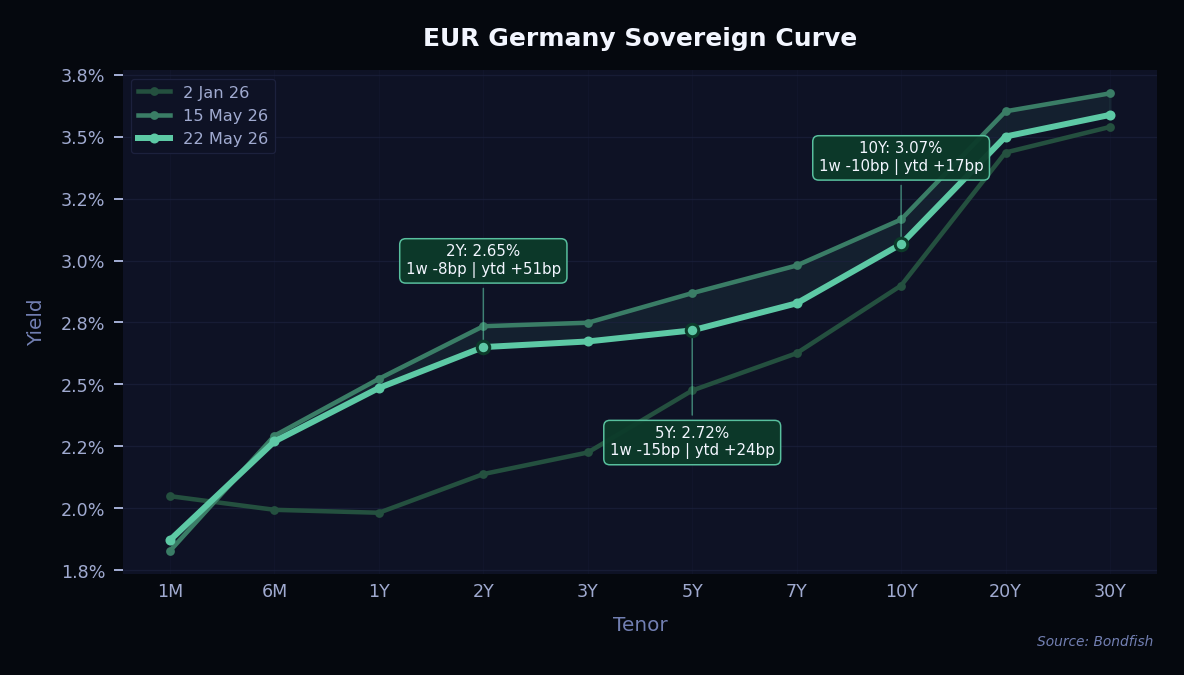

In the euro area, the curve bull-flattened modestly on softer activity data. The Euro Area composite PMI fell to a three-year low of 47.5pts in May, with France particularly weak at 43.5, while 1Q negotiated wage growth slowed to 2.46% y/y — a meaningful deceleration. The 10-year Bund yield fell 6bp to 3.04% and the 30-year declined 5bp to 3.57%, even as input price pressures remained sharply elevated amid the energy shock from the closed Strait of Hormuz. Still, ECB officials including Muller and Demarco continued to argue for a June hike, leaving the curve caught between weak activity and stagflation risk.

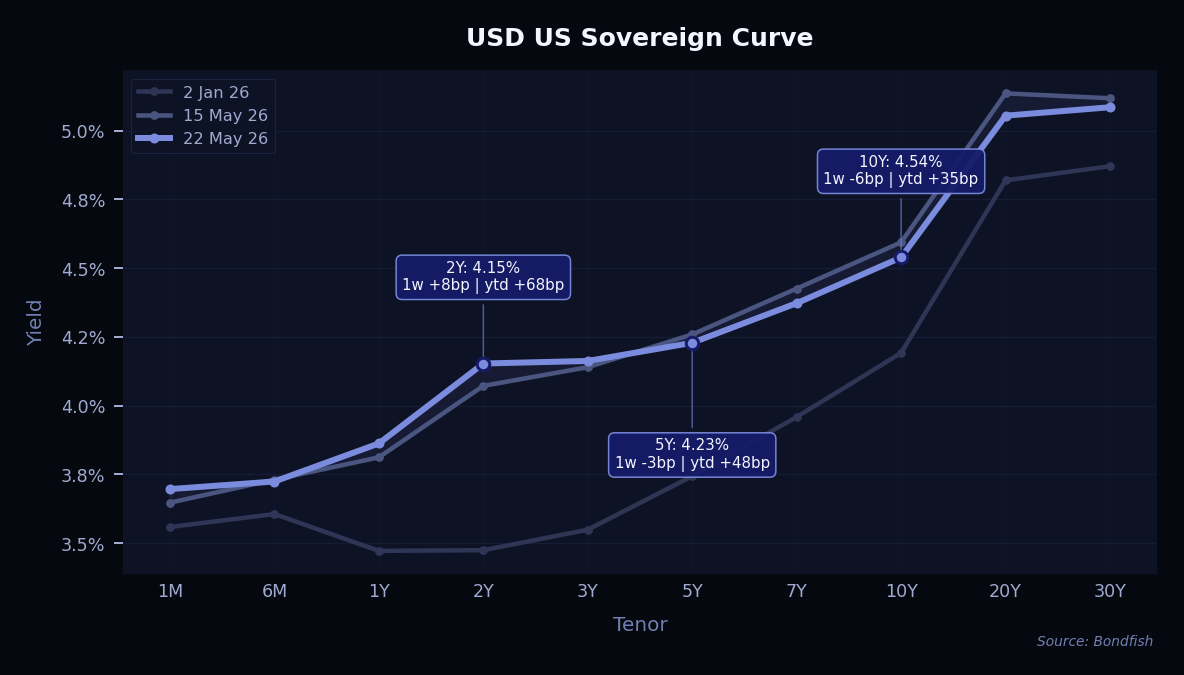

US Treasuries underperformed peers as stronger activity data and a hawkish Fed pivot reshaped the front end. The 2-year yield rose 4bp to 4.12% while the 10-year drifted lower to 4.56% and the 30-year fell to 5.06%, producing a notable bear-flattening. Markets now fully price a 25bp Fed hike by year-end — the first such pricing in some time — after Fed Governor Waller said the next move was “just as likely” to be a hike as a cut and Kevin Warsh was sworn in as the new Fed Chair.

The week's standout outperformers were dominated by long-duration GBP and EUR paper rallying on softer rates, alongside a partial recovery in select USD names. TfL 4% Apr 2064 led the gainers list as gilts rallied on weaker UK inflation and labour-market data, with EIB 4.625% Oct 2054 close behind for the same reason and Blend Funding 3.459% Sep 2049 also benefiting from the long-end repricing. In USD, Paramount Global 5.85% Sep 2043 rallied as investors took a constructive view of the Warner Bros. Discovery acquisition, with strategic synergies and scale offsetting concerns over the planned new debt issuance. goeasy 6.875% Feb 2031 rallied as shares rebounded from a 76% YTD crash after the company adopted a poison-pill defence against takeover bids; Bondfish recently published a credit analysis on goeasy for subscribers interested in the name.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| TfL 4% Apr 2064 | GBP | 5,07% | 6,00% | VeryLow |

|

Reason

Long duration and modest spread repricing.

|

||||

| EIB 4.625% Oct 2054 | GBP | 4,31% | 5,59% | VeryLow |

|

Reason

Long duration and modest spread repricing.

|

||||

| Blend Funding 3.459% Sep 2049 | GBP | 3,98% | 6,31% | Low |

|

Reason

Long duration and modest spread repricing.

|

||||

| Paramount Global 5.85% Sep 2043 | USD | 3,86% | 8,84% | High |

|

Reason

Acquiring Warner Bros. Discovery; market positive on combined scale and synergies, outweighing concerns over planned new debt.

|

||||

| goeasy 6.875% Feb 2031 | USD | 3,78% | 9,75% | VeryHigh |

|

Reason

Shares rebounded from 76% YTD crash after the company adopted a poison pill defence against takeover bids.

|

||||

| Synthomer 7.375% May 2029 | EUR | 3,73% | 13,48% | VeryHigh |

|

Reason

S&P affirmed B rating and the company completed an €800M debt refinancing, extending maturities.

|

||||

| EIB 3.625% Mar 2042 | EUR | 3,14% | 3,50% | VeryLow |

|

Reason

No clear positive issuer catalyst.

|

||||

| Indigo Group 2% Jul 2029 | EUR | 2,35% | 4,59% | Medium |

|

Reason

No clear positive issuer catalyst.

|

||||

| OeKB 3.8% Jan 2062 | EUR | 2,29% | 3,81% | VeryLow |

|

Reason

Long duration and modest spread repricing.

|

||||

Underperformers were concentrated in credit-stressed names and Swiss long-duration paper. Clearwater 4.75% Aug 2028 was the standout, falling after S&P cut the rating to CCC+, citing leverage expected above 10x and the likelihood of a liquidity crisis or debt restructuring. BCP V Modular 6.125% Nov 2028 declined after Fitch downgraded the issuer to B− as leverage breached the downgrade trigger amid weak construction markets and high funding costs. Long-duration paper led the rest of the losses: Sthn Calif Gas 5.75% Nov 2035 and Pfndbnk Schweiz 1.125% Jun 2055 both softened on modest spread repricing, while Virgin Media O2 7.875% Mar 2032 was caught in sector-wide spread widening with no specific company catalyst.

| Name | Cur | Price change 1w(%) |

Yield | Risk Level |

| Sthn Calif Gas 5.75% Nov 2035 | USD | -3,13% | 5,21% | VeryLow |

|

Reason

Long duration and modest spread repricing

|

||||

| Clearwater 4.75% Aug 2028 | USD | -2,96% | 14,34% | VeryHigh |

|

Reason

S&P downgraded to CCC+, citing leverage expected above 10x and likelihood of liquidity crisis or debt restructuring.

|

||||

| Pfndbnk Schweiz 1.125% Jun 2055 | CHF | -2,22% | 1,29% | VeryLow |

|

Reason

Long duration and modest spread repricing.

|

||||

| BCP V Modular 6.125% Nov 2028 | GBP | -2,11% | 9,67% | VeryHigh |

|

Reason

Fitch downgraded to B− as leverage breached downgrade trigger amid weak construction markets and high funding costs.

|

||||

| Virgin Media O2 7.875% Mar 2032 | GBP | -1,69% | 10,82% | VeryHigh |

|

Reason

Sector-wide spread widening; no specific company catalyst identified.

|

||||

| Ziggo Bondco 6.125% Nov 2032 | EUR | -1,57% | 8,59% | VeryHigh |

|

Reason

Sector-wide spread widening; no specific company catalyst identified.

|

||||

| SIG 9.75% Oct 2029 | EUR | -1,10% | 19,17% | VeryHigh |

|

Reason

No clear negative issuer catalyst.

|

||||

| Motion Bondco 4.5% Nov 2027 | EUR | -0,70% | 6,50% | VeryHigh |

|

Reason

Moody's cut outlook to stable from positive as leverage rose to ~9x, EBITDA fell and free cash flow turned deeply negative.

|

||||

Note: only long-term senior unsecured ratings were taken into account.

The headline downgrade of the week was Fitch's move on China Vanke to restricted default (RD), while Whitbread, the parent of Premier Inn, was downgraded to BBB− by Fitch and Akamai Technologies lost its mid-IG status at BBB− from S&P. Clearwater Paper also suffered a multi-notch cut from B+ to CCC+ on rising leverage concerns. On the upgrade side, Kioxia crossed into investment grade at BBB− from S&P, Ovintiv was lifted to BBB by Fitch, Restaurant Brands International was upgraded to BB+ by S&P, and CNP Assurances was raised to A by Fitch.

| Issuer | Agency | Change |

| Access Bank | S&P | B- → B |

| Advancion | S&P | CCC+ → CCC |

| AIP RD Buyer | S&P | B → B- |

| Akamai Technologies | S&P | BBB → BBB- |

| Alchemy US Holdco 1 | Fitch | B- → CCC+ |

| AZZ | Fitch | BB → BB+ |

| Bank of Industry | S&P | B- → B |

| BW Homecare | S&P | CCC- → SD |

| Cabinetworks | S&P | CCC+ → SD |

| China Vanke | Fitch | CC → RD |

| Claudius Finance Parent Sarl | S&P | B+ → B |

| Clearwater Paper | S&P | B+ → CCC+ |

| CNP Assurances | Fitch | A- → A |

| Colombia Telecomunicaciones SA ESP | S&P | B+ → BB- |

| Dtek Oil&Gas Production | Fitch | RD → CC |

| Eldorado Gold | Fitch | B+ → BB- |

| Enstall | S&P | CCC- → D |

| Fagus | Fitch | BB+ → BB |

| Far East Horizon | Fitch | BBB- (new) |

| Getty Images | S&P | B+ → B |

| Guaranty Trust Bank | S&P | B- → B |

| Hauck Aufhaeuser Lampe Privatbank | Fitch | A → AA- |

| Heartland Dental | S&P | B- → B |

| Innovative Chemical Products | S&P | CCC → CCC- |

| Japfa Comfeed Indonesia Tbk PT | Fitch | B+ → BB- |

| Kioxia | S&P | BB+ → BBB- |

| Kymera International | Fitch | B- → CCC+ |

| Mars Intermediate | S&P | CCC+ → CCC |

| Mercer International | Fitch | B- → CCC- |

| Mineral Industri Indonesia Persero PT | Fitch | BBB- → BBB |

| National Securities Clearing | S&P | AA+ → AA |

| NUERNBERGER Beteiligungs | Fitch | A- → A |

| Odyssey Logistics & Technology | S&P | B- → CCC+ |

| Oscar Acquisitionco | S&P | CCC → SD |

| Ovintiv | Fitch | BBB- → BBB |

| Phoenix Guarantor | S&P | B+ → BB- |

| VF Ukraine | Fitch | CCC → CCC- |

| Quartz Acquireco | Fitch | BB- → B+ |

| Resolute Investment Managers | S&P | B → B- |

| Restaurant Brands International | S&P | BB → BB+ |

| SEPLAT Energy | S&P | B → B+ |

| SJM | Fitch | BB- → B+ |

| Stanbic IBTC Bank | S&P | B- → B |

| Standard Chartered Bank Nigeria | S&P | B- → B |

| United Bank for Africa | S&P | B- → B |

| West Technology | S&P | CCC+ → SD |

| Whitbread | Fitch | BBB → BBB- |

| Zenith Bank | S&P | B- → B |

Primary market activity was robust this week, with around €33 billion of European investment-grade supply pricing — one of the stronger weeks of the year. Volkswagen Bank was the headline, printing a triple-tranche €2.75 billion deal across 2028, 2030 and 2033 maturities at coupons of 3.625%, 4.00% and 4.375% respectively. Other notable IG issuers included Eni (€2 billion across 5y and 9y), Enel (€2.5 billion across 5y and 8y), Heidelberg Materials, Teleperformance, Reckitt Benckiser, E.ON, Standard Chartered, CEZ, Deutsche Lufthansa, Aviva, Telefónica, ABN AMRO, DNB Bank and KBC Group, with coupons broadly in the 3.5–4.5% range reflecting the current yield environment. In USD, Charles Schwab, Ecolab (a €5 billion four-tranche deal), Hydro One, PNC Financial Services, Georgia Power and JICA were among the larger prints.

High-yield activity was more subdued at around €3.2 billion, led primarily by non-financial issuers. AMS-Osram priced a €1 billion 6y deal at 7.25%, while Molins Finance, Audax Renovables (€350m at 7.50%), BPER Banca (€500m perpetual at 6.20%) and Bank Millennium also accessed the market. Demand conditions showed some strain — new-issue premiums continued to tick higher, with the 20-bond rolling average reaching year-to-date highs around 13 basis points, while book-coverage ratios dipped to 3.1x, a level last seen in early March. Fund flows reflected this cautious tone, with euro and sterling investment-grade funds both recording outflows, while high yield attracted modest inflows of around €294 million.

| Issuer | Size | Term | Yield | Risk Level |

| Aareal Bank | EUR 0,62bn |

6Y | 3,4% | Very Low |

|

ISIN (CUSIP)

DE000AAR0496

|

||||

| ABN AMRO Bank | USD 1,0bn |

5Y | FLOAT, +85bp | Very Low |

|

ISIN (CUSIP)

XS3388145263

|

||||

| Adidas | EUR 0,50bn |

5Y | 3,5% | Very High |

|

ISIN (CUSIP)

XS3388179676

|

||||

| Aegea Finance Sàrl | USD 0,75bn |

PERP | 7,6% | High |

|

ISIN (CUSIP)

USL01343AE91

|

||||

| Alinma Tier 1 Sukuk | USD 0,50bn |

PERP | 6,6% | Very High |

|

ISIN (CUSIP)

XS3310388734

|

||||

| American Tower | EUR 0,75bn |

7Y | 4,1% | Medium |

|

ISIN (CUSIP)

XS3389205470

|

||||

| American Water Capital | USD 0,50bn |

3Y | 4,6% | Medium |

|

ISIN (CUSIP)

03040WBJ3

|

||||

| AMS-Osram | EUR 1,0bn |

6Y | 7,5% | Very High |

|

ISIN (CUSIP)

XS3382712126

|

||||

| Angola | USD 1,5bn |

5–11Y | 8,2–9,5% | Very High |

|

ISIN (CUSIP)

XS3204248440

|

||||

| Arla Foods amba | EUR 1,0bn |

3–7Y | 3,5–4,0% | Very High |

|

ISIN (CUSIP)

XS3382815879…XS3382816091

|

||||

| Asian Development Bank | USD 4,0bn |

5Y | 4,4% | Very Low |

|

ISIN (CUSIP)

US045167GR80

|

||||

| Audax Renovables | EUR 0,35bn |

5Y | 7,8% | High |

|

ISIN (CUSIP)

XS3379667564

|

||||

| Aviva | EUR 0,57bn |

32Y | 4,9% | Medium |

|

ISIN (CUSIP)

XS3318828012

|

||||

| Baltimore Gas and Electric | USD 0,93bn |

7–30Y | 5,2–6,1% | Low |

|

ISIN (CUSIP)

US059165EV89…US059165EW62

|

||||

| Bank Millennium | EUR 0,50bn |

10Y | 4,7% | Medium |

|

ISIN (CUSIP)

XS3381223067

|

||||

| Bank of China | USD 0,50bn |

5Y | FLOAT, +38bp | Low |

|

ISIN (CUSIP)

XS3381219891

|

||||

| Bank of Valletta | EUR 0,30bn |

6Y | 4,5% | Medium |

|

ISIN (CUSIP)

XS3375198226

|

||||

| Banque Fédérative du Crédit Mutuel | EUR 1,2bn |

9Y | 4,2% | Low |

|

ISIN (CUSIP)

FR0014018HI4

|

||||

| Barclays | GBP 0,75bn |

10Y | 6,1% | Medium |

|

ISIN (CUSIP)

XS3386666245

|

||||

| BAWAG PSK | USD 0,70bn |

3Y | 4,5% | Very Low |

|

ISIN (CUSIP)

XS3389663348

|

||||

| Belfius Banque | EUR 0,75bn |

6Y | 3,3% | Very Low |

|

ISIN (CUSIP)

BE0390317866

|

||||

| Blue Owl Capital | USD 0,40bn |

5Y | 6,6% | Medium |

|

ISIN (CUSIP)

US69121KAL89

|

||||

| BMW International Investment BV | GBP 0,30bn |

6Y | 5,6% | Low |

|

ISIN (CUSIP)

XS3389229900

|

||||

| BNP Paribas Cardif | EUR 1,0bn |

15–20Y | 4,4–4,9% | Very High |

|

ISIN (CUSIP)

FR0014018PQ0…FR0014018PR8

|

||||

| Boots Group Finco / Luxco S.à r.l. | EUR 0,65bn |

7Y | 5,4% | High |

|

ISIN (CUSIP)

XS3134602401

|

||||

| Boots Group Finco / Luxco S.à r.l. | GBP 0,38bn |

7Y | 7,4% | High |

|

ISIN (CUSIP)

XS3134602583

|

||||

| BPER Banca | EUR 0,50bn |

PERP | 6,2% | High |

|

ISIN (CUSIP)

IT0005710469

|

||||

| Province of British Columbia | EUR 2,0bn |

10Y | 3,7% | Very Low |

|

ISIN (CUSIP)

XS3388170964

|

||||

| Caisse Française de Financement Local | EUR 0,75bn |

10Y | 3,7% | Very Low |

|

ISIN (CUSIP)

FR0014018ML8

|

||||

| Canada | USD 3,5bn |

5Y | 4,3% | Very Low |

|

ISIN (CUSIP)

US135087U513

|

||||

| Cassa Centrale Banca | EUR 0,50bn |

4Y | 3,8% | Medium |

|

ISIN (CUSIP)

IT0005710790

|

||||

| CBRE Europe Logistics Partners | EUR 0,50bn |

5Y | 4,0% | Low |

|

ISIN (CUSIP)

XS3385867364

|

||||

| Československá Obchodní Banka | EUR 0,50bn |

5Y | 3,3% | Very Low |

|

ISIN (CUSIP)

SK4000029518

|

||||

| CEZ | EUR 0,75bn |

8Y | 4,4% | Low |

|

ISIN (CUSIP)

XS3373524050

|

||||

| Chubb INA Holdings | USD 1,0bn |

10Y | 5,3% | Low |

|

ISIN (CUSIP)

171239AN6

|

||||

| Columbia Pipelines Operating Company | USD 0,75bn |

10Y | 5,5% | Medium |

|

ISIN (CUSIP)

USU2100BAA53

|

||||

| Commonwealth Bank of Australia | EUR 1,2bn |

7Y | 3,3% | Very Low |

|

ISIN (CUSIP)

XS3386669694

|

||||

| Republic of Congo | USD 0,85bn |

10Y | 10,0% | Very High |

|

ISIN (CUSIP)

XS3376882687

|

||||

| Corporación Andina de Fomento (CAF) | EUR 1,0bn |

7Y | 3,6% | Very Low |

|

ISIN (CUSIP)

XS3385967230

|

||||

| Dar Al-Arkan Sukuk | USD 0,60bn |

5Y | 7,4% | Very High |

|

ISIN (CUSIP)

XS3377655645

|

||||

| Deutsche Lufthansa | EUR 0,75bn |

6Y | 4,2% | Medium |

|

ISIN (CUSIP)

XS3376351055

|

||||

| DNB Bank ASA | EUR 0,75bn |

6Y | 3,6% | Low |

|

ISIN (CUSIP)

XS3388353024

|

||||

| E.ON International Finance BV | EUR 1,3bn |

5–10Y | 3,5–4,1% | Medium |

|

ISIN (CUSIP)

XS3386748993…XS3386749025

|

||||

| Ecolab | USD 5,0bn |

3–10Y | 4,6–5,4% | Low |

|

ISIN (CUSIP)

US278865BU33…US278865BX71

|

||||

| Eesti Energia | EUR 0,30bn |

5Y | 4,6% | Medium |

|

ISIN (CUSIP)

XS3338741567

|

||||

| Emlak Konut Varlik Kiralama | USD 0,65bn |

5Y | 7,8% | High |

|

ISIN (CUSIP)

XS3386678844

|

||||

| Enel | EUR 2,5bn |

4–7Y | 3,6–4,0% | Medium |

|

ISIN (CUSIP)

XS3358330663…XS3358330820

|

||||

| Eni | EUR 2,0bn |

5–9Y | 3,6–4,1% | Low |

|

ISIN (CUSIP)

XS3388188586…XS3388189394

|

||||

| Erste & Steiermärkische Bank | EUR 0,40bn |

6Y | 4,1% | Low |

|

ISIN (CUSIP)

AT0000A3UX25

|

||||

| Eurobank | EUR 0,70bn |

6Y | 3,9% | Medium |

|

ISIN (CUSIP)

XS3386670270

|

||||

| European Bank for Reconstruction and Development | USD 2,0bn |

5Y | 4,3% | Very Low |

|

ISIN (CUSIP)

US29874QFF63

|

||||

| European Investment Bank | EUR 1,5bn |

5Y | FLOAT, +26bp | Very Low |

|

ISIN (CUSIP)

EU000A4ETDK9

|

||||

| Evergy Missouri West | USD 0,30bn |

3Y | 4,7% | Medium |

|

ISIN (CUSIP)

USU3000EAC40

|

||||

| EWE | EUR 0,50bn |

8Y | 4,0% | Medium |

|

ISIN (CUSIP)

DE000A46ZXA7

|

||||

| Fédération des Caisses Desjardins du Québec | EUR 0,75bn |

5Y | 3,2% | Very Low |

|

ISIN (CUSIP)

XS3389643407

|

||||

| Fédération des Caisses Desjardins du Québec | USD 0,75bn |

5Y | 5,0% | Very Low |

|

ISIN (CUSIP)

US31429LAQ41

|

||||

| Fideicomiso Irrevocable F/6185 | USD 0,80bn |

10Y | 7,1% | High |

|

ISIN (CUSIP)

USP3990QAA96

|

||||

| FMC | USD 1,2bn |

5Y | 8,0% | High |

|

ISIN (CUSIP)

USU30249AC72

|

||||

| Ford Motor Credit Company | USD 1,0bn |

10Y | 6,5% | Medium |

|

ISIN (CUSIP)

US345397J952

|

||||

| Georgia Power | USD 1,3bn |

2–3Y, PERP | 4,6–4,8%; FLOAT | Low |

|

ISIN (CUSIP)

US373334LE90

|

||||

| Golub Capital Bdc | USD 0,50bn |

5Y | 6,5% | Medium |

|

ISIN (CUSIP)

38173MAF9

|

||||

| Republic of Indonesia | USD 2,0bn |

5–10Y | 5,0–5,7% | Medium |

|

ISIN (CUSIP)

US455780EH58…US455780EJ15

|

||||

| Huzhou City Investment Development Group | USD 0,29bn |

3Y | 4,5% | Medium |

|

ISIN (CUSIP)

XS3379901260

|

||||

| Hydro One | USD 1,0bn |

5Y | 4,8% | Low |

|

ISIN (CUSIP)

US448810AD30

|

||||

| Hypo Tirol Bank | EUR 0,30bn |

7Y | 3,3% | Very Low |

|

ISIN (CUSIP)

AT0000A3UZM4

|

||||

| Republic of Iceland | EUR 0,50bn |

5Y | 3,4% | Low |

|

ISIN (CUSIP)

XS3388350434

|

||||

| IDB Invest | USD 1,0bn |

5Y | 4,4% | Very Low |

|

ISIN (CUSIP)

US45828Q2H98

|

||||

| International Consolidated Airlines Group (IAG) | EUR 1,0bn |

5–8Y | 3,9–4,5% | Medium |

|

ISIN (CUSIP)

XS3364672256…XS3364672413

|

||||

| Japan International Cooperation Agency | USD 1,0bn |

5Y | 4,5% | Low |

|

ISIN (CUSIP)

US47109LAK08

|

||||

| KBC Groep | EUR 0,75bn |

8Y | 3,9% | Low |

|

ISIN (CUSIP)

BE0390313824

|

||||

| Kennametal | USD 0,30bn |

10Y | 5,8% | Medium |

|

ISIN (CUSIP)

US489170AG50

|

||||

| KfW | EUR 3,0bn |

10Y | 3,4% | Very Low |

|

ISIN (CUSIP)

DE000A5H27X9

|

||||

| KODIT Global 2026-1 | USD 0,30bn |

3Y | 4,6% | Very Low |

|

ISIN (CUSIP)

XS3382828187

|

||||

| Kommuninvest i Sverige | EUR 1,2bn |

4Y | 3,0% | Very Low |

|

ISIN (CUSIP)

XS3385516060

|

||||

| Kreissparkasse Koeln | EUR 0,25bn |

7Y | 3,2% | Very Low |

|

ISIN (CUSIP)

DE000A5JCXR0

|

||||

| Kuntarahoitus (MuniFin) | USD 1,0bn |

5Y | 4,4% | Very Low |

|

ISIN (CUSIP)

XS3388204458

|

||||

| Landesbank Saar | EUR 0,25bn |

10Y | 3,5% | Very Low |

|

ISIN (CUSIP)

DE000SLB4386

|

||||

| L-Bank (Landeskreditbank Baden-Württemberg) | GBP 0,15bn |

4Y | 4,2% | Very Low |

|

ISIN (CUSIP)

XS3324593097

|

||||

| L-Bank (Landeskreditbank Baden-Württemberg) | GBP 0,15bn |

4Y | 4,2% | Very Low |

|

ISIN (CUSIP)

XS3324593097

|

||||

| LBBW | EUR 1,0bn |

6Y | 3,2% | Very Low |

|

ISIN (CUSIP)

DE000LB4XGB2

|

||||

| mBank | EUR 0,75bn |

7Y | 4,3% | Medium |

|

ISIN (CUSIP)

XS3386565991

|

||||

| Merck | USD 6,0bn |

2–30Y | 4,3–5,9%; FLOAT | Very Low |

|

ISIN (CUSIP)

US58933YCE32…US58933YCJ29

|

||||

| Metropolitan Life Global Funding I | EUR 0,50bn |

7Y | 4,0% | Very Low |

|

ISIN (CUSIP)

XS3386672565

|

||||

| Mobility Global | USD 2,0bn |

3–10Y | 5,1–6,1% | Medium |

|

ISIN (CUSIP)

USU6071MAA72…USU6071MAC39

|

||||

| Molins Finance | EUR 0,50bn |

7Y | 5,5% | High |

|

ISIN (CUSIP)

XS3385893956

|

||||

| Molson Coors Beverage | USD 1,5bn |

5–10Y | 4,9–5,5% | Medium |

|

ISIN (CUSIP)

US60871RAS94

|

||||

| Kingdom of Morocco | EUR 2,2bn |

8–12Y | 4,8–5,3% | High |

|

ISIN (CUSIP)

XS3387586004…XS3385444990

|

||||

| NBN (Australia) | EUR 0,75bn |

8Y | 3,8% | Very Low |

|

ISIN (CUSIP)

XS3368925387

|

||||

| Norddeutsche Landesbank (NORD/LB) | EUR 1,5bn |

3–3Y | 2,8–3,0% | Very Low |

|

ISIN (CUSIP)

DE000NLB51T6…DE000NLB5503

|

||||

| Nordic Investment Bank | EUR 1,0bn |

7Y | 3,1% | Very Low |

|

ISIN (CUSIP)

XS3391770743

|

||||

| Northwestern Mutual Life Insurance | USD 1,2bn |

30Y | 6,1% | Very Low |

|

ISIN (CUSIP)

U66647AF2

|

||||

| NRW.BANK | EUR 1,5bn |

7Y | 3,2% | Very Low |

|

ISIN (CUSIP)

DE000NWB0B16

|

||||

| OCBC Bank | USD 0,50bn |

3Y | FLOAT, +47bp | Very Low |

|

ISIN (CUSIP)

XS3386635448

|

||||

| Oman Arab Bank | USD 0,40bn |

PERP | 6,8% | Medium |

|

ISIN (CUSIP)

XS3303713310

|

||||

| Province of Ontario | USD 3,0bn |

10Y | 4,9% | Very Low |

|

ISIN (CUSIP)

US683234D471

|

||||

| PNC Financial Services Group | USD 1,6bn |

3Y | 4,6%; FLOAT | Low |

|

ISIN (CUSIP)

US693475CJ21

|

||||

| Pricoa Global Funding I | USD 0,45bn |

5Y | 5,0% | Very Low |

|

ISIN (CUSIP)

US74153XBS53

|

||||

| Prs Finance | GBP 0,19bn |

5Y | FLOAT, +52bp | Very Low |

|

ISIN (CUSIP)

XS3248351564

|

||||

| RGA Global Funding | USD 0,50bn |

5Y | 5,2% | Low |

|

ISIN (CUSIP)

USU76212AA47

|

||||

| Rheinmetall | EUR 0,50bn |

5Y | 3,5% | Medium |

|

ISIN (CUSIP)

XS3344481935

|

||||

| RR Donnelley & Sons | USD 0,90bn |

5Y | 12,4% | Very High |

|

ISIN (CUSIP)

USU25783AL24

|

||||

| State of Saxony-Anhalt | EUR 0,50bn |

2Y | 2,9% | Very Low |

|

ISIN (CUSIP)

DE000A46ZYY5

|

||||

| Societe Generale | USD 1,2bn |

6Y | 5,4% | Low |

|

ISIN (CUSIP)

US83368TCQ94

|

||||

| Southern Company Gas Capital | USD 0,50bn |

30Y | 6,0% | Medium |

|

ISIN (CUSIP)

US8426EPAL25

|

||||

| Standard Chartered | EUR 1,0bn |

6Y | 3,9% | Low |

|

ISIN (CUSIP)

XS3381221525

|

||||

| Stedin Holding | EUR 0,50bn |

7Y | 3,8% | Very High |

|

ISIN (CUSIP)

XS3389660161

|

||||

| Swedish Export Credit | EUR 1,0bn |

7Y | 3,3% | Very Low |

|

ISIN (CUSIP)

XS3388158241

|

||||

| Sydbank | EUR 0,50bn |

5Y | 3,7% | Low |

|

ISIN (CUSIP)

XS3391818963

|

||||

| Tatra Banka | EUR 0,25bn |

6Y | 4,3% | Medium |

|

ISIN (CUSIP)

SK4000029559

|

||||

| Telefónica Emisiones | EUR 0,75bn |

8Y | 4,3% | Medium |

|

ISIN (CUSIP)

XS3388349188

|

||||

| Teleperformance | EUR 1,2bn |

6–9Y | 4,8–5,5% | Very High |

|

ISIN (CUSIP)

FR0014018LK2…FR0014018LM8

|

||||

| Tietoevry | EUR 0,30bn |

5Y | 4,4% | Very High |

|

ISIN (CUSIP)

FI4000599121

|

||||

| TP ICAP Finance | GBP 0,25bn |

7Y | 6,5% | Medium |

|

ISIN (CUSIP)

XS3092057077

|

||||

| Trinity Capital | USD 0,30bn |

5Y | 7,2% | Medium |

|

ISIN (CUSIP)

US896442AL44

|

||||

| VEON MidCo BV | USD 1,4bn |

5–7Y | 7,0–7,5% | High |

|

ISIN (CUSIP)

XS3372847957…XS3372848419

|

||||

| Volkswagen Bank | EUR 2,8bn |

2–8Y | 3,7–4,5% | Medium |

|

ISIN (CUSIP)

XS3386702149…XS3386742798

|

||||

| Xylem | USD 1,0bn |

7–10Y | 5,2–5,5% | Medium |

|

ISIN (CUSIP)

US98419MAN02…US98419MAP59

|

||||

| Yapı ve Kredi Bankası | USD 0,50bn |

PERP | 9,4% | Very High |

|

ISIN (CUSIP)

XS3307951403

|

||||

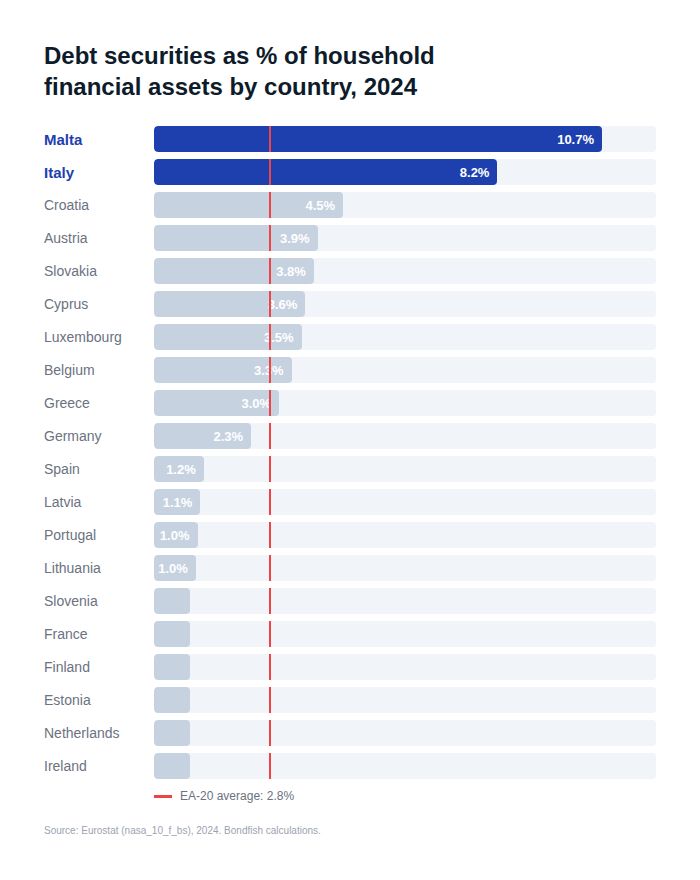

Which European households hold the most bonds? We looked at Eurostat's latest financial balance sheet data (2024) and found a dramatic gap across the euro area. Malta and Italy stand out with 10.7% and 8.2% of household financial assets in debt securities — three to four times the EA-20 average of 2.8%. Meanwhile, the Netherlands and Ireland sit below 0.2%. The divergence isn't cultural — it's policy-driven. Italy offers a preferential 12.5% tax rate on government bonds versus 26% on most other investments, and the Treasury has raised over €112 billion through retail-targeted issuances like BTP Valore since 2023. In Malta, the Central Bank acts as a daily market maker for government bonds, publishing bid and offer prices every morning and effectively guaranteeing liquidity for retail investors. Other highly indebted euro area governments might want to take notes.