.jpg)

Want to know in advance what you will earn on your investment. If you intend to hold a bond to maturity, it works much like a typical time deposit

Do not want to pay ongoing fees each year

Are confident in the creditworthiness of a bond issuer

Prefer to invest on your own and pick the better returns from the wide variety of options available

Do not want to worry about the credit risk of bond issuers

Have limited capital to invest

You are concerned about liquidity and want to be able to sell the instrument whenever you want with low costs

Navigating the world of investments can often feel like an exhilarating yet complex journey. Today, we're set to compare two popular investment vehicles in the fixed income market: Bond ETFs (Exchange-Traded Funds) and single-name bonds. Often, Bond ETFs are seen as more suitable for individual investors compared to the latter option. But is this really the case, or just a myth? Let's dive in!

A Bond ETF is akin to a basket containing a variety of bonds. These funds are traded on stock exchanges, similar to stocks. They offer a collection of bonds in a single package, providing immediate diversification. The sheer number of bonds in an ETF's portfolio can be staggering, sometimes encompassing over 10,000 different bonds.

Managed by large investment companies such as BlackRock, Amundi or Invesco, Bond ETFs typically fall into two categories. The first, known as passively managed ETFs, are designed to track the performance of a bond index, thereby replicating its composition. The second type, actively managed ETFs, operates based on a specific investment mandate, which may include criteria like ratings, duration, and currency, among others.

For managing these ETFs, investment companies charge management fees, which are typically deducted periodically over the year and are calculated as a percentage of the assets under management (AUM). It's worth noting that actively managed ETFs tend to charge higher fees than their passively managed counterparts.

A single-name bond, on the other hand, is an individual bond issued by a single entity, like a government or a corporation. When you buy a single-name bond, you're essentially lending money to the issuer, who promises to pay you back on a specific date, with regular interest payments along the way.

1. Greater Transparency and Predictability

The majority of single-name bonds have a specific maturity date. Although the offering documents may sometimes provide for early redemption options, you have a fairly solid idea of the future payment schedule of the investment. You also know exactly who you're lending money to. So a straightforward fundamental analysis can be done. But most importantly, you'll receive a known annual return, called a yield, if you intend to hold a bond until maturity.

In contrast, most ETFs don't have a fixed maturity. While finite life Bond ETFs, which have a fixed maturity date like single bonds, do exist, they are relatively rare and may have lower liquidity compared to their perpetual counterparts.

The composition of a Bond ETF's portfolio changes constantly. Bonds are added to and removed from the fund on a regular basis, introducing a degree of uncertainty. This fluidity means that it's often unpredictable what the ETF's return will be over a given period of time, such as a year.

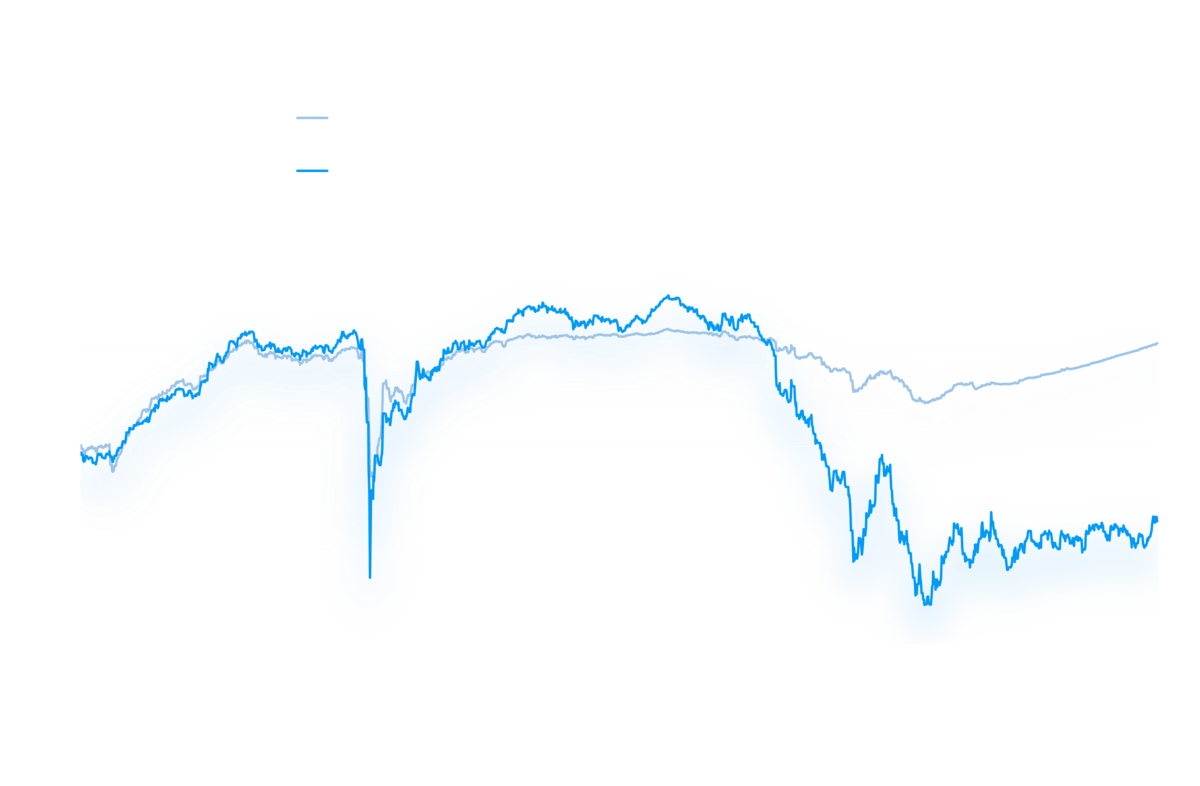

To illustrate this, let's consider a practical example. Imagine that five years ago, we invested in a 5-year bond issued by BNP Paribas, set to mature in November 2023, and also in the iShares Core Euro Corporate Bond ETF, which at that time was primarily composed of high-grade corporate bonds denominated in euros with an average maturity of 5 years. The BNP bond was trading with a yield of 1.2% back then, while the average yield of the bonds within the ETF was around 1.5%.

Now, let's see the outcomes. Over these five years, the BNP bond would have yielded a total return of over 6%, which aligns exactly with the yield known at the time of purchase. On the other hand, an investment in the ETF would have resulted in a loss of over 4%. That's a substantial difference in performance, exceeding 10%.

2. No Recurring Fees

When it comes to costs, the landscape between single-name bonds and Bond ETFs is quite distinct. Bond ETFs typically come with management fees, with passively managed funds charging an average of 0.2% of AUM and actively managed funds charging an average of 0.4% of AUM. These fees are deducted annually and can significantly impact returns. Consider that the average yield on single name high grade corporate bonds in euros today is around 4%; thus, ETF fees can eat up to 10% or more of your annual return. This fee impact is something to consider in your investment strategy.

In contrast, investing in single-name bonds generally involves a fixed transaction fee when buying and selling. For instance, platforms like TradeRepublic charge a fixed fee of 1 EUR per bond transaction, regardless of the amount. It's worth noting that buying and selling bond ETFs also incur commission fees.

To illustrate, let's compare the costs for purchasing and holding 10,000 Euro worth of a single-name bond versus a bond ETF with a 0.4% management fee over a year. For the single-name bond, your expense would be just 1 Euro, while for the ETF, it would amount to 40 Euros paid annually.

3. A Wide Variety of Choices

One of the most significant advantages of single-name bonds is the vast array of options they offer, catering to a wide range of risk-return profiles. The Euro-denominated bond universe is a testament to this diversity, comprising more than 20,000 bonds. Among these, about 1,000 bonds are actively traded and accessible to individual investors, with denominations as low as or lower than 1,000 euros.

This expansive selection allows investors to tailor their portfolios to their precise preferences and risk tolerance. For example, you could opt for nearly risk-free government bonds, such as 1-year term German Bunds currently yielding around 3.5%, or venture into higher-risk territories with corporate bonds. An example of the latter is the bond of the Finnish PHM Group Holding Oyj, which matures in 2 years and now offers a yield of more than 9% in euros.

In comparison, the Euro-denominated Bond ETF market offers a more limited selection. There are only about 200 ETFs available in this category, and almost all of them are passively managed. This limited variety stands in stark contrast to the extensive choices available in single-name bonds. While ETFs provide the convenience of pre-packaged diversification, they may not offer the same level of specificity and customization that can be achieved by selectively investing in individual bonds.

While single-name bonds offer an impressive array of options and specific benefits, it's important to consider the other side of the coin. Bond ETFs, despite their more limited variety in the Euro-denominated market, bring their own unique set of advantages. These benefits can be particularly appealing to certain types of investors or investment strategies. Let's explore what makes bond ETFs an attractive option for many.

1. Enhanced Liquidity: Bond ETFs typically offer better liquidity. This manifests in two ways:

a) Availability of Size: Compared to single-name bonds, where live quotes are only available for a fraction of the numerous bonds in the market, ETFs generally provide more opportunities to find the size you want to buy or sell.

NB: With Bondfish and our specialized bond screener, we want to help you find liquid bonds that you can trade immediately.

b) Tighter Bid-Ask Spreads: ETFs often feature narrower bid-ask spreads, which refers to the difference between the buying and selling prices. A wider spread results in higher trading costs, as it reflects the approximate difference between the price you pay when buying the asset and the price you might receive when selling it later. However, it's important to note that while ETFs usually don't have a fixed term, single-name bonds do. So if you plan to hold a bond until maturity, you won't face the cost associated with bid-ask spread differences.

The reason behind ETFs' better liquidity is largely due to market makers, typically banks and financial institutions, who are contractually obliged to provide consistent purchase and sale quotes during exchange trading hours for the ETFs.

2. Small Lot Sizes

ETFs stand out for their flexibility in trading volumes. They can be traded in much smaller quantities compared to bonds, making them highly accessible for a range of investment sizes. In fact, many ETFs are available in fractions as low as 10 Euros and below, offering a level of entry that is particularly suitable for smaller investors or those looking to diversify with limited capital. In contrast, bonds typically trade at higher minimum sizes, often around 1,000 Euros, and more frequently at 100,000 Euros or more, which can be a significant barrier for individual investors with limited funds.

3. Reduced Credit Risk

One of the key strengths of bond ETFs lies in their ability to spread out risk across a diverse portfolio. This diversification dilutes the impact of any single issuer's financial difficulties on the overall ETF performance. For instance, if an issuer defaults, it typically won't significantly affect the ETF's returns, as the bonds from that issuer usually represent only a small portion of the entire portfolio, often not exceeding a percent.

In contrast, if you invest in a single-name bond and the issuer defaults, it could lead to a substantial loss, potentially nearly the entire invested amount. Therefore, when investing in single-name bonds, you better be confident about the credit quality of the issuer.

Our bond screener and weekly bond report meticulously highlight the credit risks associated with each bond, helping you make informed investment decisions.

In addressing our initial query – whether Bond ETFs are indeed more suitable for individual investors compared to single-name bonds – it becomes clear that the answer isn't so straightforward. The decision hinges on your personal investment preferences and goals.

If you value predictable cash flows, want control over your risk-return profile, seek a fixed term to maturity, and prefer clarity on who you’re lending to, then single-name bonds could be your ideal choice. Contrary to common perception, there is an abundance of bonds traded in sizes that are accessible and suitable for individual portfolios, and we at Bondfish are here to guide you through this universe.

Ultimately, whether you lean towards the diversification and convenience of Bond ETFs or the specificity and control of single-name bonds, it's about finding the right fit for your unique financial journey. Explore the options with us at Bondfish, and let's navigate the world of bonds together.